Summary

Silver lining of a faster growth slowdown

IMF trimmed its global economic growth outlook, to 2.8%, and warned on downside risks from the banks ‘scare’. Could take 0.4% off growth. Europe and commodity exporters lead weakness, with Asia where rebound is. But the silver lining is potential for a faster inflation fall and nearer rate cuts. IMF see’s return to pre-pandemic low rate /low growth world. Supports long duration assets from big-tech to bonds and crypto.

Lower inflation and Q1 start helps markets

Broad stocks rise in a shortened week as US inflation fell for 9th straight month, and big US banks started Q1 results strong. This offset high recession and bank fears. Overseas stocks continued to lead up, and EUR/USD hit 1.10. TSLA cut prices again. LVMH surged on strong sales. BABA fell on Softbank’s sale plan. Buffett hiked Japan stakes. See 2023 Year Ahead HERE. Video updates, twitter @laidler_ben.

The stubborn inflation mirage

US inflation markets most important number. March prices rose a less-than-feared 5%, a 9th deceleration. Core price were a stickier 5.6% but our tracker shows less pressures.

Banking pressures are not over

March’ banking ‘scare’ may seem mostly behind us. But macro consequences of tighter lending conditions remain. History reminds these ‘scares’ can be big and global. @RealEstateTrusts

Small caps in the cross-hairs

Small caps uniquely exposed to GDP slowdown we see coming. Are more cyclical, less diversified, with more debt. Are c50% all jobs in economy but only 15% of the stock market.

Big change for world’s biggest commodity

Oil world’ most traded commodity and Brent its benchmark. US added to Brent for 1st time. Will lower its price and premium to WTI.

Ethereum rallies after Shanghai upgrade

Crypto asset class continued world-beating YTD rally. Bitcoin price rose above $30,000. Ethereum crossed $2,100 as the long-awaited PoS Shanghai upgrade completed and overhang sale fears were unfounded. TRON bucked the uptrend as Binance US delisted coin. Whilst LSE (LSEG) latest to look to launch Bitcoin futures.

Commodities recover as dollar falls further

Commodities gained again as dollar weakness extended, with DXY index now at 100 vs its 114 Sept. 2022 peak. Oil gained on outlook for a US petroleum reserve rebuild. But ag prices led up, with Arabica coffee soaring on big supply deficit forecast from LatAm, and sugar hit a 10-year high as India’s drought hit exports.

The week ahead: Q1 earnings, PMI’s, China

1) First full Q1 earnings week, from BAC to GS, and TSLA to NFLX. 2) US, EU, JP, UK, AU flash PMIs slowdown health-check. 3) A China Q1 GDP and March retail sales reopening rebound. 4) Plus UK double-digit inflation, hawkish ECB minutes, and the start of Fed May 3 ‘quiet period’.

Our key views: Accelerated macro outlook

Banking fears individual not systemic. But doing Fed’s job for it. Accelerating GDP and inflation slowdown and interest rate peak. See market recovery with bumps in road. Slowdown hurts earnings. Low yields help valuation. Focus cheap and defensive assets, from healthcare to big tech More cautious on cyclicals and banks.

Top Index Performance

| 1 Week | 1 Month | YTD | |

| DJ30 | 1.20% | 6.35% | 2.23% |

| SPX500 | 0.79% | 5.64% | 7.77% |

| NASDAQ | 0.29% | 4.24% | 15.83% |

| UK100 | 1.68% | 7.31% | 5.64% |

| GER30 | 1.34% | 7.04% | 13.53% |

| JPN225 | 3.54% | 4.24% | 9.19% |

| HKG50 | 0.53% | 4.71% | 9.19% |

*Data accurate as of 17/04/2023

Market Views

Lower inflation and Q1 start helps markets

- Broad stocks rise in short week as US inflation fell for a 9th month and big US banks JPM and C started Q1 results strong. This offset recession and bank fears. Overseas stocks led up, and the EUR/USD hit 1.10 as the dollar fell further. TSLA cut prices again. LVMH surged on strong sales. BABA fell on Softbank’s sale. Buffett hiked Japan stock stakes. See our 2023 Year Ahead HERE.

