VIEW: Stocks had a blistering start to 2024, with the S&P 500 annualising its best year in 70. April has been more challenging, as expected, and we are on the verge of an overdue market ‘pullback’. The proximate cause is a reset of Fed rate cut expectations and higher bond yields. We see this as a healthy breather, with extended weakness to be bought. The twin bull market earnings growth and still-coming rate cuts pillars remain in place. And significant cash on the sidelines. Our focus is the cheaper and more economically sensitive sectors and regions, from financials to Europe. A short term contrarian signal is VIX volatility over the 1 STD level of 28.

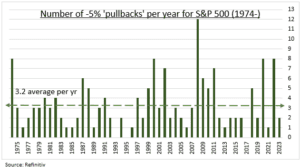

PULLBACK: Market sell offs come with the territory. There is no investment reward without risk. US stocks have seen long term average annual price returns of 10%, and stocks historically rise significantly more often than they fall. The S&P 500 has seen an average of three modest 5%+ ‘pullbacks’ a year (see chart). Much more often than 10% ‘corrections’. Or rare 20% ‘crashes’. Whilst the average intra-year S&P 500 drop has been a sizable -14%. Last year for example saw a -10% intra-year S&P 500 correction but ended up 24% for the calendar year. Whilst 2020 saw a much worse -34% intra-year plunge yet still ended up 16% for the full calendar year.

DRIVERS: Stock markets are in a short-term vice, squeezed three ways. 1) A repricing of later and lesser Fed rate cuts. With GDP growth stronger and inflation stickier. Driving bond yields higher and especially impacting those with high valuations, like tech (IYW), or high debts, like real estate (XLRE). 2) High geopolitical uncertainties, from Ukraine to the Middle East, have contributed to the US dollar (DXY) rally and the VIX rebound to long-term average levels. 3) The weaker technical backdrop of sharply rallied markets, high investor sentiment, and a statistically overdue pullback. With weak mid-year seasonality now arguably being pulled forward into April.

All data, figures & charts are valid as of 16/04/2024.