Breville might be known for its coffee machines and toasters, but behind the kitchen essentials is one of Australia’s best-run companies. With global reach, clever branding and innovation at its core, Breville has a healthy balance sheet, solid cash flow, and double-digit growth, a great combination for long-term investors. But with Trump’s new tariffs heating up again and causing a stir in global markets, is the pressure rising on this household favourite? Let’s find out.

- Breville’s coffee segment is booming, driving double-digit revenue growth and a fast-growing subscription service putting it front and centre in the at-home barista trend.

- New tariffs on Chinese and Asian-made goods are a major test, but Breville’s global brand and early inventory moves give it breathing room.

- Breville has 5 buy ratings, 7 holds, and 4 sells, with an average price target of AUD$34..27 signalling a potential upside of 25.5% from its last closing price.

Explore Breville (BRG:ASX)

The Basics

Breville Group was founded in Sydney in 1932, and it has come a long way since its early days making radios. Now, it’s best known for designing and selling premium small kitchen appliances. You may use one of their items every single day without even realising it. From coffee machines and blenders to food processors, toasters, and smart ovens, Breville makes all the countertop essentials that are sold in more than 70 countries.

Alongside its Breville products, it also sells under other brands like Sage (its name in the UK/Europe), Baratza (coffee grinders), and Kambrook (a more affordable, value-focused option). These brands allow Breville to cover everything from the high-end enthusiast market to everyday essentials, depending on the customer and region.