Stubborn inflation a mirage

- US inflation is the most important number in global markets. It drives everything from the Fed outlook to recession risks. March saw a better than-feared 9th inflation headline fall to 5%, even as core price rises were a stickier 5.6%. We see one final ‘insurance’ hike from the Fed on May 3rd.

- We see a quicker US inflation fall later this year driven by weaker economy, with our underlying prices tracker, from labour to housing, helping. The median indicator is -31% from its peak and – 4% since February. This could set markets up for a quicker V-shaped recovery as investors look to interest rate cuts later this year.

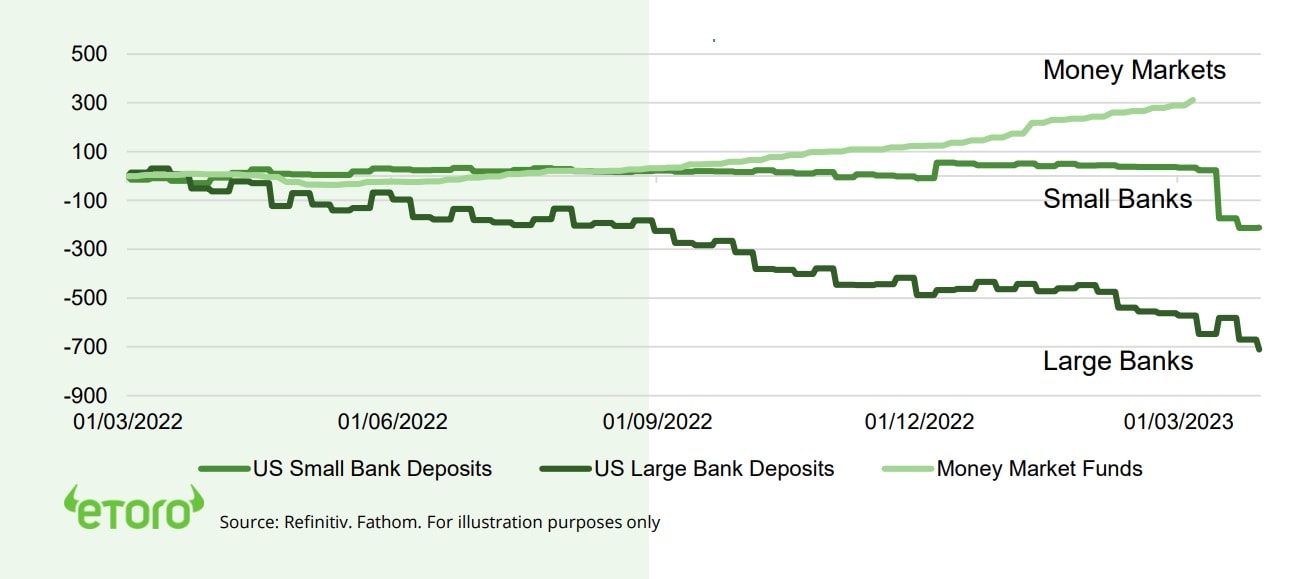

Banking pressures are not over

- March’ banking ‘scare’ may seem mostly behind us. But the macro consequences remain and history reminds these can be big and global. The $17.3 trillion US commercial bank deposits, equal to 65%/GDP, continue to slowly fall. This predated the SVB failure, driven by the Fed’s 5% policy rate. Depositors are moving to higher yield money market funds, which are at a record $5.2 trillion.

- Tighter liquidity is slowing loan growth, doing the Fed’s work for it. IMF forecasts show this could cut 0.4% from US and Euro GDP growth. It also presses banks to raise deposit rates, eating into their profit margins. There have been 151 systemic bank crises globally the past 50 years. @BigBanks.

Small caps in the cross-hairs

- Small caps uniquely exposed to faster GDP growth slowdown we see coming. As well as less small and mid-size bank lending as deposit outflows continue. Small caps more cyclical, less diversified, with more debt. Small cap benchmarks, Russell 2000 (where c.40% stocks loss making) and S&P 600 (only profit making stocks), are lagging but positive YTD.

- Both have similar valuations to large cap and twice profits growth. Superficially attractive but we see worse to come. A return to cyclicals, like small caps, needs a capitulation in growth expectations. This lies ahead. This has more impact for the economy than the stock market.

Big change for world’s biggest commodity

- Oil the world’ most traded commodity and Brent its main benchmark. North Sea Brent production has continued to fall, whilst US is now a net exporter. Brent price calculation will now include Midland Texas oil from Permian basin, to boost its liquidity.

