Summary

Our sector and style rotation roadmap

Market stress gave plenty of opportunity among equity sectors and investment styles last year. The performance gap between best and worst was an above average 105% for US sectors and 32% for styles. We see cautious High Dividends, Defensives, and Value still leading in 1H 2023. With room for a rotation to lagging higher risk Tech, Growth, Small Caps in 2H as lower inflation cuts interest rate and recession fear.

Starting year on the front foot

A positive 2023 start as US equities were helped by signs of a cooling jobs market, that tempered hawkish Fed views. 10-yr bond yields slumped and dollar was firm. Overseas equities did even better as EU inflation fell, and China pushed its reopening. TSLA slumped more as it missed delivery forecasts. Tech layoffs rose, from CRM to AMZN. Some small caps plunged, from BBBY to SI. 2023 Year Ahead View HERE. See video updates, twitter @laidler_ben. We are back in January 2023. Happy holidays!

The three drivers of the Q1 roadmap

Our positive outlook has three key drivers. 1) US/EU inflation and interest rate relief, 2) China successfully going-for-growth, and 3) a less bad outlook for huge global tech sector.

History is on your side

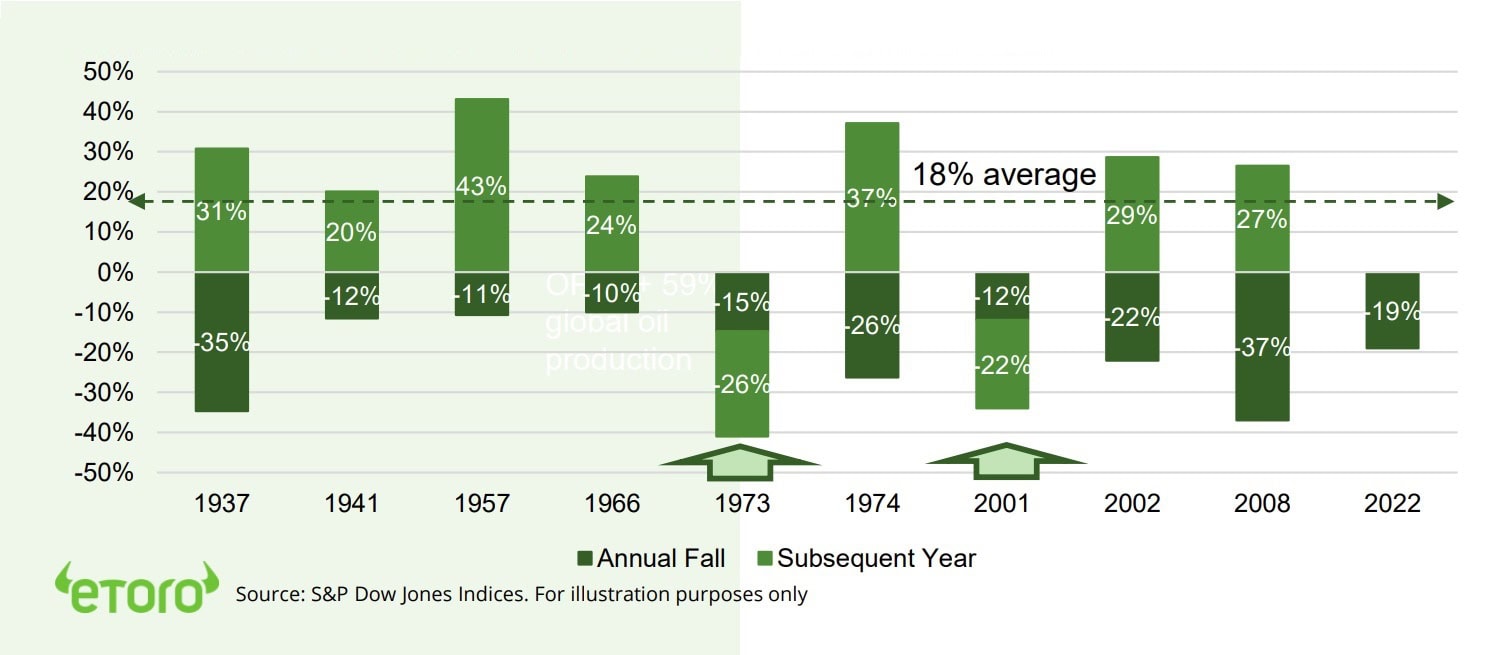

S&P 500 fell 19% in 2022. But consecutive down years rare. History is on your side with average 18% gain after big falls. January performance typically gives good lead on the year.

