Summary

Loosening financial conditions challenges Fed

The double-digit stock market rally off June lows is increasingly ‘fighting the Fed’. The equity and bond rally has loosened financial conditions, and undone much of Fed’s interest rate tightening. This raises risks ahead of Jackson hole, key jobs and prices data, and the Sept. 21 FOMC. But with inflation likely peaked, we would use any market weakness to add select ‘quality risk’ big tech and small cap, alongside core defensives.

Markets consolidates after strong gains

Markets eased after a four week winning streak. Cross-currents of weaker China growth, Europe inflation and natgas rises, and still-hawkish Fed. But decent Q2 stock results, from WMT to CSCO, and lower US producer prices. US 10-year bond yields rose back to near 3%, the US dollar soared, and Bitcoin slumped. Came ahead of this week’ Jackson hole Fed meeting. See presentation, video updates, and twitter @laidler_ben.

The growing ‘productivity paradox’

Economic growth is being held back by weak productivity, despite the tech surge. Puts a focus on tech productivity-enablers from 5G, to cloud computing, and semiconductors.

Europe in the eye-of-the-storm

Record natgas prices, looming energy rationing, drought, stagflation, recession. Europe is stuck between economic rock-and-a-hard-place. EUR borne brunt as equities resilient with valuations cheaper. See @EuropeEconomy.

Not giving up the latte

Coffee prices holding near highs as consumers do not want to give up their $3 lattes, whilst Brazil Arabica supply falls. Impacts Starbucks (SBUX) to Nestle (NESN.ZU).

Crypto more popular than stocks

Easing of this crypto-winter very different from the last, with a higher equity correlation, and institutional and retail adoption.

Crypto assets fall back after rebound

Bitcoin fell below $22,000, whilst Ethereum (ETH) also gave back some of recent big gains ahead of September’s ‘merge. Meme coins Shiba (SHIBxM) and Doge (DOGE) followed their equity peers up. Stablecoin Tether announced more transparency whilst LatAm e-commerce giant Mercado Libre (MELI) an ETH cashback token.

Commodities held back by China and dollar

Weak economic data from biggest buyer, China, and the stronger US dollar combined to hold back commodity prices. But soaring EU natgas prices also drove up US natgas and EU carbon credits. Cotton prices rose on estimates for 20% lower supply from no. 3 supplier, US.

The week ahead: Fed-talk at Jackson Hole

1) Focus on Fed inflation tough-talk at Jackson Hole symposium. 2) Latest global PMI growth and inflation data, on US, EU, UK, Japan. 3) Big tech earnings from NVDA, CRM, ZM, and SNOW. 4) Europe’ energy and cost-of-living crisis, including UK 50%+ price cap hike.

Our key views: Inflation drives everything

Peaked US inflation drives sight of end to Fed rate hikes and less recession risk. Supports from both resilient consumers and corporates, But recovery likely U not V shaped. Gradually lower inflation will be a bumpy ride but slowly de-risks market, allowing higher-risk assets, big tech to crypto, alongside core defensives.

Top Index Performance

| 1 Week | 1 Month | YTD | |

| DJ30 | -0.16% | 5.67% | -7.24% |

| SPX500 | -1.21% | 6.74% | -11.28% |

| NASDAQ | -2.62% | 7.36% | -18.79% |

| UK100 | 0.66% | 3.77% | 2.25% |

| GER30 | -1.82% | 2.19% | -14.73% |

| JPN225 | 1.34% | 3.64% | 0.48% |

| HKG50 | -2.00% | -4.06% | -15.49% |

*Data accurate as of 22/08/2022

Market Views

Markets consolidate after strong gains

- Sharp global equity rally from June lows eased back last week. Faced cross-currents of weaker Chinese demand, Europe inflation and natgas fears, and still-hawkish Fed commentary. But continued resilient company results, from WMT to CSCO, and lower US producer prices eased price rise fears. Comes ahead of this week’ Fed Jackson hole meeting. Page 6 for Resource reports, presentations, videos, and twitter.

