Summary

Investors been cautious to embrace the rally

We are seeing an ‘everything’ rally, of both bonds and equities, as the inflation and interest rate shock eases. Yet investors have been cautious to embrace it. Equity inflows are barely positive this year after big 2022 outflows. These small inflows are a contrarian positive for markets, and helps its risk/reward. With pressure now on investors to catch up, as fundamentals have improved, or use any inevitable weakness to add.

The ‘everything’ rally survives a big week

The markets strong start to year survived a huge event week. Perceived dovish interest rate hikes from US Fed, ECB, and BoE helped. Whilst IMF raised its global GDP forecasts, calming recession fears. Offset US 517,000 big payrolls surprise and weak Tech giants AAPL, AMZN, GOOG results, even as META cut costs and launched a 10% buyback plan. F followed TSLA in cutting EV prices. See our 2023 Year Ahead HERE. See video updates, twitter @laidler_ben. We are back in January 2023. Happy holidays!

Improving global growth drives markets

IMF global update validates the less-bad macro. They raised their GDP growth forecast this year by 0.2% to 2.9%, after three straight cuts. It’s the fundamental support to recent rally.

Fear of missing out on the ‘everything’ rally

Markets had one of best starts to year ever, confounding consensus. Fundamentals and history are on your side, but return pace will slow. January often sets year tone.

Hong Kong leads global markets

Hong Kong (HKG50) is world’s fifth largest equity market, led rally, but often misunderstood with mix of mainland and local stocks.

Who owns what and why it matters

Company ownership matters and differs around world and across sectors. Families, founders, and SOE’, all drive governance and valuations.

Crypto assets price rally holds

Crypto assets held firm, with Bitcoin (BTC) nearing $24,000 and now up 40% this year, benefitting from broader global rally. Avalanche (AVAX) among top performers after recent AWS deal and first Intain institutional subnet. UK launched crypto reg proposals, Follows the EU’s MICA laws passage last year.

Commodities in the performance shadows

Another down week made commodities worst performing asset class this year, a reversal from 2022 leadership. Oil led energy down after no change at OPEC+ meeting and low expectations for Feb 5th next round of EU and G7 sanctions on Russia. EU. Ag prices did better as coffee and sugar rose on supply disruptions.

The week ahead: hopefully a quieter week

1) Q4 earnings home stretch now, with overseas focus. DIS, PEP, ULVR, AZN, BAT, BP. 2) Australia RBA to raise more with inflation running hot. 3) UK Q4 GDP report to make a recession ‘official’. 4) Biden State of Union speech with debt ceiling deadlock. Plus Fed Powell speaks.

Our key views: A clear but gradual recovery

Lower inflation sees near interest rate cycle top. Reopening China cuts recession risk. Lower bond yields drive tech relief. Sticky inflation or higher for-longer Fed mistake the risks. See a gradual recovery with plenty bumps in road. Focus cheap and defensive assets. Higher risk crypto, tech, small cap as inflation fall picks up.

Top Index Performance

| 1 Week | 1 Month | YTD | |

| DJ30 | -0.15% | 0.88% | 2.35% |

| SPX500 | 1.62% | 6.20% | 7.73% |

| NASDAQ | 3.31% | 13.60% | 14.62% |

| UK100 | 1.76% | 2.63% | 6.04% |

| GER30 | 2.15% | 5.93% | 11.15% |

| JPN225 | 0.46% | 5.91% | 5.42% |

| HKG50 | -4.53% | 3.19% | 9.50% |

*Data accurate as of 06/02/2023

Market Views

The ‘everything’ rally picks up steam

- The markets strong start survived a huge event week. Boosted by perceived dovish rate hikes from Fed, ECB, and BoE. Whilst IMF raised GDP estimates, calming recession fear. Offset big US payrolls surprise and AAPL, AMZN, GOOG results weakness, even as META cut costs and launched a 10% buyback plan. F followed TSLA in cutting EV prices. See our 2023 Year Ahead View HERE.

Improving global growth drives markets

- The IMF global update validates the less-bad macro outlook. They raised their GDP growth forecast this year by 0.2% to 2.9%. This better tone comes after three straight outlook cuts. It’s driven by a combo of resilient consumers, China’s reopening, and less inflation. It’s the fundamental support to global equities’ recent rally.

