Summary

Global view on what investors are thinking

Our global survey gets into the investing minds of 10,000 DIY investors in 13 countries. Shows ever-important retail investors resilient. Younger investors are seeing the bright side of the bear market. Saw confidence beginning to rebound as inflation falls. An investor dash-for-cash balanced by a more bullish view on the future. Taking the long view on tech and crypto assets, planning to increase after the 2022 price plunge.

Markets suffer a recession reality check

US equities led a small global ‘reality check’ after year’ strong start. Weak US retail sales rekindled recession fears and saw 10-year bond yields fall to 3.4%. The US dollar is now 10% off highs, and Brent oil up 10% from recent lows. US hit its debt ceiling. MS and GS big results divergence; MSFT and GOOGL cut jobs; NFLX new subs surged; recession fear hit solar high flyers ENPH and SEDG. 2023 Year Ahead View HERE. See video updates, twitter @laidler_ben. We are back in January 2023. Happy holidays!

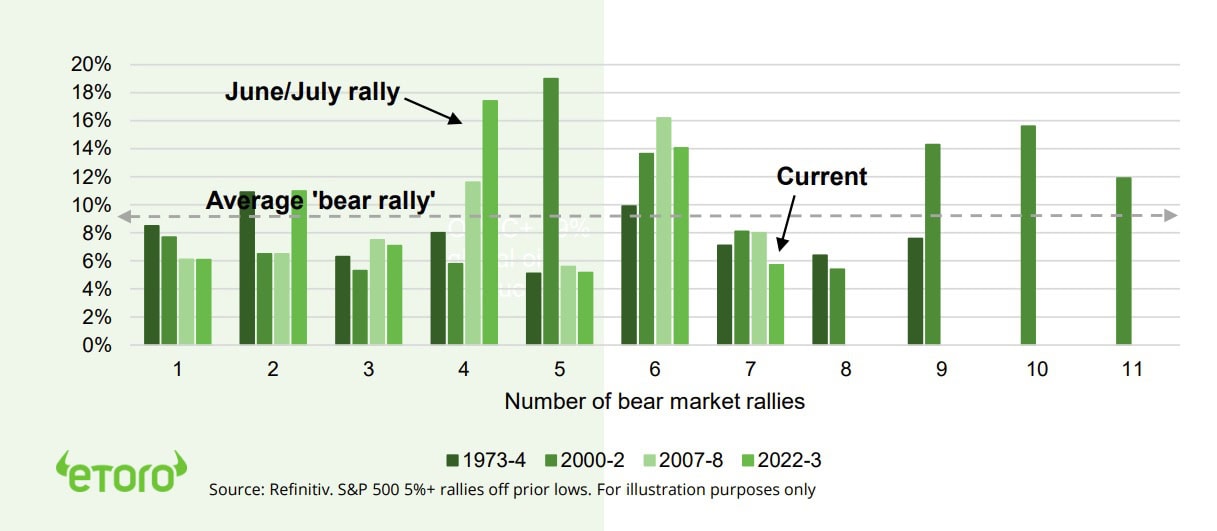

Counting the bear rallies

This 7th ‘bear market rally’ of past year compares more favourably to the multiple false dawns of the 1973, 2000, and 2007 sell-offs. Now light at end of tunnel, but don’t overdo pace.

Europe comes in from the cold

Europe’ equities are on a roll, besting US past 3 months. Is confounding sceptics and denting its long under performance. Valuations cheap and macro less-bad. @EuropeEconomy.

Natural gas impact goes global

Plunging US (NATGAS) and EU natural gas prices have been an important driver of equity markets. We see more stable prices ahead.

Bitcoin macro leading micro

Crypto assets world’s best performers this year, Depressed Bitcoin (BTC) up 25% as competition from 5% Fed funds rate eases.

Crypto holds on to strong gains this year

Crypto held on to its leading asset price gains, with Bitcoin (BTC) up 25% this year. Strength was widespread, with Solana (SOL) continuing its big post-FTX rebound, and top meme-coin Shiba Inu (SHIBxM) particularly strong. More negatively, crypto lender Genesis US filed for bankruptcy, and US arrested Bitzlato founder.

