Please see this week’s market views from eToro’s global analyst team. The full 5-pager includes latest market data, the house investment view, and ‘special’ focus on investment implications of Valentine’s Day.

Valentine’s Day investment thoughts

Valentine’s Day is the latest test of the resilient consumer, that is keeping the world out of recession. It’s the 5th biggest US consumer event of the year with avg. $182 spend. Candy the most common present but all-time-high cocoa prices making pricier. Other valentines related stocks, from flowers to cards, not well-represented, or good performing, in the stock market. The little-known ‘Valentines Day’ optimism technical effect can temporarily boost stock prices. See Page 4

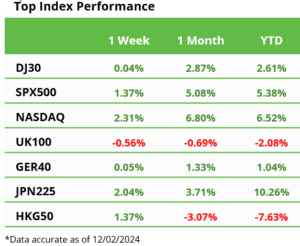

S&P 500 touches the 5,000 milestone

S&P 500 index hit psychological 5,000, up 20% from Oct, as Q4 earnings recovery broadens with high-profile DIS to ARM ‘beats’ taking growth to +8%. Services PMI drove US Q1 GDP NOWCast to big 3.4%. China stimulus hopes drove market up into the new year holiday. Investors rewarded dividend/buyback hikes from BP to F. SNAP leads disappointments See our 2024 Outlook HERE and twitter @laidler_ben. See Page 2

Productivity the only free lunch in economics

US seeing productivity boom driving ‘immaculate disinflation’ and helping S&P 500 earnings, with combo of rising wages, new tech adoption and government investment spending. See Page 2

Retail investors drive ‘overnight effect’

Most S&P 500 returns historically made in less-liquid overnight session rather than in day. And most powerful in those assets most-owned by retail investors from TSLA to GME. See Page 2

Crypto catalysts as Bitcoin ETF dust settles

Bitcoin spot ETFs are already proportionately larger than gold ETF peers, whilst Bitcoin halving, Fed rate cuts, and the spot ETH ETF deadline are the next big looming catalysts. See Page 2

Natgas risk/reward is looking up

Prices slump under $2.00/MMBtu that historically been tipping point for lower supply and stronger demand to rebalance as LNG booms. See Page 2

BTC relief rally extends to $48,000

Bitcoin (BTC) recovery rally extends as the new spot ETF inflows are some of the strongest across all the $10 trillion ETF universe. Whilst total digital asset trading rises for fourth month, to $1.4 trillion. Ethereum (ETH) Dencun upgrade coming March 13. CEO of miner HUT steps down. See latest Weekly Crypto Roundup. See Page 3

Mixed commodity week as oil and cocoa rise

Divergence from Brent oil rising over $80/bbl., on Middle East tensions, whilst the US natgas price slump deepened to 25-yr low under $2/MMBtu. Cocoa hit a new all-time-high price on West Africa supply disruption. Palladium prices fell below platinum for the first time since 2018 on ICE car catalytic demand concerns. See Page 3

The week ahead: Inflation, profits, Valentine

1) Potential Jan. US inflation (Tue) relief to <3%. 2) US earnings wind down w/ KO, MAR, ABNB, DE, AMAT and AIR.PA to SONY. 3) UK with inflation est. >4% and latest resilient GDP as BoE pushes back on early rate cuts. 4) Valentine Day (Wed) consumer test. Population and commodity giant Indonesia election. China NY holiday. See Page 3

Our key views: Outlook for a different 2024

We see a stronger but very different 2024. Lower inflation and coming interest rate cuts as growth slows, and the earnings outlook idiosyncratically accelerates. Will drive an investor rotation from 2023 US and big tech winners to rate sensitive losers from Europe to real estate. See Page 5