- This change will start from June, with those futures contracts already trading. We expect a modest anchoring of Brent prices, with US Midland crude historically trading at a price discount to Brent, and therefore a smaller premium to WTI.

US bank deposit outflows vs money market inflows (US$ billions, since March 2022)

Ethereum Shanghai upgrade completes

- Crypto continued its asset-leading rally this year. Bitcoin (BTC) rose over $30,000, and its highest level since June 2022, boosted by positive markets and low US interest rate expectations.

- Ethereum (ETH) price crossed $2,100 as the long awaited Shanghai proof-of-stake (POS) upgrade completed and market fears on the overhang of $30 billion un-staked supply proved unfounded.

- TRON (TRX) bucked the price uptrend as the Binance US exchange delisted the coin. Whilst the London Stock Exchange (LSEG) became the latest to look to launch trading of Bitcoin futures.

Commodity rally as US dollar weakens

- The price recovery in commodities, the weakest asset class this year, continue. As the US dollar weakened, with Fed rate cut forecasts building, and China trade data positively surprising, reinforcing its gradual reopening recovery.

- Brent oil prices were among the main price gainers, further digesting OPEC’s recent 1mbpd surprise production cut, and with the US saying it would look to start rebuilding its depleted strategic petroleum reserve (SPR) this year.

- Agricultural prices were the major gainers. Arabica coffee led on forecasts for a bigger deficit after supply shortfalls in major LatAm producers. Whilst sugar prices hit a decade price high on drought-hit supply from no.2 producer India.

US Equity Sectors, Themes, Crypto assets

| 1 Week | 1 Month | YTD | |

| IT | 0.22% | 7.47% | 20.39% |

| Healthcare | 0.76% | 6.51% | -0.81% |

| C Cyclicals | 1.27% | 4.85% | 12.86% |

| Small Caps | 1.52% | 2.02% | 1.13% |

| Value | 1.00% | 5.38% | -0.49% |

| Bitcoin | 8.18% | 24.27% | 83.27% |

| Ethereum | 11.26% | 26.23% | 74.15% |

Source: Refinitiv, MSCI, FTSE Russell

The week ahead: Q1 earnings, PMI’s, and China

- The first full week of US Q1 earnings see’s rest of big banks, from BAC to GS, as well as big-tech’s TSLA and NFLX, plus consumer giants from JNJ to P&G. S&P 500 forecasts are for ‘less bad’ -5% YoY.

- April flash US, EU, Japan, UK, Australia PMI’s focus as recession fears rise and inflation slowly eases. Global PMI a resilient 53, consistent with solid 3% global growth. Weak manufacturing leads risks.

- Q1 China GDP growth to pick up to est. 3.2%, as economy reopens, and a welcome contrast to the building global slowdown. March retail sales est. +4.5% as the consumer-led recovery broadens.

- Other key events include a) a hoped for fall in UK’s world-leading 10.4% inflation. 2) ECB minutes as its hawkish stance helped drive big EUR rally. 3) Fed into quiet period (Fri) ahead of May 3rd meet.

Our key views: An accelerated macro outlook

- Banking sector fears are likely individual not systemic. Bank buffers are bigger now and the authorities response stronger. But this is doing the Fed’s job for it. By accelerating the GDP and inflation slowdown and the interest rate peak.

- See a V-shaped market recovery with plenty bumps in road. Faster slowdown hurts earnings. But lower bond yields helps valuation. Focus on cheaper and more recession defensive assets, from healthcare to derated big tech. More cautious on assets most exposed to recession risk, like cyclicals, small caps, and commodities. Or lower yields, like banks.