Why Japan matters in 2023

Global top 3 economy, market, and most traded FX is out of many investors minds. But its Christmas shock to continue in 2023.

Unlikely to see a commodities ‘three-peat’

Commodities the best asset class performer last two years. We are more cautious on 2023. We prefer related equities to physical.

Bitcoin puts terrible 2022 behind it

Bitcoin (BTC) and Ethereum (ETH) rose, resilient to market volatility and FTX fallout. Solana (SOL) led gainers, recovering some of its huge FTX driven losses, as new BONK ecosystem token soared. Crypto-bank Silvergate (SI) slumped on deposit outflows. Coinbase (COIN) reached a $100 million regulator settlement.

A weak start for commodities

A firm dollar and slumping energy prices saw commodities make a weak start to year. Natgas led energy down, on warm US/EU weather and Freeport LNG plant delays. Prices now 60% off highs. Lumber slump continued with US housing slowdown. Industrial metals, like copper, saw support from China reopening hope.

The week ahead: earnings and inflation duo

1) Global Q4 earnings season kicks off with US banks (Fri). S&P 500 est. EPS -4%. 2) Hope for a 6th straight fall in headline US inflation (Thu), to 6.5%. 3) The third anniversary of 1st covid death (Wed) comes as China goes-for-growth and accelerates its zero covid reopening.

Our key views: A gradual U-shaped recovery

Lower inflation is key to relief from double-barrel interest rate and recession pressures. We see a gradual and U-shaped recovery. 1H focus cheap and defensive assets, from healthcare to UK. Room for more aggressive 2H, as lower inflation de-risks markets. Stickier inflation or higher-for longer Fed mistake the big concerns.

Top Index Performance

| 1 Week | 1 Month | YTD | |

| DJ30 | 1.46% | 0.46% | 1.46% |

| SPX500 | 1.45% | -1.00% | 1.45% |

| NASDAQ | 0.98% | -3.96% | 0.98% |

| UK100 | 3.22% | 2.98% | 3.22% |

| GER30 | 4.93% | 1.67% | 4.93% |

| JPN225 | -0.46% | -6.91% | -0.46% |

| HKG50 | 6.12% | 5.48% | 6.12% |

*Data accurate as of 09/01/2023

Market Views

Starting year on the front foot

- It was a positive 2023 start as US equities helped by signs of a cooling jobs market, that tempered hawkish Fed views. 10-yr bond yields slumped and the dollar was firm. Overseas equities did even better as EU inflation fell, and China pushed its reopening. TSLA’s slump continued as missed delivery forecasts. Tech layoffs accelerated, from CRM to AMZN. Some small caps suffered, from BBBY to SI. See our 2023 Year Ahead View HERE.

The three drivers of the Q1 roadmap

- Our positive equity outlook has three key drivers. 1) Relief with the declining US/EU inflation and interest rate shock, whilst the consumer and corporate earnings stay relatively resilient. 2) A successful China zero-covid re-opening, as the world’s second largest economy goes for growth and gives insurance against a global recession.

- Also 3) less tech headwinds. IT, communications, and the tech-parts of discretionary are over 1/3 of global equities. They need to perform better for overall markets to rise. Tech companies are moving quickly to cut costs and the harsh valuation pressures should ease.

History is on your side

- The S&P 500 index fell 19% in a miserable 2022. But consecutive down years are rare, for equities and bonds. History is on your side with an average 18% S&P 500 annual gain after big falls. January performance typically gives a good lead on the full year. A fast inflation fall is the fundamental driver, and we believe underway.

- The S&P 500 seen nine prior 10%+ ’corrections’ over the past 75 years. Seven have seen subsequent positive years, averaging an 18% gain (see chart). The two that did not saw worse falls, of over 20%. These were in 1973, with the ‘Nixon shock’ and oil crisis, and 2001, with the ‘tech bubble’.

Why Japan matters in 2023

- Japan is a global top 3 economy, stock market, and most traded currency. It has traditionally been out of-mind for many. But it provided this year’s’ Christmas ‘surprise’, and this may continue in 2023.

