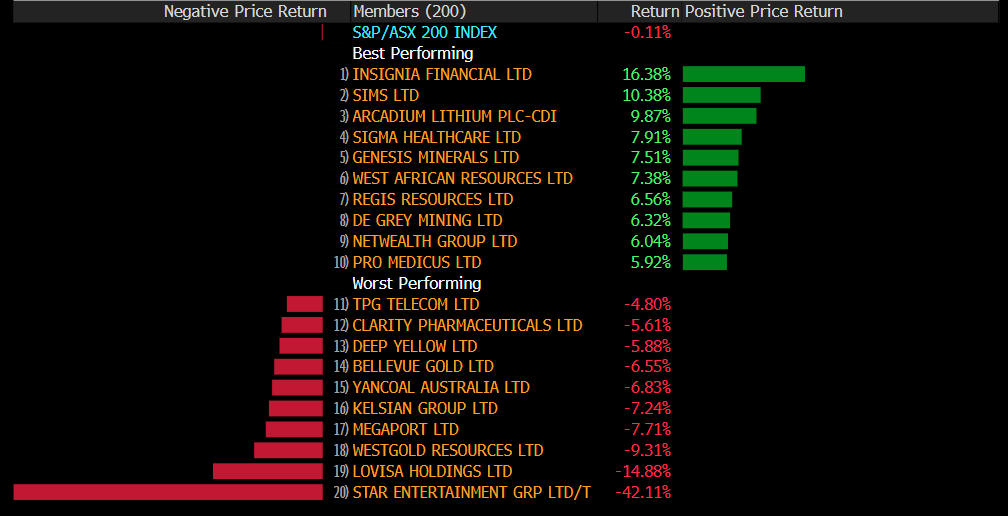

It was a good start to the first full trading week of 2025 on the ASX, with the index closing up 0.5%. Healthcare was the winner of the week, up 1.15%, but at the other end of the index, things kept getting worse for Star Entertainment, with shares tumbling 42%.

In the US on Friday, good news became bad news, with stronger than expected jobs data. December’s nonfarm payrolls report showed hiring increased by 256,000 for the month, well ahead of the 155,00 expected and up from November’s 212,000. That sent the S&P500 1.54% lower.

Earnings season kicks off again in the US this week, with major banks reporting their earnings on Thursday morning. JPMorgan, Goldman Sachs, Citi, and Wells Fargo are among the major US lenders reporting on Thursday morning.

3 things to watch for the week ahead:

- AU Unemployment – Thursday

Last month, employment rose more than expected to 35.6k, well up from the 12.1k gain in October, and the unemployment rate fell to 3.9% from 4.2%. That release showed that Australia’s job market continues to defy expectations. This week, we will get a further look into the labour market with the latest job data on Thursday.

At the time of writing, market pricing sees a 73% chance of an RBA rate cut in February, a significant change from where we were last year. Strong employment and lower unemployment will almost certainly cast doubt over a February rate cut. This week’s data will be key in the RBA’s next move. If the labour market doesn’t give up some of its gains, and the unemployment rate doesn’t pick up to above 4%, it’s very unlikely we’ll see a February rate cut.

The recent population growth through strong migration has boosted labour supply, but with net overseas migration set to slow down, new job additions are likely to slow, which is also supported by declining job ads. The market expects to see a 20k increase in jobs, with the unemployment rate picking up to 4%.

- US Inflation

The direction of US interest rates is undoubtedly up for debate, and this week, we’ll see that debate fuelled further by the release of US Inflation data. Market expectations are for headline inflation to rise to 2.9% from 2.7% in November, with core inflation set to stay unchanged at 3.3%. These numbers will likely support the case that we won’t see a Fed rate cut until the middle of the year, with markets not pricing a cut until June.

Trump’s inauguration is just around the corner, and that in itself brings plenty of uncertainty around inflation. In the latest FOMC minutes released last week, members expected inflation to keep moving toward 2%. However, they were keen to point to the effects of potential trade and immigration policy changes that could mean that returning inflation towards that 2% target could take longer than anticipated.

The shift in rate cut expectations has been big. Fed officials indicated they expect just two rate cuts across their eight meetings this year, down from four 25bps cuts in their September projections. Investors should also prepare for the scenario of no rate cuts. This is a slightly bold statement, but it is possible, especially if the US economy remains strong and Trump’s policies reignite inflation.

- TSMC Q4 Earnings

It was a great 2024 for Taiwan Semiconductor, with shares rising by 90%. It has already started 2025 on the front foot, gaining around 5%. It has the potential to extend those gains this week when it reports its quarterly earnings on Thursday.

TSMC works with some of the biggest names in the world: Apple, AMD, and, most importantly, Nvidia. They work with these names because they are the leaders in advanced chip-making capabilities. As the demand for AI chips continues to grow, alongside Nvidia’s dominance within the AI space, TSMC has seen huge demand, driving revenue and earnings.

TSMC’s dominance in advanced chipmaking may help to shield it from any tariff changes or trade policy shifts following the re-election of Donald Trump. But, it is still an uncertainty that investors have to contend with. Near-term profitability could face pressure as the company increases mature-node fab utilisation and seeks additional US subsidies to expedite its capacity expansion in the region. Markets expect earnings of USD$2.16, signalling 50% growth year over year, with revenue of USD$26.1 billion.

*All data accurate as of 13/01/2025. Data Source: Bloomberg and eToro

Disclaimer:

This communication is general information and education purposes only and should not be taken as financial product advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial product. It has been prepared without taking your objectives, financial situation or needs into account. Any references to past performance and future indications are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.