- The caveat is that global growth is low vs a long term 3.8% average, with inflation high at 6.6%. And vulnerable with risks skewed to downside. Emerging market is the relative bright spot, and a top equity performer this year. Its GDP growth likely already bottomed last year. Overall, be invested but risk conscious.

Fear of missing out on the ‘everything’ rally

- Global equities had one of their best starts to the year ever, confounding consensus. Both history and the fundamentals remain on your side, but the returns pace will slow. January often sets the tone for the year, with back-to-back down years rare. The fundamentals have become less bad, from China’s reopening to falling US inflation.

- Was all that needed with market pessimism so high. These remain big supports but returns pace will inevitably slow. There will be bumps ahead. We stay positive, but are ready for lower returns and more cross-asset divergence ahead.

Hong Kong leads global markets

- Hong Kong (HKG50) is world’s fifth largest equity market and led recent global equity rally. It’s the gateway to China, which is reopening its economy, supporting its huge property sector, and easing its tech crackdown. It traces its roots back to 1891, a century longer than mainland exchanges.

- This gives it a unique and confusing makeup. Two thirds the Hang Seng index is mainland stocks, with other third HK focused. It’s led by financials (34%) and tech (30%) sectors. Institutional investors dominate. Its dollar linked, with HKD pegged to USD since 1983.. It’s still on an undemanding 10x P/E valuation and a 3% dividend yield.

Who owns what and why it matters

- Company ownership matters and differs around the world. Understanding owners incentives and time frames is important. It helps explain key issues, from rise of governance issues and share buybacks to the valuation gap on many markets.

- Institutional investors and atomised shareholder bases dominate in ‘Anglo-Saxon’ markets, even as passive investment flows have surged. Whilst the State and Families are more important in Europe and especially in emerging markets. Differences are very also big across global sectors.

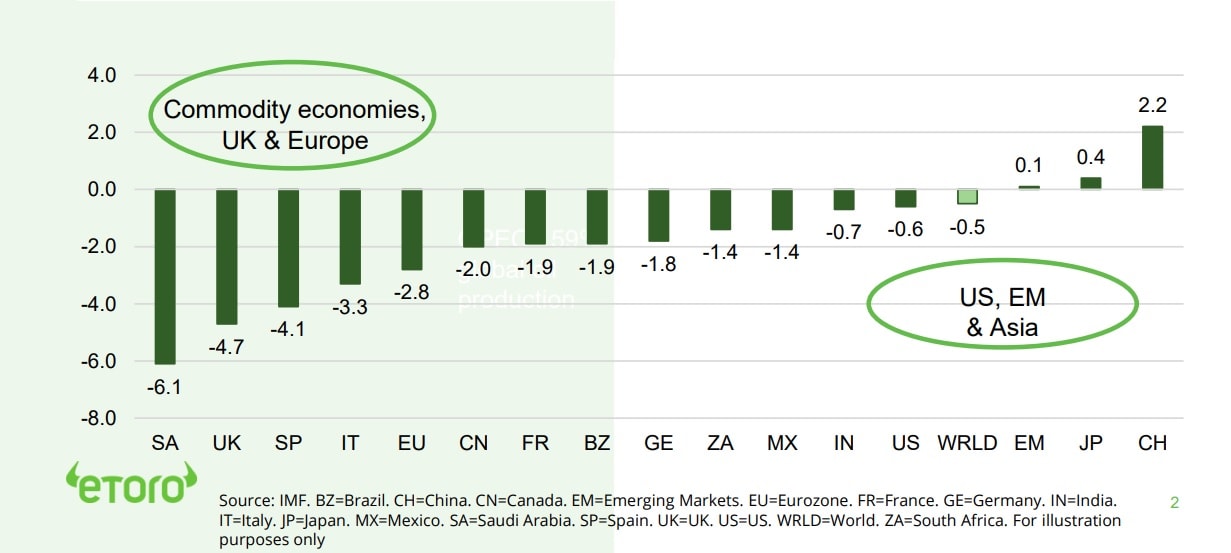

The GDP slowdown (2023 – 2022 GDP Growth, pp)

Crypto assets price rally holds

- Crypto assets stayed firm, with Bitcoin (BTC) nearing $24,000 and up 40% this year. Whilst Ethereum (ETH) nears $1,700. Both boosted by the improving global macro outlook, as inflation eases and central bank rate hikes decelerate. Has made crypto by far the nest asset class performer of 2023 after its big falls of last year.