- Bank of Japan (BoJ) widened its yield curve control band on 10-yr bonds to 0.50%. This first step to tighten monetary policy will continue as Kuroda retires in April, and the economy accelerates. This may attract capital back to Japan, including its $1.1 trillion of US treasuries, and further boost a still cheap Yen. A negative stock impact may be offset by low valuations and China’s recovery.

Unlikely to see a commodities ‘three-peat’

- Commodities were best performing asset last two years. And seems a 2023 consensus pick. We are more cautious. Prices peaked mid 2022, in line with historic rallies. Recessions been the usual undoing. Whilst its diversification benefits are now less clear.

- A weaker dollar, stronger China, ‘green’ demand, and underinvestment give support. This should keep prices ‘high-for-longer’. But exposure may be better via forward-looking related equities. A ‘three peat’ leadership year is unlikely.

S&P 500 index ‘corrections’ and subsequent annual performance (%)

Bitcoin puts terrible 2022 behind it

- Bitcoin (BTC) and Ethereum (ETH) prices both rose in a positive start to 2023. Resilient to broader markets volatility, as Fed stays hawkish. And to further FTX-related asset class fallout.

- Solana (SOL) led gainers on the back of the 3,600% price surge of the BONK meme-coin recently launched in its ecosystem. This has helped Solana recoup some of its dramatic losses that came after FTX’s bankruptcy last year.

- FTX fallout has continued, with bank Silvergate (SI) plunging after it saw sharp deposit outflows and cut 40% of its workforce. Exchange Coinbase (COIN) reached a $100 million settlement with US regulators over its compliance shortfalls.

Energy drives a weak start for commodities

- It was a weak start to the year for commodities, after the last two years strong performance. This came as the US dollar rebounded from recent lows and oil and natural gas prices plunged.

- Natgas prices stood out, and now 60% off their March 2022 highs, as unseasonal warm weather in both the US and Europe sapped demand. This shortfall was worsened by the continued delay to reopening the Freeport LNG terminal.

- Industrial metals, like copper, were resilient on hopes China’s accelerated end to its zero covid policy would boost the economy. Gold was helped by less competition from US bond yields.

US Equity Sectors, Themes, Crypto assets

| 1 Week | 1 Month | YTD | |

| IT | 0.63% | -3.54% | 0.63% |

| Healthcare | -0.11% | -0.69% | -0.11% |

| C Cyclicals | 3.11% | -3.55% | 3.11% |

| Small Caps | 1.79% | -1.09% | 1.79% |

| Value | 2.18% | 1.31% | 2.18% |

| Bitcoin | 2.63% | -0.01% | 2.63% |

| Ethereum | 6.27% | 1.62% | 6.27% |

Source: Refinitiv, MSCI, FTSE Russell

The week ahead: earnings and inflation duo

- Global Q4 earnings season kicks off (Fri) with JPM and US banks. Growth fears are running high, with S&P 500 consensus forecasts for a 4% earnings fall, the first fall since Q3 2020.

- December US inflation report (Thu) in focus, with forecast for a 6th straight headline fall to 6.5% vs June’s 9.1% peak. Watch sticky services and housing prices in the est. 5.7% ‘core’ rate.

- Third anniversary of first covid death (Wed) comes as China gone for growth, accelerating end of its zero-covid policy. Seen cases soar but underpinned investor recovery hopes.

- Also Fed Chair Powell’s speech at Riksbank Symposium (Tue). Plus big 25th ICR Consumer and JP Morgan Healthcare sector conferences.

Our key views: A gradual U-shaped recovery

- Lower inflation is the key to our outlook for relief from the double-barrel interest rate and recession pressures. Alongside China going for growth, cutting global recession risks. And a less-bad year for the world’s largest sector, tech. The biggest investor concerns are stickier inflation or a higher-for-longer Fed mistake.

- We see a gradual and U-shaped recovery. With a continued 1H focus on cheap and defensive assets, from healthcare to dividends and UK. See room for more aggressive 2H, from tech to small caps, as lower inflation de-risks markets.

