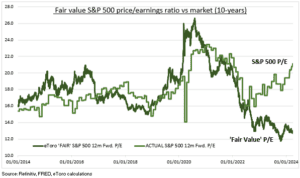

HEADWINDS: US valuation risks are rising again. The S&P 500 price/earnings ratio is now well above long term averages. And rising 10-yr bond yields widened the gap to our fair value P/E to a record 40% (see chart). Stocks have become less sensitive to rising yields over the past year, but there will still be a tipping point. US GDP growth ‘exceptionalism’ and concerns on higher-for-longer interest rates are pressuring up yields. Alongside a return of the catch-all ‘term premium’ of broader uncertainties from fiscal sustainability to election outcomes. This makes a Q1 earnings season recovery crucial, and supports our rotation to cheaper ‘insurance’ assets.

FAIR-VALUE: We use 10-yr US bond yields, corporate profitability, and long-term GDP growth estimates to estimate a ‘fair value’ S&P 500 (SPY) P/E ratio. It has a good long-term track record but this has broken down recently. The current 13x is low and a record 40% under the S&P 500 consensus 21x. It’s the biggest gap of the decade. And reflects the top-heavy market with ‘magnificent-seven’ concentration at records. And investor expectations for better earnings growth and potentially economic growth ahead. A 0.5% higher 10-yr bond yield cuts our P/E by 7%. A return to the long-term GDP outlook a decade ago (2.6% vs 1.8%) raises it 10%.

DOUBLE-FOCUS: It also reminds on the relative markets risk and reward. Tech sectors are the largest in US, already highly profitable, with already high valuations. They are well-supported, but the upside is now from elsewhere. We see an increasing rotation continuing to cheaper sectors, like financials (XLF) and to real estate (IYR). And to regions, like Europe (FEZ) and emerging markets (EEM). They have the most room for valuations to rise. They are also an ‘insurance’ to eventual valuation pressures if bond yields rise. And they have the double benefit of the most earnings upside to our base case of an economic soft landing and lower interest rates.

All data, figures & charts are valid as of 04/04/2024.