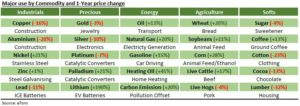

MESSAGES: Commodity markets have been on a roller-coaster ride all this year. The broad Bloomberg commodity index fell 15% from its June high. But it is still by far the best performing asset class this year, up 17%. Recent weakness has been driven by the surging US dollar and rising global recession fears. But this has been cushioned by a supply side tightened by over a decade of low investment and rolling disruptions from war to weather. Cross-checking individual commodity performance against its major use is illustrative. It gives an unsettling view of Chinese growth, the US housing slowdown, and global discretionary consumption. Whilst being a lot more reassuring on basic food demand and the steadily accelerating EV adoption.

WEAKEST: Declines across industrial metals, from ‘Dr. copper’ to aluminum, are emblematic of China’s struggling stop-start economic recovery and gargantuan property sector slowdown, with the country over half of global metals demand. Whilst the big slump in volatile lumber prices is a worrying lead indicator for the creaking US housing market, where 90% of homes are wooden framed. Falling cocoa and cotton prices don’t bode well for discretionary consumption. With fears of increasingly squeezed consumer budgets and high inventories offsetting crop failures.

STRONGEST: Lithium prices have continued to surge, alongside accelerating electrical vehicle (EV) adoption. This has also been a tailwind for nickel. But recovering legacy ICE car volumes are also providing temporary support to others, like palladium. Food commodities, from grains to cattle, have seen plenty of supply disruption but also benefited from the consumer refocus on basic needs and continued demographic support. Others have benefitted as lower priced substitutes. With switches from natgas to oil (also driving carbon emissions) and wheat to corn.

All data, figures & charts are valid as of 04/10/2022