Fixed Income, Commodities, Currencies

| 1 Week | 1 Month | YTD | |

| Commod* | -4.16% | -3.24% | -4.16% |

| Brent Oil | -8.59% | 2.32% | -8.59% |

| Gold Spot | 2.21% | 3.38% | 2.21% |

| DXY USD | 0.38% | -0.86% | 0.38% |

| EUR/USD | -0.55% | 1.04% | -0.55% |

| US 10Yr Yld | -31.69% | -2.12% | -31.69% |

| VIX Vol. | -2.49% | -7.45% | -2.49% |

Source: Refinitiv. * Broad based Bloomberg commodity index

Focus of Week: sector and styles roadmap for a 2023 of two halves

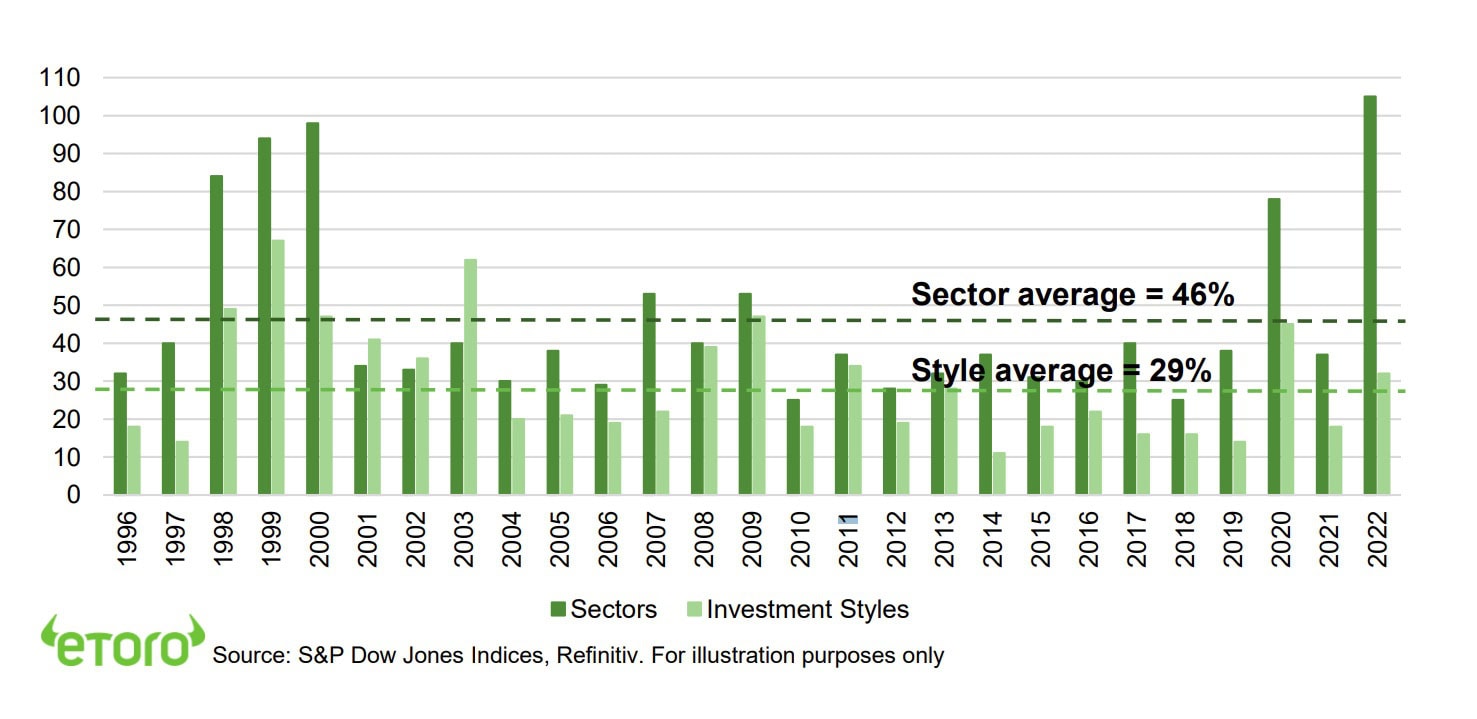

Market stress gives above average opportunities among both equity sectors and investment styles

2022 again showed the benefit of an active approach to managing equity sectors (from communications to utilities) and investment styles (from high dividend to small caps). Market stress drove a wide gap between best and worst performers (see chart). We see 2023 as a year of two halves. With the first half resembling 2022, with volatility high as investors second guess the inflation decline, Fed interest rate peak, and recession risks. Dividends and defensives should keep being rewarded. But the second half may see room for more risk, if the fast inflation fall is validated and Fed rate cuts come onto the horizon as we expect. This opens opportunity in hard pressed tech, real estate, and small caps. See our 2023 investment views.

