Please see this week’s market views from eToro’s global analyst team. The full 5-pager includes latest market data, the house investment view, and a weekly ‘special’.

Contrarian ideas among this year’s laggards

Markets have been very strong this year, but not everyone has benefitted. We highlight the biggest laggards from small caps to VIX volatility across the world, sectors, themes, and asset classes, looking for contrarian opportunities for the brave. We highlight bottoming and weather-driven ‘widow-maker’ Natgas; ending of China’s triple disappointment; high dividend yield as interest rate hikes end; and crypto Polygon on its rebranding and 2.0 upgrade. See Page 4

S&P 500 inflation and strike crosscurrents

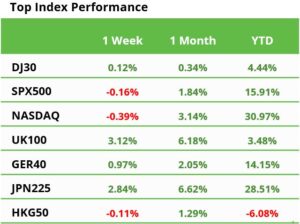

Stocks firm as core US inflation hit new low and retail sales stayed strong, whilst China growth bottomed. Europe boosted by the ECB’s last hike. Versus headwind from UAW car strike and ‘triple witching’ volatility. TSLA surge on Dojo supercomputer value. AAPL surprise iPhone15 price ‘freeze’ as goes for volume. ARM soared in biggest IPO of year. See Q3 Markets Outlook HERE and at twitter @laidler_ben. See Page 2

The hard last inflation yards

US inflation most important number in markets and its gradual easing, as housing and jobs pressures cool, opens way to rate cuts and helps the economic and profits outlook. See Page 2

The three drivers of the earnings recovery

Next bull market stage led by profits recovery of tech leadership, profits margins, GDP resilience taking over from rising valuations. See Page 2

Currencies in interest firing line

LatAm currencies resilient to early rate cuts but Poland’s Zloty plunged, on very different real rates and FX valuations, and taste of what to come as global rate cycle turns. See Page 2

Beer shows the limits to price rises

Big beer producers are seeing the limits of their multi-year price ‘premiumisation’ strategy as consumers push back, whilst investors derate their premium market valuations. See Page 2

Crypto resilient to FTX overhang risk

Crypto markets benefited from broader market relief and shrugged off the overhang risk from bankruptcy court allowing FTX to sell its $3 billion crypto holdings. Credit card giant V announced stablecoin plan with SOL. Ripple bought custodian Fortress. Binance laid off workers. See the latest Weekly Crypto Roundup. See Page 3

Energy drives commodity rally on

Brent oil prices rallied to over $93/bbl. on deeper market deficit forecasts, lifting whole asset class and threatening markets. BP.L CEO resigned, throwing renewables shift into focus. Ag markets saw more weather disruption, and cocoa hit new high. Nickel hit a new low, on China slowdown and EV battery demand fears. See Page 3

The week ahead: Fed, BoE, PMIs, and Fedex

1) Fed (Wed) to keep rates unchanged at top of cycle, whilst BoE (Thu) hikes again. 2) US, EU, UK, JP, AU PMI (Fri) health check. 3) FDX, AZO, GIS, KBH, DRI, MU earnings and CART, KYVO IPOs. 4) Watch Oct.1 US government shutdown deadline, UAW auto strike, Oktoberfest start. See Page 3

Our key views: A positive markets breather

Market seeing breather after strong 1H, with weaker seasonality, low volatility, and coming growth slowdown. But fundamentally positive on lower inflation and coming rate cuts. Focus on defensive growth and long duration assets from healthcare to big tech. Cautious growth exposed cyclicals, commodities, and banks. See Page 5