Fixed Income, Commodities, Currencies

| 1 Week | 1 Month | YTD | |

| Commod* | 1.49% | 5.09% | -4.42% |

| Brent Oil | 1.77% | 19.54% | 0.74% |

| Gold Spot | -0.30% | 1.20% | 10.25% |

| DXY USD | -0.50% | -2.05% | -1.87% |

| EUR/USD | 1.79% | 4.07% | 3.74% |

| US 10Yr Yld | 11.48% | 8.91% | -36.00% |

| VIX Vol. | -7.23% | -33.09% | -21.23% |

Source: Refinitiv. * Broad Bloomberg index. * Basis point

Focus of Week: A sobering but positive macro health check

A reminder of the economic, and earnings, slowdown to come. And why it could be positive

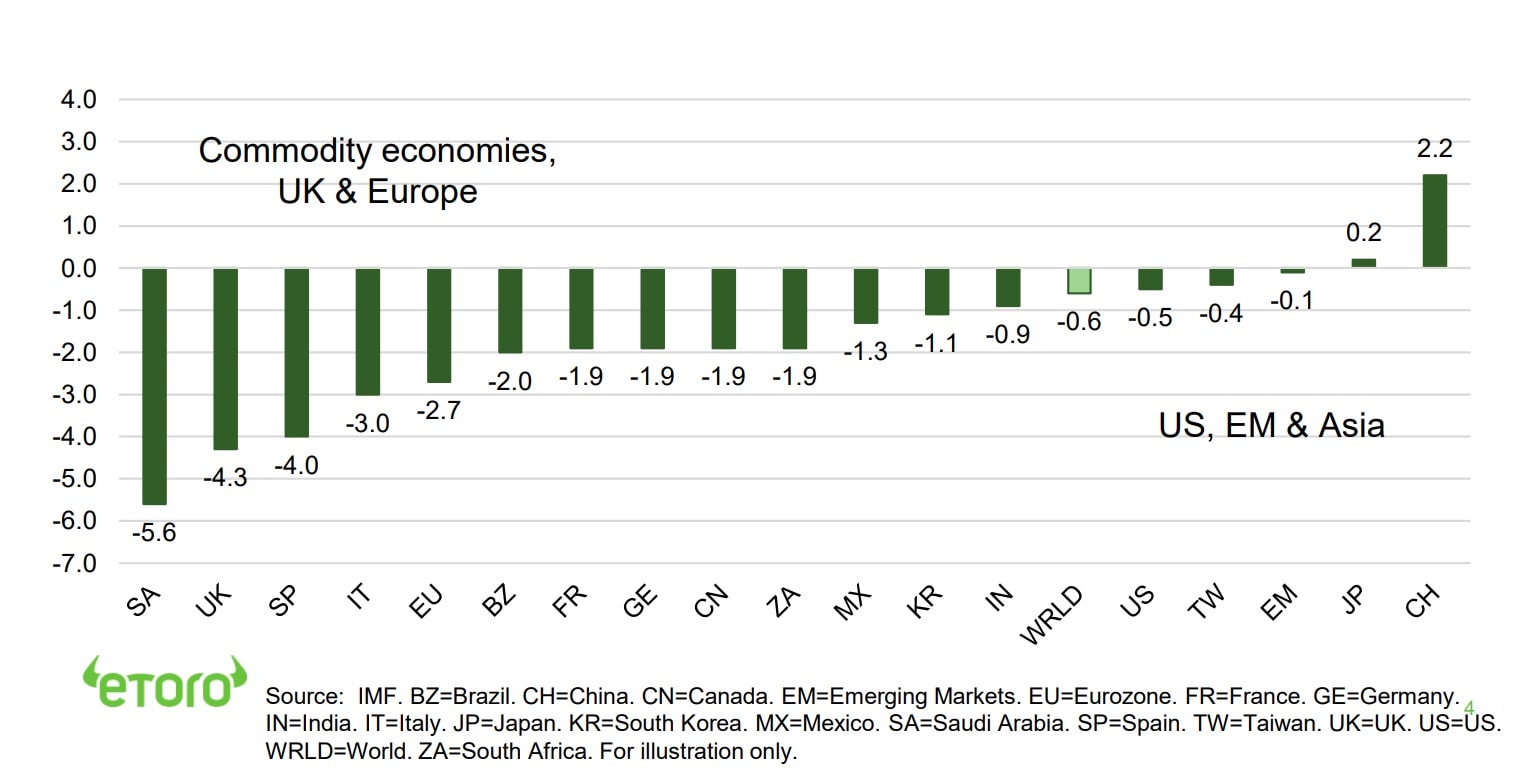

The IMF has laid out its latest economic outlook and the risks. They trimmed their GDP growth outlook for this year and highlighted the downside risks from tighter bank lending conditions. Economic growth this year is lower than last year everywhere except Asia (see chart). Most of this economic and earnings slowdown lies ahead and may be accelerated by recent bank scares. But this does not have to be negative. With forward looking markets focused on a faster inflation fall and earlier interest rate cuts. This is positive for long duration assets, from big tech and traditional defensive stocks that dominate stock markets, to bonds and crypto. But it’s a negative for cyclical assets, from consumer discretionary and small caps to commodities, which are more represented in the real economy and job markets. See our Q2 outlook video.