Average gap between best and worst US sector performance is 46% and investment style 29%

We compared the performance gap between best and worst performing S&P 500 sectors, and the best and worst investment styles. The results are dramatic. The average gap between sector performance is 46% and the gap for investment styles is 29%. The gaps are greater in times of stress, like the 2020 covid-crash and 2007-9 global financial crisis. Last year’s was no different. With the largest ever sector gap, as energy led communications by 105pp. The styles gap was an above average 32pp, of High dividends over Growth.

Dividends and Value to keep leading in 1H 2023, with room for Growth and Small Cap rebound in 2H

High dividend (HDV) and low volatility (SPLV) investment styles were rewarded in 2022 as investors sought defensive and resilient cash flows amidst the sell-off. This also helped Value (IWD) strongly outperform. By contrast tech-heavy Growth (IWF) was the worst style performer as soaring bond yields and recessions risks cut both high valuations and growth forecasts. Small caps (IWM) were hit by recession and debt concerns. Quality QUAL) did not live up to the name given its high tech weighting. We see echoes of 2022 defensive styles outperformance in first half 2023. Lower reported inflation should gradually validate a higher risk approach in the second half focused on lagging, and now cheaper, Growth and Small Caps.

Traditional defensive sectors remain a 2023 focus until lower inflation allows more risk taking

Energy stocks dramatically led a small 2022 oil price rise, with their cheap valuations and big cash returns. Traditional defensives, utilities, staples, and healthcare were also very resilient. Whilst financials low valuations and rising interest rates benefit were more than offset by recession fears. IT (XLK), communications (XLC) and discretionary were hit by a double whammy of both lower valuations and rising recession risks. Defensives remain our first half 2023 focus, with more subdued oil prices likely to hold back energy (XLE). Lesser second half recession and interest rate risks open up room for higher risk sectors like financials, interest rates sensitive real estate, and broader technology.

Performance gap between best- and worst-performing US sectors and investment styles (S&P 500, %)

Key Views

| The eToro Market Strategy View | |

| Global Overview | Aggressive Fed interest rate hiking cycle and stubborn inflation boosted uncertainty, recession risk, and hit markets. We see this gradually fading in 2023, with global growth stressed but resilient, inflation pressure slowly easing, and valuations now more attractive. Focus on cheap and defensive assets for a gradual ‘U-shaped’ market recovery. |

| Traffic lights* | Equity Market Outlook |

| United States | World’s largest equity market (60% of total) seeing slowing but resilient GDP and earnings growth. Valuations led the market rout, and now below average levels, and are supported high company profitability and near peaked bond yields. Fast Fed hiking cycle boosted recession risks. Focus on cash-flows defensives, like healthcare and high dividend. Big-tech supported by defensive growth. See gradual ‘U-shaped’ rebound as inflation slowly falls and de-risks market. |

| Europe & UK | Favour defensive and cheap UK equities (‘Economies are not stock-markets’) over high risk/high return continental Europe. Recession risks high with Russia and energy crisis, threatening to overwhelm ‘buffers’ of rising fiscal spending (defence and refugees), low interest rates (slow to raise ECB), and weak Euro (50%+ sales from overseas). Equities partly cushioned by lack of tech, and 25% cheaper valuations vs US. Favour cheap and defensive UK over Continent. |

| Emerging Markets (EM) | China, Korea, Taiwan dominate EM (60% wt.), and more tech-centric than US. Positive on China as economy reopens, cuts interest rates, and eases tech regulation crackdown. Valuations 40% cheaper than US and market out of favour. Recovery helps global sectors from luxury to materials. Broader EM needs weaker USD and peak US rates catalyst. |

| Other International (JP, AUS, CN) | Canada and Australia benefit from strong equity market weight in commodities and financials, if global growth resilient and bond yields risen. Japanese equities among cheapest of any major market, benefit from weaker JPY and with low inflation, offsetting structural headwinds of low GDP growth, an ageing population, and world’s highest debt. |

| Traffic lights* | Equity Sector & Themes Outlook |

| Tech | ‘Tech’ sectors of IT, communications, consumer discretionary (Amazon, Tesla), dominate US and China. Hurt by higher bond yields and above average valuations. But structural stories with good growth, high margins, fortress balance sheets support some. ‘Big-tech’ attractive new recession defensives. ‘Disruptive’ tech is much more vulnerable. |