Commodities resilient to recession worries

China reopening, weaker dollar, and rebounding oil – now 10% off recent lows – offset rekindled recession fears and plunging natural gas prices. Natgas continued to suffer from the unseasonal weather, conservation, and rising US production. Lower US bond yields and dollar supported gold, now +20% from its September lows

The week ahead: earnings and PMI’s check-up

1) Big tech-led earnings week with MSFT, TSLA, V, INTC, JNJ, CVX. 2) Global PMI’s (Tue) check-up with recession worries on rise. 3) US Q4 GDP (Thu) to see firm but slower c.2.5% growth. 4) Chinese markets closed for week-long NY holiday, a key test for its zero-covid reopening.

Our key views: A gradual U-shaped recovery

Lower inflation key to relief from double-barrel interest rate and recession pressures. We see a gradual and U-shaped recovery. 1H focus cheap and defensive assets, from healthcare to UK. Room for more aggressive 2H, as lower inflation de-risks markets. Stickier inflation or higher-for longer Fed mistake the big concerns.

Top Index Performance

| 1 Week | 1 Month | YTD | |

| DJ30 | -2.70% | 0.52% | 0.69% |

| SPX500 | -0.66% | 3.22% | 3.47% |

| NASDAQ | 0.55% | 6.12% | 6.44% |

| UK100 | -0.94% | 3.98% | 4.28% |

| GER30 | -0.35% | 7.84% | 7.97% |

| JPN225 | 1.66% | 1.21% | 1.76% |

| HKG50 | 1.41% | 12.51% | 11.44% |

*Data accurate as of 23/01/2023

Market Views

Markets suffer a recession ‘reality check’

- US equities led a small global reality check after a strong start to the year. Disappointing US retail sales rekindled recession fears and saw 10-year bond yields fall to 3.4%. US dollar is now 10% off highs, and Brent oil up 10% from recent lows. US hits its debt ceiling. MS and GS see a big results gap; MSFT and GOOGL cut jobs; NFLX new subs surged; recession fear hit solar high flyers ENPH and SEDG. See our 2023 Year Ahead View HERE.

Counting the bear rallies

- This was the 7th ‘bear market rally’ of past year, and is starting to compare more favourably to the 1973, 2000, and 2007 sell-off examples (see chart). Bear markets typically see many false dawns, but we have come a long way already.

- Joins our list of supportive historic market parallels, such as the rarity of back-to-back annual pullbacks. And alongside the three positive fundamental drivers: of less inflation and interest rate shock, a reopening China, and less bad tech. Just watch the market recovery pace. It’s still going to be a long haul and gradual U shaped recovery, with risks high.

Europe comes in from the cold

- Europe’ equities are on a roll, besting US by 17pp past three months. This is confounding sceptics and denting its multi-year under performance. Poor sentiment and low valuations (12x P/E, 30% discount to US) been an open door for ‘less-bad’ fundamentals. Natgas plunged, China reopening, and continents growth avoided recession so far.

- Fourth quarter earnings (est. +14% YoY) should provide further resilience. Europe is not out-of-the woods. Inflation has barely peaked and the stronger Euro is a mixed blessing. But we think it is an attractive contrarian hunting ground for the brave. See @EuropeEconomy.

Natural gas impact goes global

- Natgas prices plunged on both sides the Atlantic. Europe’ fall got the headlines, but heavyweight US natgas (NATGAS) plunge seen 18-month price lows. Helped relieve inflation pressures and recession fears. And been important driver of equity markets.

- Lower prices driven by unseasonally warm weather and easing demand. Outlook for a modest US price recovery. Would be a goldilocks scenario both for commodity and for macro investors. US EIA is now forecasting average $4.90/MMBtu price this year, well below 2022 but above current.

Bitcoin macro leading micro

- Crypto assets are the world’s best performers this year, with Bitcoin (BTC) up 25%. Strength is being driven by crypto’ traditionally high beta and the less-bad macro environment, with competition from 5% Fed funds rate to ease. And being helped by the crypto class becoming a very small and out of-favour asset class after last year’s plunge.