- Avalanche (AVAX) among top performers of week. It benefitted from recent Amazon Web Services deal. Now from Intain as first institutional subnet.

- The UK government launched a consultation on its crypto regulation proposals, set to end April 30th. Follows EU’s MICA laws passage last year.

Commodities in the performance shadows

- Commodities again saw a down week, and were in the shadow of the broader markets rally. It is the worst performing asset class this year, a reversal from its 2022 leadership position.

- Energy slipped as Brent oil fell after no-change at the OPEC+ meeting and low expectations ahead of the coming February 5th next round of EU and G7 sanctions on Russian energy. EU natgas gains were more than offset by further US falls.

- Agricultural prices were led higher by supply fears. Sugar rose to a six year high as number 2 producer India set for a production shortfall. Similarly arabica coffee rebounded from recent lows as Brazil production forecasts were slashed.

US Equity Sectors, Themes, Crypto assets

| 1 Week | 1 Month | YTD | |

| IT | 4.21% | 16.36% | 15.76% |

| Healthcare | -0.06% | -1.00% | -1.41% |

| C Cyclicals | 2.54% | 18.09% | 17.66% |

| Small Caps | 3.88% | 13.41% | 12.73% |

| Value | 0.25% | 3.03% | 2.79% |

| Bitcoin | 0.01% | 39.97% | 40.92% |

| Ethereum | 2.58% | 36.52% | 38.22% |

Source: Refinitiv, MSCI, FTSE Russell

The week ahead: time for a quieter week

- Q4 earnings season rolls on, with a more international focus. US see’s Disney, Pepsi, AbbVie and Paypal. International heavyweights Unilever, Astra Zeneca, Linde, BP, Total, BAT, and Toyota.\

- The Central Bank meeting pace now eases off, but Australia’s RBA could do more than a 0.25% move in its 9th hike from current 3.1% with latest headline inflation rising 7.8% and not easing off.

- The UK is the ‘sick man’ of Europe with inflation at 10.5% and Friday’s GDP report set to see a second straight quarterly GDP fall. Typically this is the official sign of an economic recession.

- Biden’s 2nd State of Union (Tue) to US Congress to focus on Ukraine war, US debt ceiling, cooling growth and inflation, amidst political partisanship. Fed’s Powell speaks (Tue) to DC Economic Club.

Our key views: A clear but gradual recovery

- Consistently lower inflation gives visibility on the interest rate cycle top. Whilst the reopening of China cuts global recession risks. Lower bond yields drives relief for the key tech sector. Sticky inflation or higher-for-longer Fed mistake the risks.

- We see a gradual market recovery with the low in, but plenty of bumps in the road. Focus cheap and defensive assets, from high dividend, to healthcare, and UK. With higher risk crypto, tech, and small cap as the inflation fall picks up and de-risks markets. Overseas markets to lead the US. Commodities and the dollar to take a performance back seat.

Fixed Income, Commodities, Currencies

| 1 Week | 1 Month | YTD | |

| Commod* | -4.07% | -0.96% | -5.08% |

| Brent Oil | -7.41% | 1.55% | -7.18% |

| Gold Spot | -2.59% | 0.38% | 2.60% |

| DXY USD | 1.04% | -0.85% | -0.51% |

| EUR/USD | -0.64% | 1.46% | 0.90% |

| US 10Yr Yld | 1.19% | -3.89% | -35.58% |

| VIX Vol. | -0.97% | -13.25% | -15.41% |

Source: Refinitiv. * Broad based Bloomberg commodity index

Focus of Week: the building ‘pain trade’ is positive

Lacklustre fund inflows are positive for markets

We examine exchange traded funds (ETFs) and mutual fund flows this year for insight into investing trends and emerging themes, as the passive universe continues to boom. These flows are a good proxy for broader investor flows. They have been a fraction of the dramatic moves seen last year and are significantly lagging the strong markets performance this year. This is a growing ‘pain trade’ for many. It is a significant technical support to markets, with investors set to follow the rally or buy any coming dip.

