Bye H1, hello H2

The first half of the year ended with the S&P 500 up 15%, the Nasdaq 100 up 17%, the Dow Jones 30 up 4%, and the small-cap Russell 2000 up 1%. The S&P 500 technology sector rose 21% and dominated from January to June, with communication services being the only other sector outperforming the broader index. Gold climbed 12%, Brent oil advanced 12%, and the Dollar Index gained 4.5%. Europe and Emerging Markets (both up 7%) felt the strength of the US market. China’s local Shenzhen Index lost 6%, the French CAC40 shed 1% due to election fears, and the S&P 500 real estate sector was the only negative sector, down 5%. Bitcoin lost part of its gain in June but still ended up 45%, making it the best-performing asset.

This week is all about fresh US jobs data and snap elections in both France and the UK. The US markets will be closed for Independence Day. The lack of any other high-profile events will put a spotlight on car sales reports for the first six months of the year, with particular focus on struggling brands like Tesla and Volkswagen. Penny stock Polestar will report earnings on 2 July as it tries to avoid being the next victim in the EV knockout race.

Consumer stocks raise concerns about US household strength

Nike lost $28 billion in market value in just one day after predicting an unexpected 10% sales drop for the upcoming quarter. It’s not an isolated case, as Walgreens, Levi”s, H&M, and L’Oréal have also flashed warning signals. Watch out for more as we anticipate the Q2 earnings season.

French elections: Le Pen’s far-right party comes in first in the 1st round

French elections are held in two rounds on 30 June and 7 July. The exit polls for the 1st round give 34% to Le Pen, 22% to Macron, and 29% to the leftist New Popular Front. The French voting system is somewhat complicated. In each constituency, the top two contenders advance to the 2nd round, joined by any candidate who has received at least 12.5% of the vote. Parties may withdraw candidates, for example, to try and block a far-right absolute majority. Expect markets to react nervously to any significant news. Watch the spread between French and German government bonds, as well as stocks of companies like BNP, SocGen, Vinci and Engie.

UK elections: How low will the Tories go?

On 4 July, Labour Party leader Keir Starmer is projected to win a landslide victory, with the only question remaining being how many seats the Conservative Party will continue to hold. Expect markets to have already priced in a substantial Labour win in full.

Resilient US labour market holds Fed back from rate cuts

Over the past six months, an average of 255,000 new jobs (Non-Farm Payrolls) have been created monthly. Friday’s release of June data is crucial: 200,000 jobs or more would signal a thriving economy, bolstering the “higher for longer” scenario. Expectations are set at 180,000 jobs, which would indicate a cooling labour market. However, a slump in the labour market is not necessary for investors to increase their bets on interest rate cuts for the second half of the year. In fact, a sustained period of weakness lasting several months would be fundamentally concerning.

ECB’s balancing act: reducing inflation and stimulating the economy

Monthly EU inflation data are due on Tuesday. Inflation in the EU has been sticky between 2.4% and 2.9% for the past seven months. June numbers may see pressure ease with an expected drop from 2.6% to 2.5%. Core inflation is anticipated to fall to 2.8% from 2.9%. Lower numbers would open the door for further interest rate cuts, providing relief to Europe’s cyclical and interest-sensitive stock market.

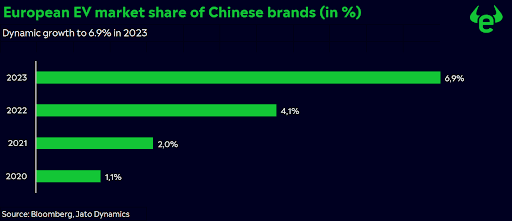

Electric vehicles from China: EU introduces punitive tariffs from 4 July

Power dynamics in the European electric vehicle market are shifting. The market share of Chinese brands increased to 6.9% in 2023, up from 4.1% the previous year (see chart). The EU accuses these brands of benefiting from unfair state aid and has proposed new, incremental, and brand-specific tariffs ranging from 17.4% for BYD to 38.1% for SAIC. Nevertheless, imposing tariffs as a shield for the domestic auto industry could backfire. The Chinese market is of existential importance for Western car manufacturers. Beijing has already announced retaliation, starting with an anti-dumping investigation into pork imports from the EU. Yet, both sides appear willing to negotiate.