The growing ‘productivity paradox’

- Economic growth is hurt by weak productivity, despite the tech surge. There are only two big ways economies grow: 1) more people and 2) how much people produce (‘productivity’). This cuts GDP, and earnings, growth and boosts the impact of inflation. No surprise Fed cut long-term growth forecast 2.6% to 1.9% over past decade.

- Focus productivity tech like 5G (@5GRevolution), cloud computing (@CloudComputing), and semis (@Chip-Tech) and education to boost.

Europe in the eye-of-the-storm

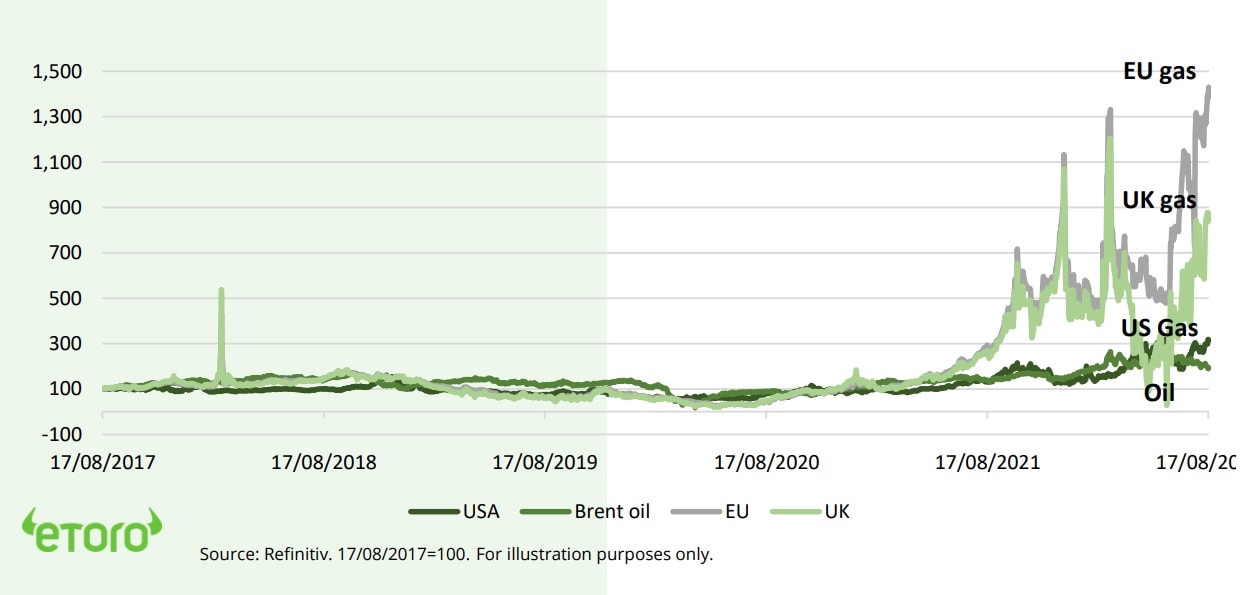

- Record natgas prices, looming energy rationing, drought, stagflation, recession. Europe is stuck between an economic rock-and-a-hard-place.

- The energy crisis (see chart) is intractable, set to drag the continent into a recession later this year, and its impact will last into 2023. The Euro has borne the brunt of this investment storm, down at parity with the US dollar. Whilst equities have been more resilient. See @EuropeEconomy.

- Profits growing off a low base, up 29% in Q2. Whilst valuations were already cheap, with most-impacted Germany at a 45% P/E valuation discount to the US. FTSE100 shows stock markets are not economies. A weaker euro, still low interest rates, and rising fiscal spending are all important supports.

Not giving up the latte

- Arabica price held near decade highs as consumers not want to give up their $3 morning brew despite squeezed finances. Has tightened coffee market, as lower Brazilian yields cut the supply and inventory outlook. Took Arabica’s price-premium to Robusta up sharply, boosting blending and restrain prices.

- High bean prices added to the building consumer downtrading and profit margin pressures on big users from Starbucks (SBUX) to Nestle (NESN.ZU). Similar to the Big Mac index, the Latte index shows Switzerland with the world’s priciest latte’s and Turkey having the cheapest.