| Defensives | Core positions as macro risks rise and bond yields are better priced. Consumer staples, utilities, real estate attractive defensive cash flows, less exposed to rising economic growth risks, and robust dividends. Offset impact of higher bond yields. Healthcare most attractive, with cheaper valuations, more growth, some rising cost protection. |

| Cyclicals | Higher risk cyclical sectors, like discretionary (autos, apparel, restaurants), industrials, energy, and materials, are cheap and attractive if see a ‘slowdown not recession’ scenario. Are select but high risk opportunities from energy to financials stocks. With often depressed earnings, cheaper valuations, and have been out-of-favour for many years. |

| Financials | Benefits from high bond yields, charging more for loans than pay for deposits. Also one of cheapest P/E valuations, and with room for large dividend and buyback yields. But can be outweighed by high recession risks, with lower loan demand and higher defaults. Banks most exposed. Insurance and Diversifieds (like Berkshire Hathaway) the least. |

| Themes | We favour Value over Growth on GDP resilience, lower valuations, rising bond yields, under-ownership after decade under-performance. Dividends and buybacks recovering with cash flows. Power of dividends under-estimated, at up to 1/2 of total long term return. Secular growth of Renewables and Disruptive Tech investment themes. |

| Traffic lights* | Other Assets |

| Currencies | USD ‘wrecking ball’ driven by rising Fed interest rates and ‘safer-haven’ bid. Many DM currencies hurt by still low interest rates and struggling growth. ‘Reverse FX war’ interventions ineffective. Strong USD hurt EM, commodities, US foreign earners like tech. But helps big EU and Japan exporters. Stabler USD outlook as near top of Fed cycle. |

| Fixed Income | US 10-year bond yields risen above prior 3.5% peak, as Fed hikes continue aggressively and balance sheet runoff accelerates. Set to ease as recession risks rise and inflation expectations fall. Additionally US has a wide spread to other market bond yields, and structural headwinds of all-time high debt, poor demographics, low productivity. |

| Commodities | Strong USD and rising recession fears hit commodities. But still above average prices helped by GDP growth, ‘green’ industry demand, supply under-investment, recovering China, Russia supply crisis. Oil helped by slow return of OPEC+ supply and Russia 10% world oil supply problems. But commodities not to repeat their 2022 performance leadership. |

| Crypto | In the latest ‘crypto winter’ (16th crash for bitcoin) with dramatic and early asset class sell-off and later specific risk events from Luna to FTX. See long term asset class development with small size under $1 trillion, correlations low, regulation growing, development/catalysts continuing – Ethereum merge to proof-of-stake and coming BTC halving. |

| *Methodology: | Our guide to where we see better risk-adjusted outlook. Not investment advice. |

| Positive | Overall positive view, and expected to outperform the asset class on a 12-month view. |

| Neutral | Overall neutral view, with elements of strength and weakness on a 12-month view |

| Cautious | Overall cautious view, and expected to underperform the asset class on a 12-month view |

Source: eToro

Analyst Team

| Global Analyst Team | |

| CIO | Gil Shapira |

| Global Markets Strategist | Ben Laidler |

| United States | Callie Cox |

| United Kingdom | Adam Vettese Mark Crouch Simon Peters |

| France | Antoine Fraysse Soulier David Derhy |

| Holland | Jean-Paul van Oudheusden |

| Italy | Gabriel Dabach |

| Iberia/LatAm | Javier Molina |

| Poland | Pawel Majtkowski |

| Romania | Bogdan Maioreanu |

| Asia | Nemo Qin Marco Ma |

| Australia | Josh Gilbert |

Research Resources

Research Library

eToro Plus: In-Depth Analysis. Dive deeper into market insights: Read daily, weekly and quarterly summaries, catch up on the latest market trends and get the most recent, in-depth overview of markets.

Presentation

Find our twice monthly global markets presentation on the multi-asset investment outlook.

Webinars

Join our live Weekly Outlook webinars every Monday at 1pm GMT, or watch the replay at your convenience. Also see the other online courses and webinars.

Videos

Subscribe to our timely video updates on market moving events, and the ‘week ahead’ view

Follow us on twitter at @laidler_ben

COMPLIANCE DISCLAIMER

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.