Commodity producers and Europe lead the GDP slowdown, with Asia the only growth exception

The IMF has trimmed its world economic outlook to 2.8% GDP growth this year and with an acceleration to 3% next. The slowdown this year is focused on richer countries – led by Europe – where the growth rate more than halves. China is the big exception. The IMF see a global commodity-driven inflation slowdown to 7% this year but still high 4.9% next. With inflation sticky and not returning to target 2% levels until 2025.

With banking sector risks potentially accelerating the growth slowdown further

The IMF show how tighter bank lending conditions could cut a further 0.3% from overall global GDP growth, focused on US and Europe and smaller companies. They see a ‘tricky phase’ of slow growth, heightened financial risks, and still high inflation. This has increased hard economic landing risks sharply.

See the greatest risks outside the banking system, in private markets to pension funds

The IMF separately published its global financial stability report. This delves into the twin risk of high inflation and high interest rates on markets. They are especially concerned by the non-bank financial system, from pension funds to private credit markets. Of the combo of high leverage, liquidity mismatches, and high interconnectedness. But are clear that its not 2008, with better preparation and authority tools.

And a longer-term return to the past of low growth and low interest rates

Controversially they also argue that once the current inflation pressures have eased, then interest rates are likely to revert to pre-pandemic lows. Reflecting sluggish underlying economic growth, demographic headwinds, and record high debt levels. This also supports our long-duration focus, from tech to bonds.

The GDP growth slowdown (2023 – 2022 GDP Growth, pp)

Key Views

| The eToro Market Strategy View | |

| Global Overview | Aggressive Fed interest rate hiking cycle, stubborn inflation, and now financial sector concerns, is accelerating our 2023 view. Of a quicker GDP slowdown, lower inflation, and a peaking Fed interest rate cycle. Will pressure earnings further but also lower bond yields and take pressure off de-rated valuations. We are invested, believing Oct 2022 was the low, and focus on cheap and defensive assets for a faster ‘V-shaped’ market recovery. See our Q2 Outlook HERE |

| Traffic lights* | Equity Market Outlook |

| United States | World’s largest equity market (60% of total) seeing slowing but resilient GDP and earnings growth. Valuations led the market rout, and now at average levels, and are supported high company profitability and near peak bond yields. Focus on cash-flows defensives, like healthcare and high dividend. Big-tech supported by defensive growth. See gradual ‘U-shaped’ rebound as inflation slowly falls and de-risks market and tech/small cap/crypto appetite. |

| Europe & UK | Favour defensive and cheap UK (‘Economies not stock-markets’) and continental European equities. Recession risk easing with lower natgas prices amd reopening China with high ‘buffers’ of rising fiscal spending (defence and refugees) and weak Euro (50%+ sales overseas). Even as ECB hikes aggressively. Equities cushioned by lack of big tech sector and 30% cheaper valuations vs US. Banks better capitalised and regulated but loans/GDP much higher. |

| Emerging Markets (EM) | China, Korea, Taiwan dominate EM (60% wt.), and more tech-centric than US. Positive on China as economy reopens, cuts interest rates, and eases tech regulation crackdown. Valuations 40% cheaper than US and market out of favour. Recovery helps global sectors from luxury to materials. Broader EM needs weaker USD and peak US rates catalyst. |

| Other International (JP, AUS, CN) | Canada and Australia benefit from strong equity market weight in commodities and financials, if global growth resilient and bond yields risen. Japanese equities among worlds cheapest but threatened by tightening monetary policy and stronger Yen with rising inflation and new BoJ governor. |

| Traffic lights* | Equity Sector & Themes Outlook |

| Tech | ‘Tech’ sectors of IT, communications, consumer discretionary (Amazon, Tesla), dominate US and China. Hurt by higher bond yields and above average valuations. But structural stories with good growth, high margins, fortress balance sheets support some. ‘Big-tech’ attractive new recession defensives. ‘Disruptive’ tech is much more vulnerable. |

