Please see this week’s market views from eToro’s global analyst team. The full 5-pager includes latest market data, the house investment view, and ‘special’ focus on investment implications of US and UK elections.

Investing through the US and UK elections

We look for lessons from Trump’ surprise victory in 2016 and the UK’s Labour’s party landslide win in 1997. Markets did well in both, despite policy differences. Shows election impacts may be overdone, as we overestimate politicians. Biden and Trump face off in replay of 2020 US election, but now better known, with greater constraints. UK investors should see comfort in parallels with Blair’ ‘New Labour’ 1997 victory. Defence, energy, infrastructure are potential winners. See Page 4

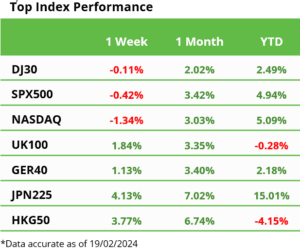

Stocks take bad inflation print in stride

US stocks were held back by a worse-than-expected 3% US inflation report. Whilst supported by a good US earnings season, with overall profits +9%. The JPY fell below 150, whilst Bitcoin surged 10%. AI optimism saw ARM surge, and helped drive NVDA to become the US’s 3rd largest stock. Buffett’s BRKb trimmed its big AAPL holding. See our 2024 Outlook HERE and twitter @laidler_ben. See Page 2

The tail-risk of an inflation comeback

Stocks ignore tail risk of US inflation rebound with economy strong. Bonds and dollar consider. Our prices tracker and 3% Jan. print flash yellow. Lot riding on productivity boom. See Page 2

Still cautious sentiment drives buy-the-dip

Our investor sentiment index still only neutral, a contrarian support to stocks and driver of buy-the-dip market support despite rising interest rate and valuation headwinds. See Page 2

A tale of two housing markets

US builders (PHM to LEN) soared as counter-intuitively benefit from high mortgage rates, whilst UK peers (TW.L to BKGH.L) need them to fall, despite similar markets. See Page 2

Europe’s carbon price perfect storm

ETS plunged on recession to lower natgas prices. Yet, many overhangs cyclical, and EU regulatory supply/demand squeeze is coming. See Page 2

Crypto market cap rallies back to $2 trillion

BTC soars over $50,000 with Nov. 21st $66,000 all-time-high in sight. As assets in new spot BTC ETF leaders IBIT and FBTC over $3 billion each, and ‘halving’ on horizon. ETH over $2,800 with BEN latest to file spot application. Took asset class mkt cap to $2 trillion. COIN results rebound. See latest Weekly Crypto Roundup. See Page 3

Commodity prices continues to struggle

Asset class hurt by the stronger dollar, rate cuts pushback, and China NY holiday. Brent firm over $80/bbl. as a ‘reflation hedge’, whilst natgas hit new lows, and EU carbon credits plunged. Cocoa and uranium rally continues, and palladium rebounds. Whilst ALB beats estimates despite lithium’s 78% YoY collapse. See Page 3

The week ahead: Presidents Day, China, NVDA

1) US Presidents Day (Mon) and China’s NY market reopening. 2) Key NVDA (Tue) results, w/ est. $20bn of sales, plus WMT, HD, BKNG, HSBC, GLEN. 3) US, EU, UK, JP, AU flash PMI growth and inflation, with inflation stickier. 4) 2nd anniversary (Sat) of Russia invasion of Ukraine. Big CAGNY consumer event. WMT stock split. See Page 3

Our key views: Outlook for a different 2024

We see a stronger but very different 2024. Lower inflation and coming interest rate cuts as growth slows, and the earnings outlook idiosyncratically accelerates. Will drive an investor rotation from 2023 US and big tech winners to rate sensitive losers from Europe to real estate. See Page 5