Crypto more popular than stocks, for many

- Latest ‘crypto winter’ started to ease, with crypto $1.1 trillion asset-of-choice leading rebound in $110 trillion equities. Crypto also looking to put self inflicted wounds behind with Sept. 15 Ethereum merge. Much changed since 2017-18 crypto winter. Equity correlation higher; more crypto instruments available; more institutional and retail adoption.

- Younger DIY investors now own more crypto than equities (37% to 31%) in contrast to older cohorts, and been ‘buying the dip’ (39% to 12%).

European and UK natural gas prices surge (Last 5 years. Index=100)

Crypto falls back after rebound

- Crypto prices fell back sharply after recent strong gains, with bitcoin (BTC) falling below $22,000 and Ethereum (ETH) seeing some profit-taking ahead of the September 15th ‘merge’ date.

- Meme coins Shiba (SHIBxM) and Dogecoin (DOGE) were the outperformers. Likely helped by the sharp rally in equity meme compatriots last week, led by Bed, Bath & Beyond (BBBY).

- Other developments saw the largest stable coin Tether (USDT) hire accountant BDO Italia for stepped-up monthly proof-of-reserve reports. Whilst LatAm e-commerce giant Mercado Libre (MELI) launches its own ETH cashback token.

Held back by struggling China and rising dollar

- Commodity prices were held back by weaker economic data from no.1 buyer China, that forced the central bank their to cut interest rates. Whilst more hawkish commentary from the US Fed officials pushed up the US dollar.

- European natgas prices soared to new record highs, with impacts rippling to other markets. US prices are near 14-year highs, part supported by stepped up EU demand as it looks to replace Russian supplies. Whilst EU demand switching to dirtier fuels is boosting EU emission credit prices.

- Cotton prices rose as US drought drives est. 20% less supply from the world’s no.3 producer, and more than offsets recession-demand concerns.

US Equity Sectors, Themes, Crypto assets

| 1 Week | 1 Month | YTD | |

| IT | -2.52% | 5.82% | -20.08% |

| Healthcare | -1.18% | 3.15% | -8.23% |

| C Cyclicals | -1.70% | 8.83% | -18.90% |

| Small Caps | -2.94% | 7.08% | -12.83% |

| Value | -0.53% | 5.98% | -6.46% |

| Bitcoin | -11.74% | -10.19% | -54.97% |

| Ethereum | -11.39% | 9.39% | -54.42% |

Source: Refinitiv, MSCI, FTSE Russell

The week ahead: Fed to talk tough

- US Fed Jackson Hole symposium August 25-7, titled ‘Reassessing constraints on the economy and policy’. Likely to repeat Fed’s still-hawkish bias ahead of September 21 FOMC meeting.

- August flash PMI’s for the US, EU, UK, Japan, Australia provide timely check-up on the race between slowing GDP and inflation. Risk is that the global composite PMI slips further from July’s border-line contraction level of 50.8.

- Spotlight on rebounding tech earnings, with reports from GPU chip giant NVDA, customer relationship manager leader CRM, WFH favourite ZM, plus SNOW, VMW, PANW, INTU.

- Europe’ energy and cost-of-living crisis gathers steam with new all-time-high natgas prices. UK set to announce next 50%+ rise in consumer energy price cap that driving inflation to 13%.

Our key views: Inflation drives everything

- Peaked US inflation drives sight of end to Fed rate hikes and eases recession risks. Market supports from both resilient consumers and corporates, But recovery U not V shaped. Gradually lower inflation will be a bumpy ride but it slowly de-risks markets and allows more higher-risk assets, from big tech to crypto.

- Focus on core cheap and defensive assets to be invested in this ‘new’ world, to manage still high risks. Sectors, like healthcare, defensive styles like div. yield, and related UK to China markets.