- Micro pressures remain high after FTX’s collapse and crypto has never faced a long recession. But this obscures plenty of longer term silver linings. From ecosystem development, to rising retail interest, the coming Bitcoin ‘halving, and regulation and institutional catalysts.

History of S&P 500 ‘bear market rallies’

Bitcoin holds onto strong initial gains

- Crypto assets held on to their very strong start to the year, after the dramatic 2022 losses. Bitcoin (BTC) is up 25% since January 1st, and is by far the best performing asset class this year.

- Strength was widespread, with Solana (SOL) continuing its rebound from its huge FTX-driven weakness at the end of 2022. Whilst top meme coin Shiba Inu (SHIBxM) also gained from the easing macro economic concerns.

- Negative news came from leading crypto lender Genesis US declaring bankruptcy. Whilst authorities cracked down, with US arresting the founder of crypto-exchange Bitzlato.

Commodities resilient to recession worries

- Commodity prices had a resilient week. Continued optimism over the reopening of China, a weaker US dollar, and a firmer performance from oil markets all combined to steady prices. This offset a broad rise in recession fears after the weak US retail sales and IP data.

- Natural gas prices stole the show, plunging on continued unseasonal warm weather and higher US production. US prices are over 60% lower than recent highs, and down more in Europe.

- US 10-year bond yields plunged below 3.4%, down a long way from a recent high at 4.2%. This provided less competition to zero-yielding gold, and helped further support its recent rally.

US Equity Sectors, Themes, Crypto assets

| 1 Week | 1 Month | YTD | |

| IT | 1.26% | 6.30% | 6.81% |

| Healthcare | -1.06% | 0.18% | -0.87% |

| C Cyclicals | -0.41% | 8.01% | 8.28% |

| Small Caps | -1.04% | 6.83% | 6.02% |

| Value | -1.88% | 2.39% | 1.18% |

| Bitcoin | 12.94% | 29.66% | 32.45% |

| Ethereum | 14.17% | 33.43% | 35.84% |

Source: Refinitiv, MSCI, FTSE Russell

The week ahead: earnings and PMI’s check

- Q4 earnings season accelerates with big-tech MSFT, TSLA, V, INTC, ASML plus other heavy weights like JNJ and CVX. Lacklustre but in-line so far with S&P 500 revenue +4% and EPS -3%.

- With recession fears rising, US, EU, JP, UK, AU December PMI (Tue) provide a timely health check. Hope for stability near current weak <50 level, with lower ‘price paid’ inflation pressure.

- US Q4 GDP growth forecast firm at +2.5% annualised, but down versus prior 3.2%. Focus on strength of consumer as savings used up, and impact of recent Q4 US dollar weakness.

- Chinese markets closed all week for New Year holidays, and start of ‘Year of the Rabbit’. Is a test this year given traditional home travel and as end zero-covid policy and reopen economy.

Our key views: A gradual U-shaped recovery

- Fed risks a policy mistake, with a high-for-longer interest rate outlook even as forward inflation and GDP growth outlook falls. Market bottomed but recovery to be U-shaped. Gradually lower inflation will be a bumpy ride but will eventually start to de risk markets and allow risk assets, from equities to crypto sustainably recover.

- Focus on core cheap and defensive assets to be invested in this ‘new’ world, of higher inflation and lower growth, and to manage still high risks. Sectors, like healthcare, defensive styles like div. yield, and related UK to Japan markets.