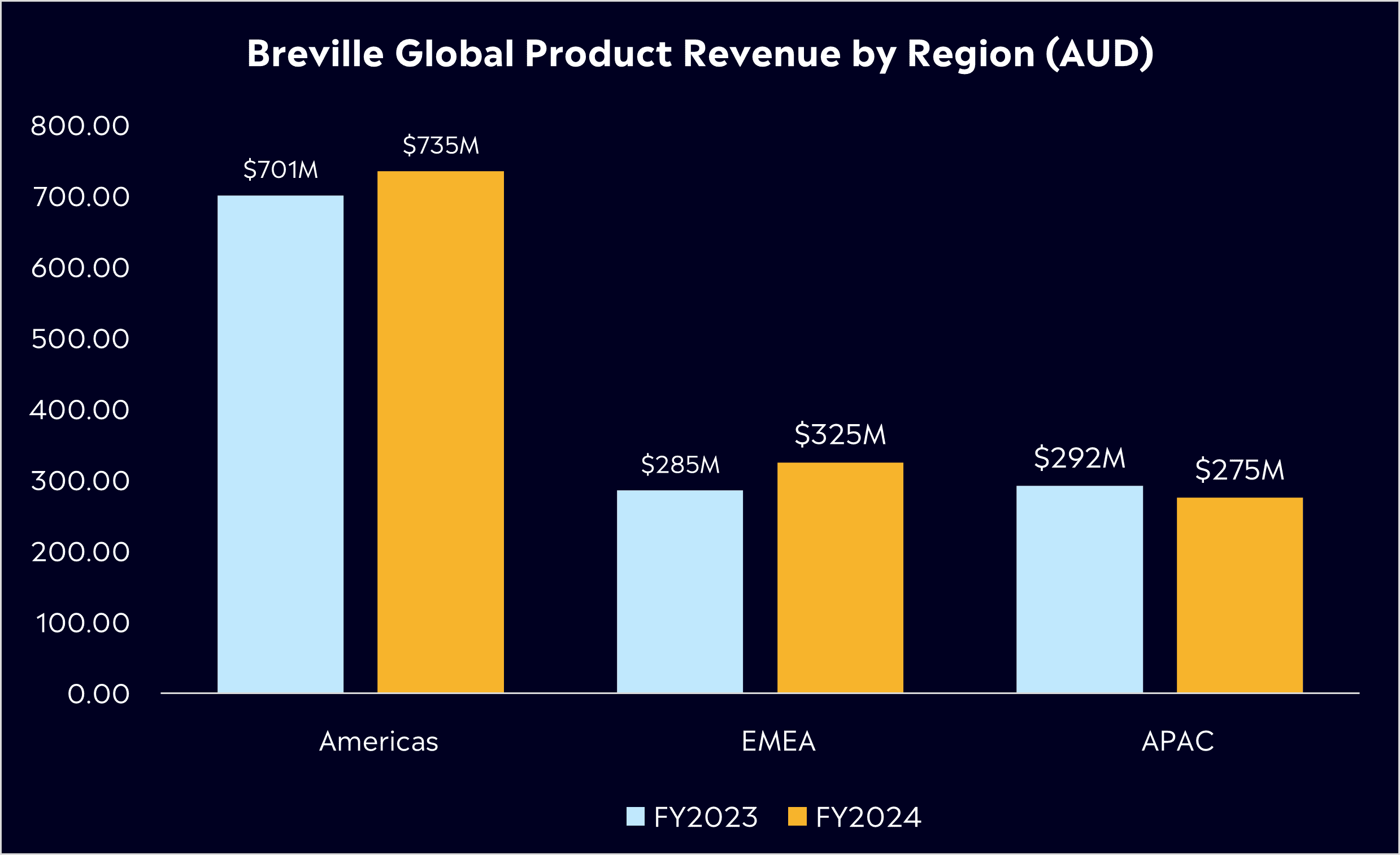

Its revenue is split into two segments. Firstly, global product. This is Breville’s core business, where they design and sell their branded products worldwide. Revenue is divided via the Americas, EMEA (Europe, Middle East & Africa), and APAC. This segment of the business accounts for around 88% of revenue.

Then there is the distribution segment, a much smaller part of the business that distributes third-party brands like Nespresso in Australia and New Zealand, making up around 12% of total revenue.

Breville is also making moves deeper into the coffee game. In recent years, they’ve made two acquisitions to become the ‘one-stop shop’ for at-home specialty coffee. They’ve also launched Beanz, a subscription-based coffee bean delivery business. It saw a massive 71% growth in the first half of the fiscal year and continues to see strong interest.

Breville has built its reputation on quality and innovation. It’s not just about making good-looking appliances, it’s about making them smarter as well. Breville helped revolutionise the at-home coffee game, and its smart ovens and espresso machines continue to raise the bar. This innovation-first mindset has allowed the brand to command premium pricing globally and stay ahead in a competitive space.

Fun Fact: Although the original ‘inventor’ of the sandwich press is up for debate, Breville created the first ever ‘jaffle’ machine in the 1970s. Yes, you’ve got Breville to thank for those lovely toasties.

Competitor Diagnosis

Breville faces competition from global appliance giants and specialised kitchen gadget brands. When we think about some of the brands that help kit out our homes, it’s usually LG, Samsung, Bosch etc. But, from a small application perspective, we look at other well-known names like KitchenAid (owned by Whirlpool), Tefal (owned by Groupe SEB), Russell Hobbs (owned by Spectrum Brands) and newer entrants like SharkNinja.

Although toasters and blenders are key, Breville’s coffee machine segment is becoming more important than ever. Breville contends with Italy’s De’Longhi, a very well-known brand worldwide. Breville and De’Longhi often go head-to-head in coffee machines, with both selling ‘cafe quality coffee at home’ machines that can rise as high as almost AUD$4000.

Those companies offer a broad range of kitchen appliances, often overlapping with Breville’s product categories. KitchenAid is famous for its mixers, which have a high price point thanks to their classic design and durability, while Breville often differentiates itself with more innovative features and technology in its products. There are many other competitors, too many to list, but we can also look at own-brand kitchen appliances from brands such as Kmart here in Australia that target more cost-conscious consumers.

With competition rife, there are challenges for Breville. Big players like De’Longhi or Tefal have extensive distribution and product ranges, but price points are key. SharkNinja’s products are often cheaper while still offering good functionality. SharkNinja’s products are also getting love from Gen Z’s. Its CREAMi and SLUSHi products are a hit on TikTok, even roping in superstars like David Beckham, helping to drive its food appliances revenue 80% higher in 2024 after just 10% growth the year prior.