Fixed Income, Commodities, Currencies

| 1 Week | 1 Month | YTD | |

| Commod* | -0.72% | 4.97% | 23.34% |

| Brent Oil | -1.96% | -2.69% | 23.29% |

| Gold Spot | -3.22% | 2.03% | -3.84% |

| DXY USD | 2.34% | 1.29% | 12.64% |

| EUR/USD | -2.13% | -1.72% | -11.72% |

| US 10Yr Yld | 13.45% | 21.44% | 145.94% |

| VIX Vol. | 5.48% | -10.55% | 19.63% |

Source: Refinitiv. * Broad based Bloomberg commodity index

Focus of Week: ‘Don’t fight the Fed’

Double-digit stock market rally from bottom well-supported but is increasingly ‘fighting the Fed’

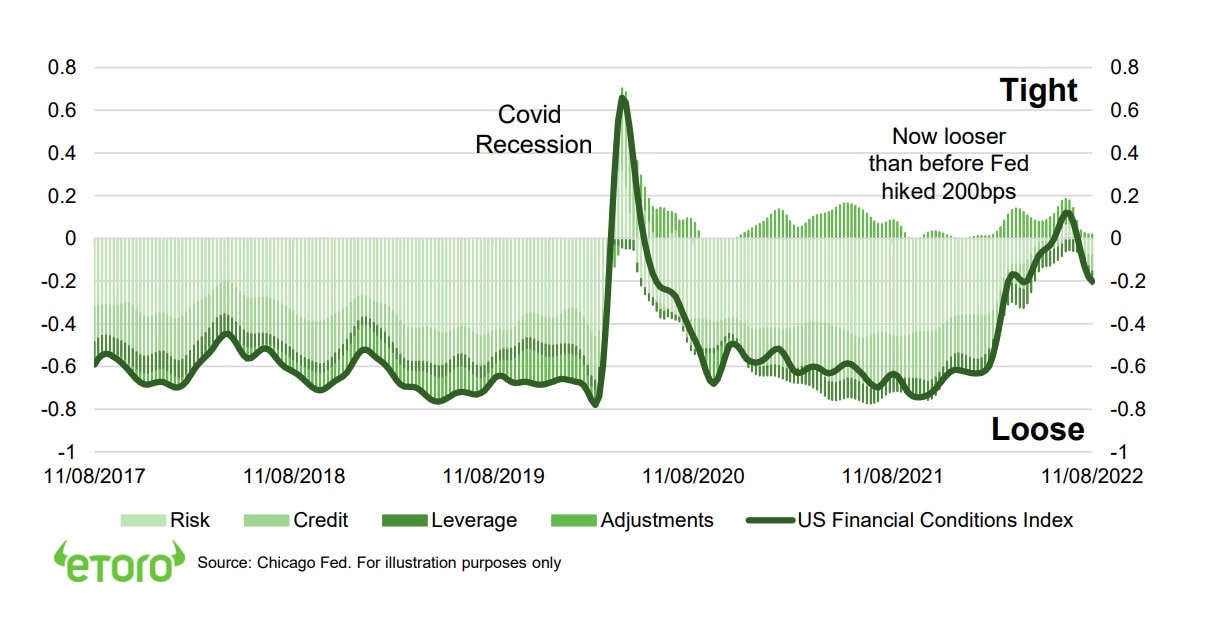

The stock market is ignoring one of its traditional mantra’s to ‘not fight the Fed’. This was coined by investor Marty Zweig in 1970 and in his Winning on Wall Street book. The sharp recent loosening in financial conditions (see chart), is the opposite of what the Fed is trying to do by aggressively hiking interest rates. This loosening has continued despite Fed governor protestations this loosening is ‘too much, too soon’. We have seen the inflation peak, but the job of lowering inflation back to the 2% target is far from done. This sets the market up for some volatility ahead, from the Fed and/or economic data. Defensive-focused investors should use any market weakness to add to select ‘quality risk’, from big tech to small caps.

The market rally is loosening financial conditions, and undoing much of the Fed’s rate tightening

The Chicago Fed national financial conditions index is now back in ‘loose’ territory. It is at levels last seen back in April, before the Federal Reserve raised interest rates by 200bps. It spent scarcely six weeks in the ‘restrictive’ territory needed to slow the economy. The index tracks market measures of risk, credit, and leverage – all have been easing off. 30-year mortgage rates have fallen over 0.5%. Whilst the S&P 500 rallied 15% from its lows. This is unwinding much of the work the Fed done to try and slow the economy.