Fixed Income, Commodities, Currencies

| 1 Week | 1 Month | YTD | |

| Commod* | 0.49% | -0.38% | -0.60% |

| Brent Oil | 2.61% | 3.68% | 1.94% |

| Gold Spot | 0.24% | 6.74% | 5.33% |

| DXY USD | -0.21% | -2.24% | -1.48% |

| EUR/USD | 0.22% | 2.26% | 1.44% |

| US 10Yr Yld | -2.57% | -26.94% | -39.99% |

| VIX Vol. | 8.17% | -4.89% | -8.40% |

Source: Refinitiv. * Broad based Bloomberg commodity index

Focus of Week: retail investors a step ahead

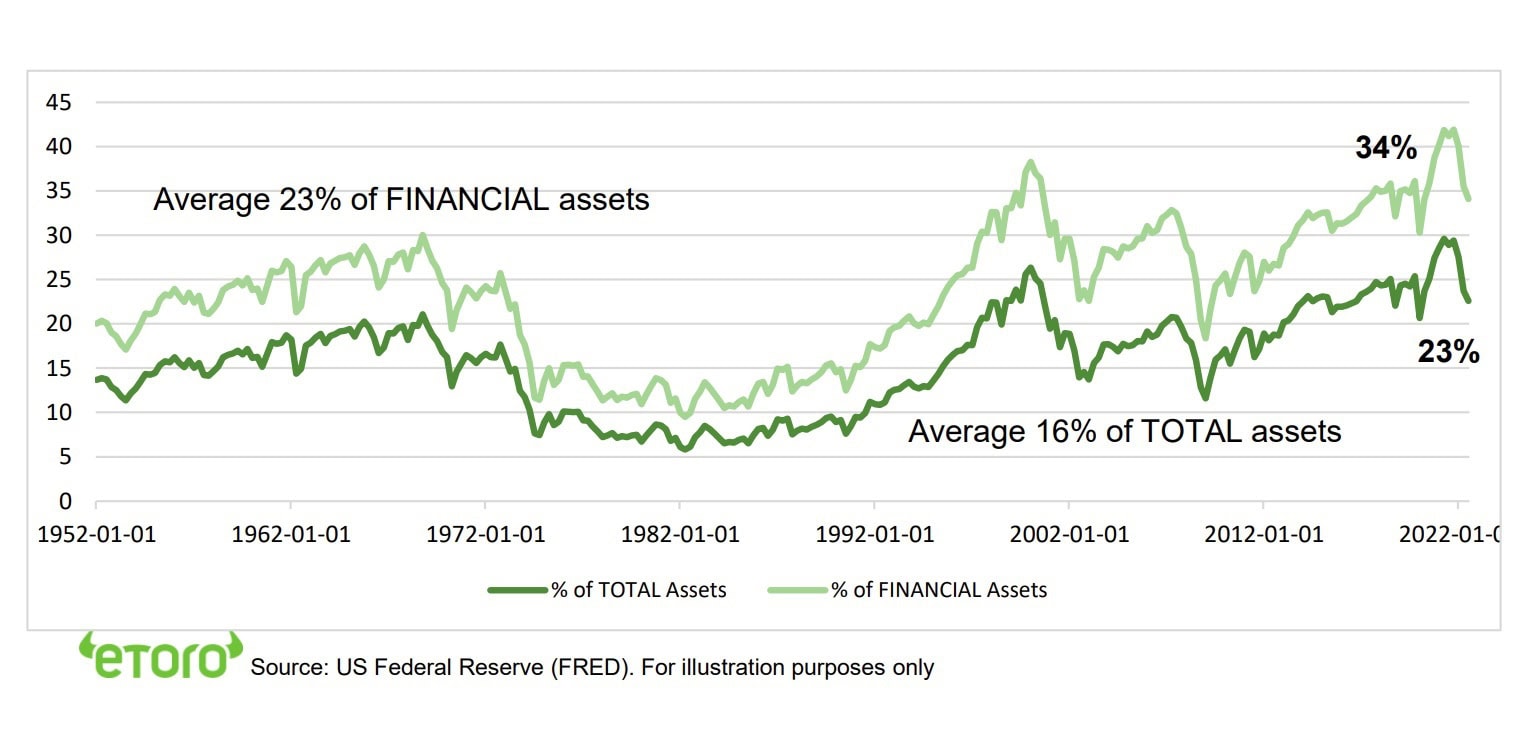

Our latest global survey shows ever-important retail investors resilient

Our Q4 global survey of DIY investors shows continued resilience amidst the first bear market that many have experienced. Alongside signs of an early return of confidence and look again at-risk assets, from tech to crypto. Retail investors continue to confound the sceptics. By investing for years rather than days. And by remaining a big (see chart) presence in global markets. We highlight four key takeaways.

