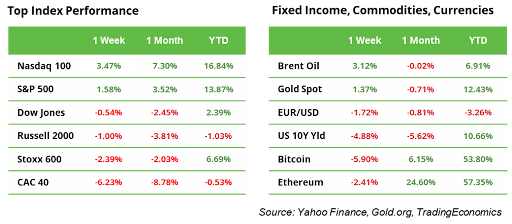

Divergence between US and Europe

The Nasdaq 100 and S&P 500 indices eked out new record highs on the back of AI announcements by Apple and a 3.3% inflation number for May, flat on the month for the first time in two years. The Fed’s dot plot guiding for one rate cut in 2024 and four in 2025 was dovish enough to lead US 10-year interest rates to fall from 4.43% to 4.21%. In Europe, the STOXX 600 Index shed 3%, mainly caused by the surprise election announcement in France after a sweeping win for Le Pen over Macron at the European Parliament vote. Investors feared that a far-right government might nationalize certain companies. Risk premiums for French bonds were elevated, and the EUR/USD exchange rate declined from 1.09 to 1.07.

This week will be light on data. We will see US retail sales, UK inflation, BoE rate decision, EU PMI, and Japan inflation. Wall Street will be closed on Wednesday due to the Juneteenth holiday. Derivatives markets are preparing for the ‘triple witching hour’. Index futures, index options, and stock options will all expire on Friday, including some of Roaring Kitty’s $GME options.

Will we face a new European debt crisis?

French national elections will be held in two rounds on 30 June and 7 July. Should Le Pen’s party win, she may nationalize motorways as part of her campaign. Infrastructure stocks like Vinci and Eiffage were sold off by more than 15%, followed by partly state-owned utility companies and banks. Arguably even more important, the spread between French and German 10-year government bonds hit 80 basis points for the first time since the European debt crisis in 2011. Markets will keep a close eye on contagion to highly indebted European countries like Italy and Spain. Market participants will also seek an ECB response, hoping Lagarde will reiterate Draghi’s “whatever it takes.”

Will we see a repricing of corporate bonds?

The surprise developments in France put a focus on potentially underestimated risks at large. This may draw attention to relatively low-risk premiums on speculative-grade corporate bonds. The Fed of St. Louis’ High Yield Index shows these bonds (credit rating ‘B’) are currently priced at only 7.5%, compared to 6% for the lowest tier of investment-grade bonds (‘BBB’). Historical data shows that the effective yield may spike up pretty quickly once investors start demanding higher compensation for the risk they are running.

Source: Federal Reserve Bank of St. Louis

Mixed macro-signals from China

Industrial production increased by 5.6% compared to the previous year, falling short of the expected 6%, and slowed down from the previous month’s 6.7%. Retail sales recovered more strongly than expected, rising by 3.7% compared to the forecasted 3%, after hitting a 15-month low of 2.3% in the previous month. Consumption has not been revived to pre-pandemic levels yet. The persistent real estate crisis continues to suppress economic growth.

US retail sales in May: further evidence of economic weakness?

Private consumption in the USA accounts for over two-thirds of nominal GDP, making retail data critically important for investors. We want to know if growth continued to slow in May. Another decline could indicate an economic slowdown and increase recession risks. This, in turn, could raise the possibility of an earlier interest rate cut. In April, retail sales rose by only 3.0% compared to the previous year, well below the long-term average. High interest rates are severely impacting consumption. Despite inflation falling more than expected, it has not been fully defeated, so the Fed feels no pressure to lower borrowing costs. At the same time, the labor market remains surprisingly robust: there is full employment and wages are rising significantly. This real wage growth increases purchasing power and could boost consumer spending.

Eurozone PMI: upturn thanks to strong service sector

The Eurozone has emerged from recession for three months. Composite PMI has trended up to 52.2 recently, but analysts expect 51.5 for June. Focus will be on the gap between Manufacturing PMI (seen at 48.5) versus Services PMI (seen at 52.7).

Earnings and events

Golden Goose, maker of $500 customisable luxury sneakers, is seeking at least $2 billion in an IPO in Italy on Friday. Earnings we will see from home builders Lennar ($LEN) and KB Home ($KBH), together with consultancy firm Accenture ($ACN) and supermarket chain Kroger ($KR), that is still battling to acquire Albertsons ($ACI).