ETFs are leading the way as their assets rise above $9 trillion

The total assets under management in exchange traded funds (ETFs) globally is now estimated at over US$9.0 trillion, across 9,500 funds. This is near double the level of only five years ago as investors have been attracted to their low fees, tax efficiency, liquidity, and instant diversification. Whilst the US dominates at near 70% of ETF total assets, the industry growth is being led by international markets.

Seeing ‘everything’ rally, of both bonds and equities, as inflation and interest rate shock eases

The ‘everything’ rally this year has encompassed most asset classes, as 2022’s inflation and interest rate shock eases and the world’s second largest economy reopens. Global equities are up 9% this year, global bonds around 3%, the dollar down 2% against overseas currencies, and crypto is up over 40%. Only broad commodities are down (-3%). The speed of the rally has broken records. It’s the second biggest start to the year of the past 30 years for the S&P 500 and the biggest since 2001 for the tech-driven NASDAQ.

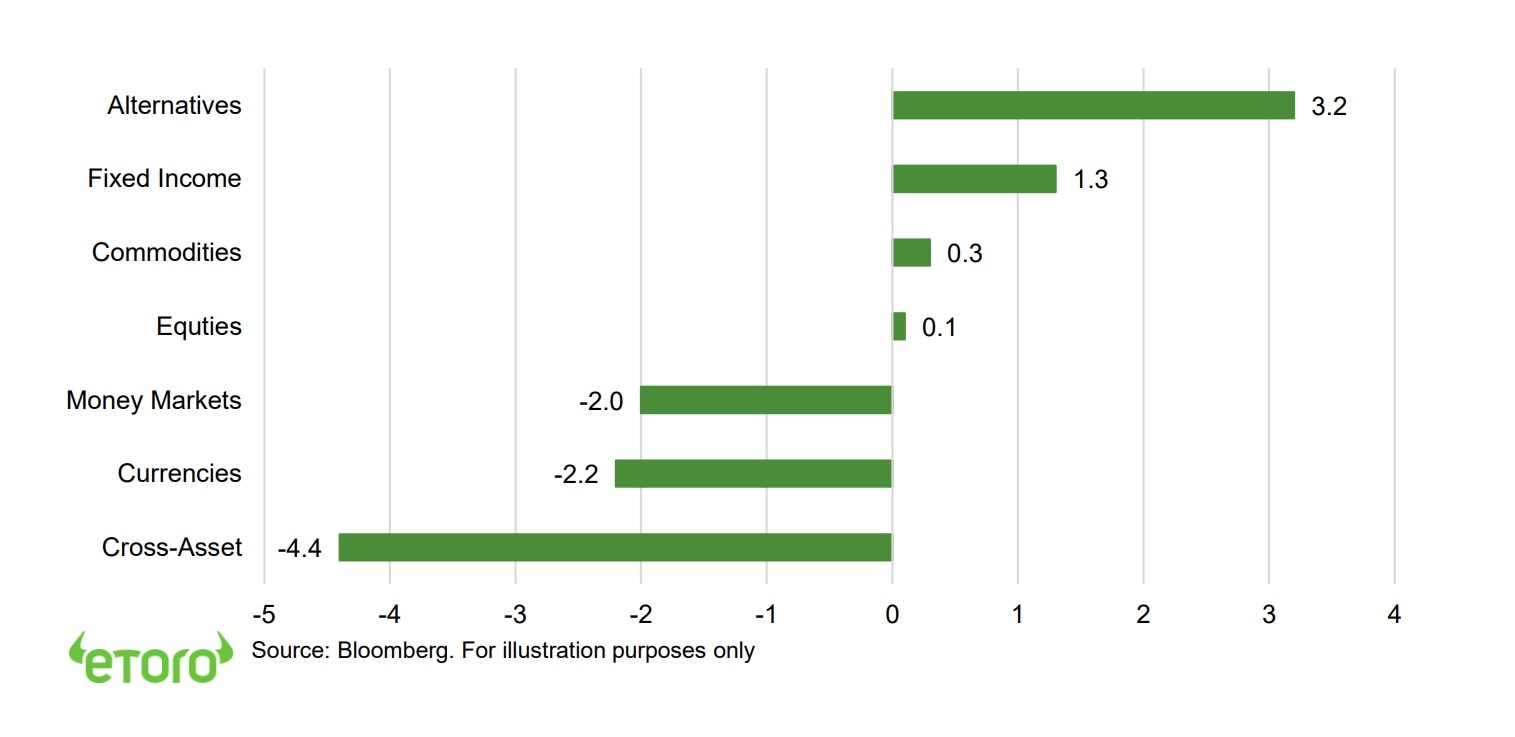

Yet investors have been cautious to embrace it

Equity inflows have been anaemic at only 0.1% of total assets (see chart) and a drop in the ocean versus the near $200 billion outflows last year. Within this, Europe (+4.1% of assets) has led, followed by emerging markets (+2.8%). Money markets have been reduced, after the strong $170 billion inflows of last year. This seems to have benefitted fixed income this year, which has seen the strongest inflows of major asset classes. Among currencies, Japan inflows have surged (+16% of AUM), on expectations for BoJ to tighten policy. Whilst industrial metals (+14%) have bucked the commodity fund outflows given China’s reopening. The strong cross-asset outflows likely reflect the historic drawdown seen to 60/40 portfolios last year.

This ‘pain trade’ helps the market risk/reward going forward

This is a classic ‘pain trade’. Investors are cautiously positioned in the face of this strong rally and less-bad fundamentals. If these remain supportive, investors will increasingly be dragged in, adding further fuel to the rally. If it falters, they may support it on the downside, using as an opportunity to cut underweights. The latest BAML fund managers’ survey shows very big underweights in US equities and high cash levels.

Global net fund inflows year-to-date as % of total assets

Key Views

| The eToro Market Strategy View | |