Younger investors are seeing the bright side of the bear market

67% of investors have positive or unchanged views on markets despite last years bear market. This positive view is led by younger investors. They are naturally more risk tolerant and have longer to retirement. But also facing their first prolonged equity bear market. 23% says they have increased their investing appetite. This compares to only 6% of the over-55’s. A majority recognise markets are cyclical and take a long view.

DIY investor confidence begins to rebound as inflation falls

69% of investors felt confident in their portfolios. This was a 5-point increase from Q3. Inflation is seen as the biggest risk but has been easing. US prices have decelerated for six straight months, and for back-to back months in the UK and Europe. But as inflation risks have fallen, global recession remains a close 2nd.

Dash-for-cash but investors also turning selectively bullish on future

We saw a big rise in those investing in cash (from 46% to 69% QoQ). With interest rates more attractive and some stockpiling of ‘dry powder’ to take advantage of market opportunities. Defensive allocations, from healthcare to utilities, and broader asset ownership, across currencies and commodities, also rose.

Taking the long view on tech, planning to increase holdings after the 2022 plunge

Investors have been selectively buying the dip amongst higher risk assets, like tech and crypto. This has positioned them well for recent better performance. Tech stocks are owned by 60% of investors and set to again become the most owned sector. Female and older investors particularly raised their allocations.

Getting into the investing minds of 10,000 retail investors across 13 countries

There are scores of surveys tracking institutional investors thoughts and outlook. But there are shockingly few for the increasingly important DIY investors, especially globally. Our quarterly Retail Investor Beat tries to fill this gap. It polls 10,000 in 13 countries from Australia to the US and across Europe.

US households assets in equities. As % of financial and of total assets

Key Views

| The eToro Market Strategy View | |

| Global Overview | Aggressive Fed interest rate hiking cycle and stubborn inflation boosted uncertainty, recession risk, and hit markets. We see this gradually fading in 2023, with global growth stressed but resilient, inflation pressure slowly easing, and valuations now more attractive. Focus on cheap and defensive assets for a gradual ‘U-shaped’ market recovery. |

| Traffic lights* | Equity Market Outlook |

| United States | World’s largest equity market (60% of total) seeing slowing but resilient GDP and earnings growth. Valuations led the market rout, and now below average levels, and are supported high company profitability and near peaked bond yields. Fast Fed hiking cycle boosted recession risks. Focus on cash-flows defensives, like healthcare and high dividend. Big-tech supported by defensive growth. See gradual ‘U-shaped’ rebound as inflation slowly falls and de-risks market. |

| Europe & UK | Favour defensive and cheap UK equities (‘Economies are not stock-markets’) over high risk/high return continental Europe. Recession risks high with Russia and energy crisis, threatening to overwhelm ‘buffers’ of rising fiscal spending (defence and refugees), low interest rates (slow to raise ECB), and weak Euro (50%+ sales from overseas). Equities partly cushioned by lack of tech, and 25% cheaper valuations vs US. Favour cheap and defensive UK over Continent. |

| Emerging Markets (EM) | China, Korea, Taiwan dominate EM (60% wt.), and more tech-centric than US. Positive on China as economy reopens, cuts interest rates, and eases tech regulation crackdown. Valuations 40% cheaper than US and market out of favour. Recovery helps global sectors from luxury to materials. Broader EM needs weaker USD and peak US rates catalyst. |

| Other International (JP, AUS, CN) | Canada and Australia benefit from strong equity market weight in commodities and financials, if global growth resilient and bond yields risen. Japanese equities among cheapest of any major market, benefit from weaker JPY and with low inflation, offsetting structural headwinds of low GDP growth, an ageing population, and world’s highest debt. |

| Traffic lights* | Equity Sector & Themes Outlook |

| Tech | ‘Tech’ sectors of IT, communications, consumer discretionary (Amazon, Tesla), dominate US and China. Hurt by higher bond yields and above average valuations. But structural stories with good growth, high margins, fortress balance sheets support some. ‘Big-tech’ attractive new recession defensives. ‘Disruptive’ tech is much more vulnerable. |

| Defensives | Core positions as macro risks rise and bond yields are better priced. Consumer staples, utilities, real estate attractive defensive cash flows, less exposed to rising economic growth risks, and robust dividends. Offset impact of higher bond yields. Healthcare most attractive, with cheaper valuations, more growth, some rising cost protection. |

| Cyclicals | Higher risk cyclical sectors, like discretionary (autos, apparel, restaurants), industrials, energy, and materials, are cheap and attractive if see a ‘slowdown not recession’ scenario. Are select but high risk opportunities from energy to financials stocks. With often depressed earnings, cheaper valuations, and have been out-of-favour for many years. |

| Financials | Benefits from high bond yields, charging more for loans than pay for deposits. Also one of cheapest P/E valuations, and with room for large dividend and buyback yields. But can be outweighed by high recession risks, with lower loan demand and higher defaults. Banks most exposed. Insurance and Diversifieds (like Berkshire Hathaway) the least. |

| Themes | We favour Value over Growth on GDP resilience, lower valuations, rising bond yields, under-ownership after decade under-performance. Dividends and buybacks recovering with cash flows. Power of dividends under-estimated, at up to 1/2 of total long term return. Secular growth of Renewables and Disruptive Tech investment themes. |

| Traffic lights* | Other Assets |

| Currencies | USD ‘wrecking ball’ driven by rising Fed interest rates and ‘safer-haven’ bid. Many DM currencies hurt by still low interest rates and struggling growth. ‘Reverse FX war’ interventions ineffective. Strong USD hurt EM, commodities, US foreign earners like tech. But helps big EU and Japan exporters. Stabler USD outlook as near top of Fed cycle. |

| Fixed Income | US 10-year bond yields risen above prior 3.5% peak, as Fed hikes continue aggressively and balance sheet runoff accelerates. Set to ease as recession risks rise and inflation expectations fall. Additionally US has a wide spread to other market bond yields, and structural headwinds of all-time high debt, poor demographics, low productivity. |

| Commodities | Strong USD and rising recession fears hit commodities. But still above average prices helped by GDP growth, ‘green’ industry demand, supply under-investment, recovering China, Russia supply crisis. Oil helped by slow return of OPEC+ supply and Russia 10% world oil supply problems. But commodities not to repeat their 2022 performance leadership. |

| Crypto | In the latest ‘crypto winter’ (16th crash for bitcoin) with dramatic and early asset class sell-off and later specific risk events from Luna to FTX. See long term asset class development with small size under $1 trillion, correlations low, regulation growing, development/catalysts continuing – Ethereum merge to proof-of-stake and coming BTC halving. |

| *Methodology: | Our guide to where we see better risk-adjusted outlook. Not investment advice. |

| Positive | Overall positive view, and expected to outperform the asset class on a 12-month view. |

| Neutral | Overall neutral view, with elements of strength and weakness on a 12-month view |

| Cautious | Overall cautious view, and expected to underperform the asset class on a 12-month view |

Source: eToro

Analyst Team

| Global Analyst Team | |

| CIO | Gil Shapira |

| Global Markets Strategist | Ben Laidler |

| United States | Callie Cox |

| United Kingdom | Adam Vettese Mark Crouch Simon Peters |

| France | Antoine Fraysse Soulier David Derhy |

| Holland | Jean-Paul van Oudheusden |

| Italy | Gabriel Dabach |

| Iberia/LatAm | Javier Molina |

| Poland | Pawel Majtkowski |

| Romania | Bogdan Maioreanu |

| Asia | Nemo Qin Marco Ma |

| Australia | Josh Gilbert |

Research Resources

Research Library

eToro Plus: In-Depth Analysis. Dive deeper into market insights: Read daily, weekly and quarterly summaries, catch up on the latest market trends and get the most recent, in-depth overview of markets.

Presentation

Find our twice monthly global markets presentation on the multi-asset investment outlook.

Webinars

Join our live Weekly Outlook webinars every Monday at 1pm GMT, or watch the replay at your convenience. Also see the other online courses and webinars.

Videos

Subscribe to our timely video updates on market moving events, and the ‘week ahead’ view

Follow us on twitter at @laidler_ben

COMPLIANCE DISCLAIMER

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.