In the modern world, insurance has become an indispensable part of financial planning for most individuals and families. QBE Insurance has provided a stable return for investors in the last ten years, just one reason why investing oracle Warren Buffett has chosen insurance as part of his portfolio over the years. With insurance premiums continuing to rise, will QBE’s share price follow suit? Let’s find out.

- With its global reach and diverse portfolio, QBE Insurance Group is well-positioned for growth and resilience in the competitive insurance market.

- Rising premiums and improved profitability in North America are driving earnings growth for QBE, which is projected to increase by 25-30% in 2024.

- Analysts are optimistic about the stock. Bloomberg Analyst recommendations include 11 buys, two holds, and one sell for QBE, signalling an 11% upside from current levels.

View QBE Insurance

The Basics

QBE Insurance Group is a global insurance and reinsurance company headquartered in Sydney. It employs more than 14,500 people in 37 countries. Insurance plays a critical role in the economy, providing essential services that people rely on for financial security. It mitigates risks, protects assets, and offers financial stability to individuals and businesses alike.

The company offers commercial, personal, and specialty products and risk management solutions to help people and businesses manage risks. It focuses on three main business segments: car and vehicle, home, and small business insurance. The company is listed on the ASX and is the largest insurer by market cap, with a market cap of over AUD$25 billion.

*Past performance is not an indication of future results.

Competitor Diagnosis

There is healthy competition in the Australian insurance market, with over 90 licensed insurers with a mix of Australian and global businesses operating, such as Insurance Australia Group (IAG), Allianz Insurance, Chubb Insurance, and ING, just to name a few. These insurers also face intense competition from banks, with Suncorp and the big four wanting a piece of the valuable insurance market.

IAG is the largest general insurer in Australia, making it QBE’s biggest competitor. However, gaining market share isn’t easy for QBE, especially when competing with giants like Allianz, who are almost four times larger and have substantial resources. Despite this, QBE’s global presence offers a diversified revenue stream that operates on every continent. This international footprint makes QBE more resilient and provides growth opportunities beyond the local market.

QBE still has work to do overseas, and North America remains a crucial area for the business. This international focus gives the company an edge over local competitors by spreading risk and capturing global growth opportunities.