Ahead of Fed Jackson hole meet, jobs and inflation data tightrope, and Sept 21st FOMC decision

The market is facing two risks after its relief rally from June lows. Firstly, that the Fed seeks to talk down the market and retighten financial conditions. The opportunity to talk is at the central bank Jackson hole symposium this week. The time for action is the September 21 meeting, where it decides whether to hike 50bps or surprise with 75bps. Key economic reports could also sway the now ‘data dependent’ Fed, with the August jobs report (2 September) and August CPI data (13 September) due before next Fed meeting.

With inflation still set to ease, use any volatility to add to ‘quality risk’

The recent rally has propelled the highest risk assets the most, from disruptive tech onwards. They are most vulnerable to a healthy breather in the rebound, or a worse-case pullback. The more the rally goes now, the more the risks rise of aggressive Fed action. Or of the inevitable ‘data-dependent’ bumps in the road, or a looming valuation ceiling with the S&P 500 now back above average valuations. But the longer term recovery remains supported. By peaked inflation, resilient earnings and consumers, and still depressed overall investor sentiment. This means we are fully invested, though defensively focused. We would use any market weakness or volatility to add to ‘quality’ risk, from big tech to small caps to crypto.

US adjusted national financial conditions index (last 5 years)

Key Views

| The eToro Market Strategy View | |

| Global Overview | Geopolitical risks alongside the Fed hiking cycle is boosting uncertainty and weakening markets. We see this as slowly fading, the global growth outlook secure, and valuations more compelling. Focus on cheap cyclical and defensive assets within equities, like Value, plus commodities, crypto. Relative caution on fixed income and the USD. |

| Traffic lights* | Equity Market Outlook |

| United States | World’s largest equity market (60% of total) seeing slowing GDP growth but still-resilient earnings growth. Valuations led market rout, and now at average levels, and are supported by peaked bond yields and high company profitability. Faster Fed hiking cycle is boosting recession risks. Focus on traditional cash-flows defensives, like healthcare and high dividend. Big-tech supported by structural growth outlook. See a gradual ‘U-shaped’ rebound as inflation falls. |

| Europe & UK | Favour defensive and cheap UK equities (‘Economies are not stock-markets’) over high risk/high return continental Europe. Recession risks high with Russia and energy crisis, threatening to overwhelm ‘buffers’ of rising fiscal spending (defence and refugees), low interest rates (slow to raise ECB), and weak Euro (50%+ sales from overseas). Equities partly cushioned by lack of tech, and 25% cheaper valuations vs US. Favour cheap and defensive UK over Continent. |

| Emerging Markets (EM) | China, Korea, Taiwan dominate EM (60% wt), and more tech-centric than US. Positive on China as economy reopens, cuts interest rates, and eases tech regulation crackdown. Valuations 40% cheaper than US and market out of favour. Recovery helps global sectors from luxury to materials. More cautious rest of EM on rising rates and strong USD. |

| Other International (JP, AUS, CN) | Canada and Australia benefit from strong equity market weight in commodities and financials, as global growth rebounds and bond yields set to rise. Japanese equities among cheapest of any major market and vaccination rates accelerating, but has structural headwinds of low GDP growth, an ageing population, and world’s highest debt. |

| Traffic lights* | Equity Sector & Themes Outlook |

| Tech | ‘Tech’ sectors of IT, communications, parts of consumer discretionary (Amazon, Tesla), dominate US and China. Expect more subdued performance as bond yields rise. But are structural stories with good growth, high margins, fortress balance sheets that justify high valuations. ‘Big-tech’ the new defensives. ‘Disruptive’ tech more vulnerable. |

| Defensives | Core positions as macro risks rise and bond yields are better priced. Consumer staples, utilities, real estate attractive defensive cash flows, less exposed to rising economic growth risks, and robust dividends. Offset impact of higher bond yields. Healthcare most attractive, with cheaper valuations, more growth, some rising cost protection. |