| Defensives | More attractive as macro risks rise and bond yields better priced. Consumer staples, utilities, real estate attractive defensive cash flows, less exposed to rising economic growth risks, and robust dividends. Offset impact of higher bond yields. Healthcare most attractive, with cheaper valuations, more growth, some rising cost protection. |

| Cyclicals | High risk cyclical sectors – like discretionary (autos, apparel, restaurants), industrials, energy, materials, and small caps – have cheap valuations, many with depressed earnings, and have been out-of-favour for many years. But they are significantly exposed to rising recession risks. Some especially cheap (energy) or see growth recovery (airlines). |

| Financials | Current stresses likely individual not systemic. Post GFC reforms boosted capital and size/speed of authorities response. But outlook for 1) less GDP growth, 2) lower bond yields and interest rates, and 3) valuation sensitivity after recent surprises, worsens outlook. Insurance and Diversifieds (like Berkshire Hatheway) more defensive. |

| Themes | Dividends and buyback themes attractive with resilient cash flows, rising pay-outs, and investor search for defensives. Power of compounding dividends under-estimated, at up to 1/2 of total long term return. Small caps pressured by rising recession risk. Secular growth of Renewables and Disruptive Tech investment themes. |

| Traffic lights* | Other Assets |

| Currencies | USD ‘wrecking ball’ driven by Fed interest rates and ‘safer-haven’ bid. DM currencies hurt by still low interest rates and struggling growth. Strong USD hurt EM, commodities, US foreign earners like tech. But helps big EU and Japan exporters. See a stabler USD outlook in 2023 as near top of the Fed cycle and global risks remain high. |

| Fixed Income | US 10-yr bond yields supported around 4% by higher Fed rate hike and stickier inflation expectations. Set to ease as recession risks slowly build and inflation expectations gradually fall. US has wide spread to other market bond yields, and headwinds of high debt, poor demographics, and low productivity. 5% bill yields an attrative cash alternative. |

| Commodities | Strong USD and rising recession fears hit commodities. But still above average prices helped by GDP growth, ‘green’ industry demand, supply under-investment, recovering China, Russia supply crisis. Oil helped by slow return of OPEC+ supply and Russia 10% world oil supply problems. But commodities not to repeat their 2022 performance leadership. |

| Crypto | Potential ‘surpsise’ after dramatic and early asset class sell-off and later specific risk events from Luna to FTX. See long term asset class development with small size $1 trillion, correlations low, regulation growing, development/catalysts continuing – Ethereum merge to proof-of-stake and coming BTC halving. |

| *Methodology: | Our guide to where we see better risk-adjusted outlook. Not investment advice. |

| Positive | Overall positive view, and expected to outperform the asset class on a 12-month view. |

| Neutral | Overall neutral view, with elements of strength and weakness on a 12-month view |

| Cautious | Overall cautious view, and expected to underperform the asset class on a 12-month view |

Source: eToro

Analyst Team

| Global Analyst Team | |

| CIO | Gil Shapira |

| Global Markets Strategist | Ben Laidler |

| United States | Callie Cox |

| United Kingdom | Adam Vettese Mark Crouch Simon Peters |

| France | Antoine Fraysse Soulier David Derhy |

| Holland | Jean-Paul van Oudheusden |

| Italy | Gabriel Dabach |

| Iberia/LatAm | Javier Molina |

| Nordics |

Jakob Westh Christensen |

| Poland | Pawel Majtkowski |

| Romania | Bogdan Maioreanu |

| Asia | Nemo Qin Marco Ma |

| Australia | Josh Gilbert |

Research Resources

Research Library

eToro Plus: In-Depth Analysis. Dive deeper into market insights: Read daily, weekly and quarterly summaries, catch up on the latest market trends and get the most recent, in-depth overview of markets.

Presentation

Find our twice monthly global markets presentation on the multi-asset investment outlook.

Webinars

eToro CLUB members can join our live Weekly Outlook webinars every Monday at 1pm GMT. Also see the other online courses and webinars.

Videos

Subscribe to our timely video updates on market moving events, and the ‘week ahead’ view

Follow us on twitter at @laidler_ben

COMPLIANCE DISCLAIMER

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.