Financial Health Check

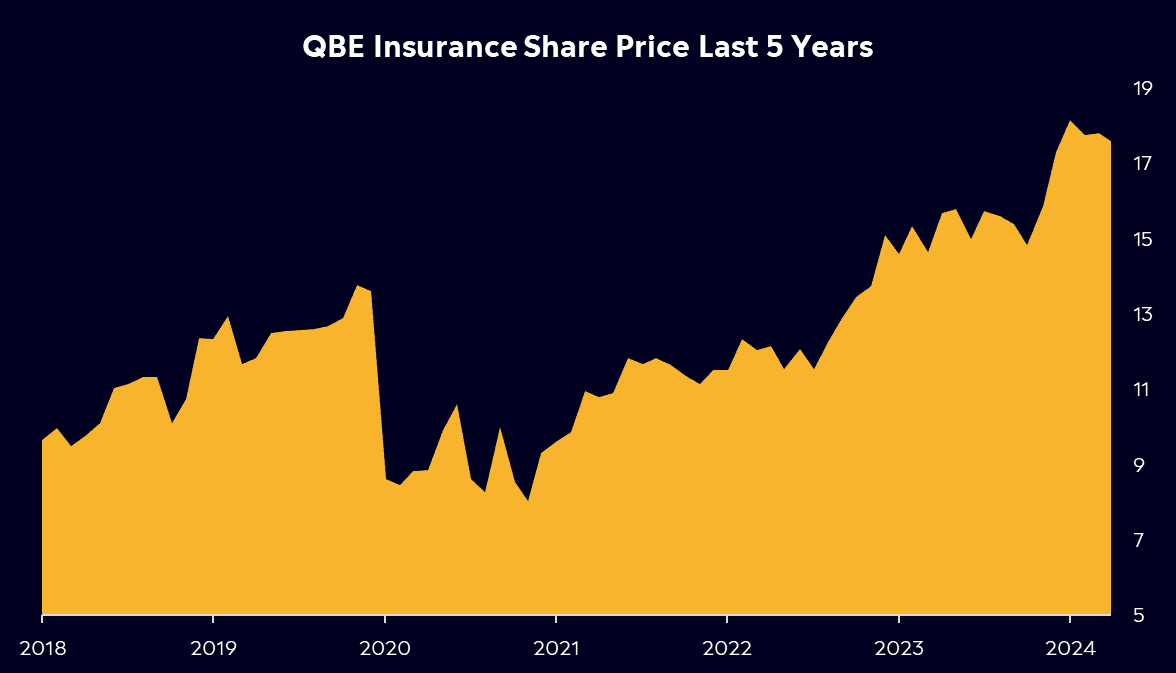

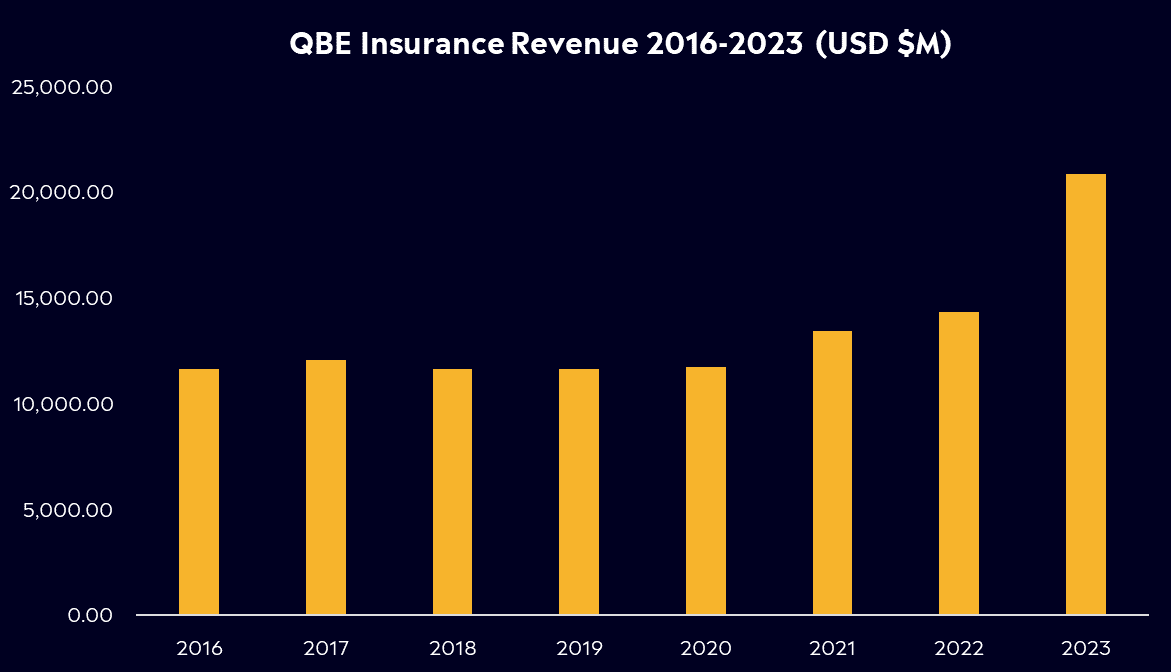

Insurance premiums have continued to rise in recent years, especially since the pandemic. This has helped QBE’s top and bottom lines, with earnings growing by 60% in 2023 and revenue growing by 45%. Those premiums look set to keep growing, supporting earnings growth for 2024.

The company has an impressive combined ratio of 95.2%, indicating profitability in underwriting, but significant work remains to prove its profitability in North America. Enhanced profitability and rising premiums in this key market are crucial to QBE’s projected earnings growth of 25-30% in 2024. This bodes well for its dividend, which could yield around 5.1%. This is a healthy payout for a stock trading at just 9.7x forward price to earnings, well below its 10-year average of 13.7x and below market peers.

The business has also been helped by a lack of ‘catastrophes’ recently, keeping payouts low as premiums grew. However, this is not always one-sided, as unforeseen weather events and natural disasters can significantly impact earnings. Insurers must be prepared for these eventualities, which can dent profitability.

*Past performance is not an indication of future results.

Buy, Hold or Sell?

Insurance companies don’t jump out to investors as the most exciting stocks to own, and that’s because they aren’t, in all honesty. However, investing doesn’t always have to be titillating. QBE has a strong track record of delivering for investors and paying a quality dividend. The business is also making great progress in North America, where it has recently streamlined its operations, and profitability looks to be improving.

Analysts are optimistic about the stock, especially compared to Australia’s other major insurer, IAG. Bloomberg Analyst recommendations include 11 buys, two holds, and one sell for QBE, with an average price target of AUD$19.48, signalling an 11% upside from current levels. This positive outlook reflects QBE’s strategic positioning and growth potential.

QBE Insurance Group stands out in a competitive market due to its global presence, diversified revenue streams, and strong financial performance. While competition remains fierce, QBE’s strategic advantages, robust growth prospects, and stable growth and income will make it a standout for some investors.

View QBE Insurance

eToro Service ARSN 637 489 466 promoted by eToro AUS Capital Limited ACN 612 791 803 AFSL 491139. Capital at risk. See PDS and TMD. This communication is general information and education purposes only and should not be taken as financial product advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial product. It has been prepared without taking your objectives, financial situation or needs into account. Any references to past performance and future indications are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.