| Global Overview | Aggressive Fed interest rate hiking cycle and stubborn inflation boosted uncertainty, recession risk, and hit markets. We see this gradually fading in 2023, with global growth stressed but resilient, inflation pressure slowly easing, and valuations now more attractive. Focus on cheap and defensive assets for a gradual ‘U-shaped’ market recovery. |

| Traffic lights* | Equity Market Outlook |

| United States | World’s largest equity market (60% of total) seeing slowing but resilient GDP and earnings growth. Valuations led the market rout, and now below average levels, and are supported high company profitability and near peaked bond yields. Fast Fed hiking cycle boosted recession risks. Focus on cash-flows defensives, like healthcare and high dividend. Big-tech supported by defensive growth. See gradual ‘U-shaped’ rebound as inflation slowly falls and de-risks market. |

| Europe & UK | Favour defensive and cheap UK equities (‘Economies are not stock-markets’) over high risk/high return continental Europe. Recession risks high with Russia and energy crisis, threatening to overwhelm ‘buffers’ of rising fiscal spending (defence and refugees), low interest rates (slow to raise ECB), and weak Euro (50%+ sales from overseas). Equities partly cushioned by lack of tech, and 25% cheaper valuations vs US. Favour cheap and defensive UK over Continent. |

| Emerging Markets (EM) | China, Korea, Taiwan dominate EM (60% wt.), and more tech-centric than US. Positive on China as economy reopens, cuts interest rates, and eases tech regulation crackdown. Valuations 40% cheaper than US and market out of favour. Recovery helps global sectors from luxury to materials. Broader EM needs weaker USD and peak US rates catalyst. |

| Other International (JP, AUS, CN) | Canada and Australia benefit from strong equity market weight in commodities and financials, if global growth resilient and bond yields risen. Japanese equities among cheapest of any major market, benefit from weaker JPY and with low inflation, offsetting structural headwinds of low GDP growth, an ageing population, and world’s highest debt. |

| Traffic lights* | Equity Sector & Themes Outlook |

| Tech | ‘Tech’ sectors of IT, communications, consumer discretionary (Amazon, Tesla), dominate US and China. Hurt by higher bond yields and above average valuations. But structural stories with good growth, high margins, fortress balance sheets support some. ‘Big-tech’ attractive new recession defensives. ‘Disruptive’ tech is much more vulnerable. |