| Cyclicals | Cyclical sectors, like consumer discretionary (autos, apparel, restaurants), industrials, energy, and materials, are cheap and attractive in a ‘slowdown not recession’ scenario. Are sensitive to re-opening economies, resilient GDP growth, and higher bond yields, with depressed earnings, cheaper valuations, and have been out-of-favour for many years. |

| Financials | Benefits from higher bond yields, charging more for loans than pay for deposits. Also one of cheapest P/E valuations, and room for large dividend and buyback yields. But is being outweighed by rising recession risks, with lower loan demand and higher defaults. Banks most exposed. Insurance and Diversifieds (like Berkshire Hathaway) least. |

| Themes | We favour Value over Growth on GDP resilience, lower valuations, rising bond yields, under-ownership after decade under-performance. Dividends and buybacks recovering with cash flows. Power of dividends under-estimated, at up to 1/2 of total long term return. Secular growth of Renewables and Disruptive Tech themes. |

| Traffic lights* | Other Assets |

| Currencies | USD well-supported for now by rising Fed interest rate outlook and ‘safer-haven’ bid on virus fourth wave virus. This is likely more modest than prior USD rallies as rest of world growth recovers and virus fears ease. A strong USD traditionally hurts EM, commodities, US foreign earners, such as tech, but helps EU and Japan exporters. |

| Fixed Income | US 10-year bond yields to rise modestly as inflation above 2% average Fed target, ‘real’ inflation-adjusted yields negative, Fed to gradually tighten policy. Will be modest as inflation expectations already high, wide spread to other market bond yields, and structural headwinds of all-time high debt, poor demographics, and low productivity. |

| Commodities | In ‘sweet spot’ of robust GDP growth, ‘green’ industry demand, years of supply under-investment, recovering China, and Russia supply crisis. Industrial metals and battery materials well positioned. Oil helped by slow return of OPEC+ supply and Russia 10% world supply problems. Gold helped by risk-aversion but held back by rising bond yields. |

| Crypto | Institutionalization of bitcoin market barely begun, as asset class benefits from very strong risk-adjusted returns and low correlations with other assets. Clear supply rules a benefit as inflation high. Volatility still high, with the 16th -50% pullback of the last decade. Adoption and development continuing regardless. See Ethereum merge to Proof-of-Work. |

| *Methodology: | Our guide to where we see better risk-adjusted outlook. Not investment advice. |

| Positive | Overall positive view, and expected to outperform the asset class on a 12-month view. |

| Neutral | Overall neutral view, with elements of strength and weakness on a 12-month view |

| Cautious | Overall cautious view, and expected to underperform the asset class on a 12-month view |

Source: eToro

Analyst Team

| Global Analyst Team | |

| CIO | Gil Shapira |

| Global Markets Strategist | Ben Laidler |

| United States | Callie Cox |

| United Kingdom | Adam Vettese Mark Crouch Simon Peters |

| France | Antoine Fraysse Soulier David Derhy |

| Holland | Jean-Paul van Oudheusden |

| Italy | Gabriel Dabach |

| Iberia/LatAm | Javier Molina |

| Poland | Pawel Majtkowski |

| Romania | Bogdan Maioreanu |

| Asia | Nemo Qin Marco Ma |

| Australia | Josh Gilbert |

Research Resources

Research Library

eToro Plus: In-Depth Analysis. Dive deeper into market insights: Read daily, weekly and quarterly summaries, catch up on the latest market trends and get the most recent, in-depth overview of markets.

Presentation

Find our twice monthly global markets presentation on the multi-asset investment outlook.

Webinars

Join our live Weekly Outlook webinars every Monday at 1pm GMT, or watch the replay at your convenience. Also see the other online courses and webinars.

Videos

Subscribe to our timely video updates on market moving events, and the ‘week ahead’ view

Follow us on twitter at @laidler_ben

COMPLIANCE DISCLAIMER

This communication is for information and education purposes only and should not be taken as investment advice, a personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without taking into account any particular recipient’s investment objectives or financial situation and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past or future performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication.