Executive Summary:

Occidental Petroleum (OXY) delivered a standout performance in 2024, showcasing operational excellence that transcends mere numbers. Record-breaking oil and gas production, coupled with a significant surge in proved reserves, underscores OXY’s strategic prowess and commitment to maximizing shareholder value.

Key Highlights: Operational Excellence in Action

OXY’s 2024 achievements highlight its operational strength:

- Unprecedented U.S. Oil Output: 571,000 barrels per day, demonstrating superior extraction efficiency.

- Record-Breaking Total Production: 1.33 million BOE per day, illustrating OXY’s substantial operational scale.

- Surge in Proved Reserves: 4.6 billion BOE, a 15% year-over-year increase, signalling robust future production potential.

Growth Catalysts: Strategic Acquisitions and Financial Strength

OXY’s growth trajectory is fuelled by strategic acquisitions, notably CrownRock, which expands its valuable Permian Basin footprint. Strong free cash flow enables debt reduction, consistent dividends, and share buybacks, mitigating the impact of crude oil price volatility.

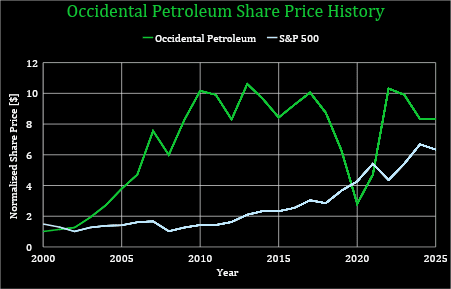

Data: https://www.macrotrends.net/stocks/charts/OXY/occidental-petroleum/stock-price-history

Business Model: A Diversified Energy Leader

- Upstream Excellence: OXY excels in oil and gas acquisition, exploration, and development across the U.S., Middle East, and North Africa.

- Chemical Innovation (OxyChem): A key producer of chlor-alkali products and PVC/VCM, supplying essential industrial inputs.

- Integrated Midstream Operations: OXY manages critical natural gas and CO2 processing and pipeline infrastructure.

- Strategic Partnerships: Supplying refineries, petrochemical plants, and other industry leaders.

Industry Analysis: Navigating Market Dynamics

- Crude Oil Price Sensitivity: OXY’s revenue is closely tied to global oil prices. Recent trends suggest potential upward momentum.

- Macroeconomic Considerations: Economic pressures and interest rate fluctuations pose challenges, but Warren Buffett’s stake signals strong market confidence. Geopolitical risks remain a factor.

- Competitive Positioning: OXY’s leadership in the Permian Basin, particularly in Enhanced Oil Recovery (EOR), and its diversified portfolio in the DJ Basin and Gulf of Mexico, provide a competitive edge.

| Competitors | Market Cap [$Billion] | PE |

|---|---|---|

| BP PLC (BP) | 90.87 | 411.92 |

| Chevron Corporation (CVX) | 292.42 | 17.13 |

| ConocoPhillips (COP) | 130.25 | 13.12 |

| EOG Resources (EOG) | 70.12 | 11.26 |

| ExxonMobil Corporation (XOM) | 510.85 | 15.01 |

| Shell (SHEL) | 168.42 | 13.81 |

| TotalEnergies (TTE) | 134.09 | 9.1 |

| Occidental Petroleum (OXY) | 45.89 | 21.63 |

| Average | 180.36 | 64.12 |

Note: A one-time environmental liability impacted Q4 2024 earnings, affecting the P/E ratio.

Investment Thesis: Building Shareholder Value

- Financial Resilience: OXY’s Q4 earnings demonstrated operational resilience, with efficiency gains and debt reduction offsetting revenue declines. Robust free cash flow supports strategic investments and shareholder returns.

- Strengthened Financial Position: Rising cash reserves and asset growth bolster OXY’s financial stability, with equity growth projected for 2025.

- Growing Dividend Appeal: The dividend, currently yielding 1.97%, is poised for further growth, enhancing investor returns.

- Strategic CrownRock Acquisition: Enhances Permian Basin presence, with non-core asset divestitures to mitigate risk.

- Operational Efficiency: Replacing higher-cost reserves with lower-cost, higher-volume reserves demonstrates portfolio strength.

- OxyChem’s Growth Initiatives: Plant enhancements and modernization projects are set to boost cash flow.

- Leadership and Recognition: CEO Vicki Hollub’s leadership and OxyChem’s safety and environmental awards underscore strong management.

Valuation:

Current valuations suggest a potential upside of 26%. Below the sensitivity of the stock price with lower growth rates. Market sentiment is positive and strengthens the value.

| Growth | LT-growth | WACC | Fair value | Vs current | |

|---|---|---|---|---|---|

| High | 15.0% | 3.98% | 9.28% | $ 61.76 | 26% |

| Medium | 13.0% | 3.98% | 9.28% | $ 57.96 | 19% |

| Low | 8.0% | 3.98% | 9.28% | $ 49.26 | 1% |

| Average | $ 56.33 | 15% | |||

| Book value | $ 28.13 | ||||

| Current | $ 48.83 |

Risk Factors: Navigating Industry Challenges

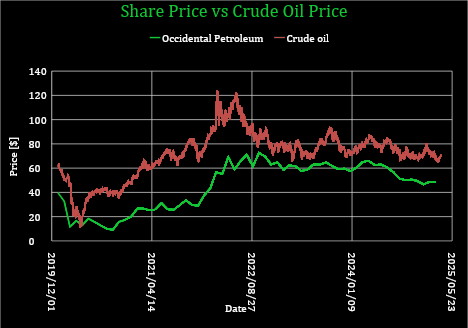

- Market Volatility: Oil and gas price fluctuations pose significant risks. See the strong correlation between the OXY stock and oil prices in the graph below.

- Regulatory Pressures: Increasing environmental regulations and legislative changes can impact costs.

- Competitive Landscape: Intense competition can erode market share.

Data: https://www.macrotrends.net/1369/crude-oil-price-history-chart

Conclusion: A Compelling Investment Opportunity

OXY’s strategic acquisitions, operational efficiency, and financial strength position it for long-term growth. While market and regulatory risks exist, OXY’s proactive management and diversified portfolio make it a compelling investment.

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.