For Breville, keeping an edge won’t be easy, but its high-quality products provide a solid customer base. Innovation also remains key to navigating competition and keeping them at bay. SharkNinja has shown that innovation in today’s age, creating products that resonate with today’s generation can be a differentiator. The market is undoubtedly crowded but growing, meaning constant product development and innovative marketing are key to staying ahead

Financial Health Check

With a business like Breville, you’re unlikely to get anything extraordinary, but Warren Buffett has become the world’s greatest investor by owning ‘boring’ businesses over many years, especially ones that serve our everyday needs. Breville handed down its half-year earnings in February, showing solid ongoing performance.

In the first half of FY25, revenue rose 10.1% to $997.5 million, while net profit after tax jumped 16.1% to $97.5 million. That double-digit earnings growth was driven by strong demand across all regions, particularly in the Americas and Europe, while coffee machines remained a key driver. This shows a continued shift in consumer behaviour, where coffee consumption at home has become a preferred choice.

The company’s gross profit margin held firm at 36.7% highlighting Breville’s ability to hold pricing power and manage input costs, a key advantage for a premium brand. This means they remain in a strong position, generating healthy free cash flows and maintaining low levels of debt, giving it the flexibility to reinvest in innovation, expand into new markets, and return capital to shareholders. In line with the profit increase, Breville lifted its interim dividend to 18 cents per share, up from 16 cents last year, around a 1.19% payout.

There were some question marks over its guidance and Breville is also at the centre of the tariff turmoil currently grappling markets. They manufacture around 90% of their goods from China. So, in a strategic move, Breville pulled forward around inventory in the US early this year to beat incoming tariffs, meaning its full-year result won’t be affected, with Breville reaffirming its FY25 EBIT growth guidance of 5–10%. However, these heavy tariffs could dampen future earnings growth.

Breville has already begun to lay the groundwork for diversifying its manufacturing beyond China, but with sweeping tariffs across Asia, earnings for the years ahead could face some pressure. They will either have to absorb the hit to margins or pass costs on to customers through price increases, something that they can do with their premium positioning. Either way, it signals some challenges ahead.

Buy, Hold or Sell?