| Defensives | Core positions as macro risks rise and bond yields are better priced. Consumer staples, utilities, real estate attractive defensive cash flows, less exposed to rising economic growth risks, and robust dividends. Offset impact of higher bond yields. Healthcare most attractive, with cheaper valuations, more growth, some rising cost protection. |

| Cyclicals | Higher risk cyclical sectors, like discretionary (autos, apparel, restaurants), industrials, energy, and materials, are cheap and attractive if see a ‘slowdown not recession’ scenario. Are select but high risk opportunities from energy to financials stocks. With often depressed earnings, cheaper valuations, and have been out-of-favour for many years. |

| Financials | Benefits from high bond yields, charging more for loans than pay for deposits. Also one of cheapest P/E valuations, and with room for large dividend and buyback yields. But can be outweighed by high recession risks, with lower loan demand and higher defaults. Banks most exposed. Insurance and Diversifieds (like Berkshire Hathaway) the least. |

| Themes | We favour Value over Growth on GDP resilience, lower valuations, rising bond yields, under-ownership after decade under-performance. Dividends and buybacks recovering with cash flows. Power of dividends under-estimated, at up to 1/2 of total long term return. Secular growth of Renewables and Disruptive Tech investment themes. |

| Traffic lights* | Other Assets |

| Currencies | USD ‘wrecking ball’ driven by rising Fed interest rates and ‘safer-haven’ bid. Many DM currencies hurt by still low interest rates and struggling growth. ‘Reverse FX war’ interventions ineffective. Strong USD hurt EM, commodities, US foreign earners like tech. But helps big EU and Japan exporters. Stabler USD outlook as near top of Fed cycle. |

| Fixed Income | US 10-year bond yields risen above prior 3.5% peak, as Fed hikes continue aggressively and balance sheet runoff accelerates. Set to ease as recession risks rise and inflation expectations fall. Additionally US has a wide spread to other market bond yields, and structural headwinds of all-time high debt, poor demographics, low productivity. |

| Commodities | Strong USD and rising recession fears hit commodities. But still above average prices helped by GDP growth, ‘green’ industry demand, supply under-investment, recovering China, Russia supply crisis. Oil helped by slow return of OPEC+ supply and Russia 10% world oil supply problems. But commodities not to repeat their 2022 performance leadership. |

| Crypto | In the latest ‘crypto winter’ (16th crash for bitcoin) with dramatic and early asset class sell-off and later specific risk events from Luna to FTX. See long term asset class development with small size under $1 trillion, correlations low, regulation growing, development/catalysts continuing – Ethereum merge to proof-of-stake and coming BTC halving. |

| *Methodology: | Our guide to where we see better risk-adjusted outlook. Not investment advice. |

| Positive | Overall positive view, and expected to outperform the asset class on a 12-month view. |

| Neutral | Overall neutral view, with elements of strength and weakness on a 12-month view |

| Cautious | Overall cautious view, and expected to underperform the asset class on a 12-month view |

Source: eToro

Analyst Team

| Global Analyst Team | |

| CIO | Gil Shapira |

| Global Markets Strategist | Ben Laidler |

| United States | Callie Cox |

| United Kingdom | Adam Vettese Mark Crouch Simon Peters |

| France | Antoine Fraysse Soulier David Derhy |

| Holland | Jean-Paul van Oudheusden |

| Italy | Gabriel Dabach |

| Iberia/LatAm | Javier Molina |

| Nordics |

Jakob Westh Christensen |

| Poland | Pawel Majtkowski |

| Romania | Bogdan Maioreanu |

| Asia | Nemo Qin Marco Ma |

| Australia | Josh Gilbert |

Research Resources

Research Library

eToro Plus: In-Depth Analysis. Dive deeper into market insights: Read daily, weekly and quarterly summaries, catch up on the latest market trends and get the most recent, in-depth overview of markets.

Presentation

Find our twice monthly global markets presentation on the multi-asset investment outlook.

Webinars

Join our live Weekly Outlook webinars every Monday at 1pm GMT, or watch the replay at your convenience. Also see the other online courses and webinars.

Videos

Subscribe to our timely video updates on market moving events, and the ‘week ahead’ view

Follow us on twitter at @laidler_ben

COMPLIANCE DISCLAIMER

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.