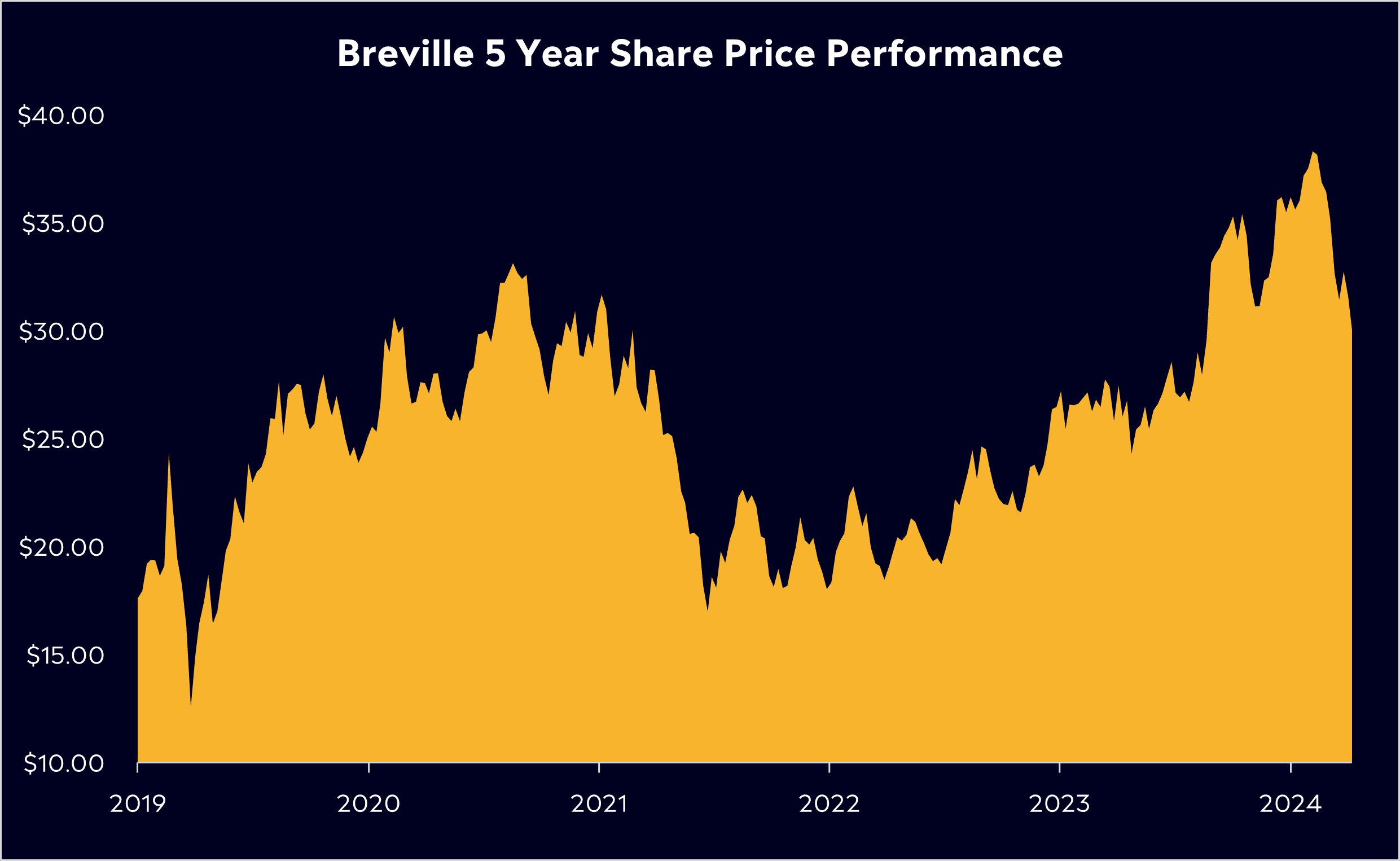

The tariff situation undoubtedly introduces uncertainty for Breville, but its early response shows a quality leadership team that can adapt quickly. For some context, the last time Trump declared a tariff war with China, Breville shares rallied 75% from July 2018 to January 2020. Having said that, Trump looks to be putting his foot on the gas this time, with a full-blown trade war a serious possibility.

Nevertheless, Breville has a healthy balance sheet, solid cash flow, a great R&D network, and is scaling globally while maintaining margins, a great combination for long-term investors. But the stock doesn’t exactly remain cheap at 27x forward earnings, above its 10-year average after a strong run higher since 2023.

According to Bloomberg’s Analyst Recommendations, Breville has 5 buy ratings, 7 holds, and 4 sells, with an average price target of AUD$34..27 signalling a potential upside of 25.5% from its last closing price.

Shares are down 20% YTD on tariff concerns and a possible trade war. Trump is looking to strong-arm nations, but he might be met with retaliation. It’s understandable that investors would be cautious about a brand like Breville on the surface, but it’s a premium and quality brand, which means it could pass on almost all of that additional cost inflation from the tariffs to its consumers. After all, it’s done exactly that before. Either way, it’s a quality stock that I believe is likely to navigate the next few years very well.

Explore Breville (BRG:ASX)

*Data Accurate as of 04/04/2025

eToro Service ARSN 637 489 466 promoted by eToro AUS Capital Limited ACN 612 791 803 AFSL 491139. Capital at risk. See PDS and TMD. This communication is general information and education purposes only and should not be taken as financial product advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial product. It has been prepared without taking your objectives, financial situation or needs into account. Any references to past performance and future indications are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.