While UK markets remained closed for the Easter bank holiday on Monday, US markets opened with a lacklustre response to the oil production cut deal struck by Opec and Russia, announced over the weekend. After a month-long price war, and with oil demand collapsing, the group agreed to cut production by close to 10 million barrels a day in May and June — the biggest cut ever agreed.

US markets reacted with a slight fall on Monday, as analysts proclaimed the cuts to be too little too late to avoid impacting oil storage capacity. While global oil prices rose following the deal, US prices remained under pressure. “Ultimately, this simply reflects that no voluntary cuts could be large enough to offset the 19 million barrel per day average April to May demand loss due to the coronavirus,” wrote analysts from Goldman Sachs.

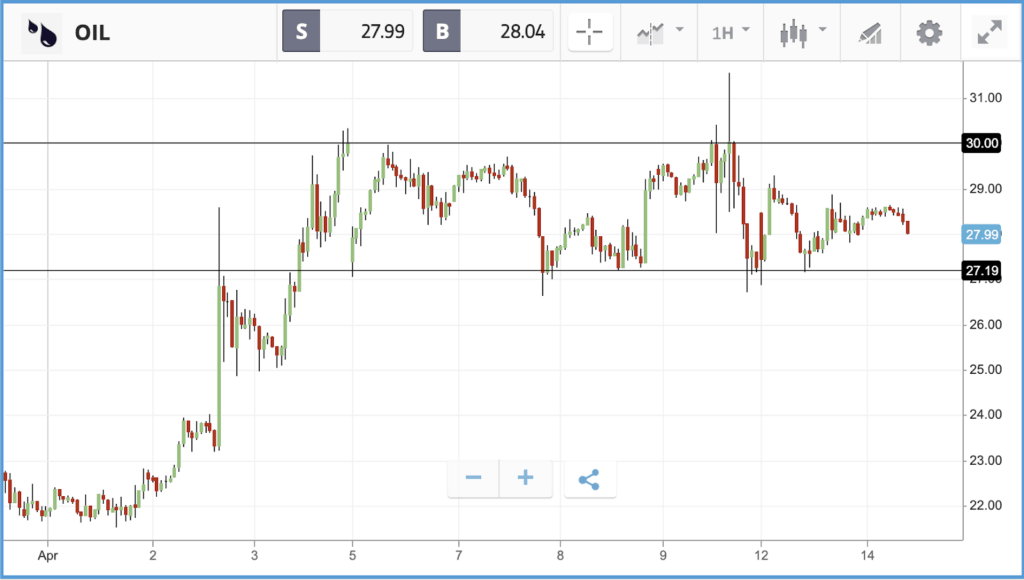

Since the beginning of the month, the price seems to have found support around the $27 mark but has failed in its attempts to convincingly clear the psychologically important $30 level.

On Monday, during a two-hour press conference, President Trump incorrectly claimed that the authority of the President and federal government is “total” when it comes to lifting coronavirus restrictions. Despite his claims that states “can’t do anything without approval of the President of the United States,” the US constitution hands public health responsibilities to state and local officials. Trump said that he wants the US economy to reopen by May 1, but many state governors have made it clear that they will not be pressured into lifting restrictions. When the lockdowns do begin to ease, investors will be watching closely for signs of whether those decisions have been taken too soon, as a resurgent wave of Covid-19 cases could potentially trigger another sell-off.

Meanwhile, share trading in Asia hit one-month highs overnight on the back of better than expected trade data from China, extending gains made earlier in the week. European markets have opened up higher, with US futures also pointing towards a firmer open. The exception is the FTSE100, which is being held back by a stronger GBP. As many of the index’s constituents earn revenue overseas, a stronger GBP is unfavourable when these earnings come to be exchanged.

Nasdaq back in single figure losses for 2020 so far

The three major US indices have all posted double digit returns over the past five trading days — Monday to Thursday last week, plus yesterday — and the Nasdaq Composite is now down just 8.7% year-to-date. The weekly gain was one of the best on record, and took stocks out of bear market territory. In a note investment firm T. Rowe Price highlighted that it was “the most beaten-down asset classes” that fared best, with small-cap stocks and value stocks outperforming. The firm’s traders said that the turn in sentiment was driven by easing new Covid-19 infection rates in hotspots such as Italy, Spain and New York. In New York, which accounts for more than 5% of global cases, deaths spiked again during the week, but new hospitalisations continued to slow.

Yesterday, the oil giants posted mixed days with little consensus from investors over the Opec deal; Chevron gained 0.7%, while Exxon Mobil fell by the same amount. The energy sector within the S&P 500 fell by 0.4% overall.

Financial stocks fell harder, closing 3.6% down as investors eye likely dismal earnings from several of the major US banks. BNY Mellon, Bank of America, Wells Fargo, Morgan Stanley, JPMorgan and more all report their Q1 2020 earnings this week.

S&P 500: -1% Monday, -14.5% YTD (+11% past five trading days)

Dow Jones Industrial Average: -1.4% Monday, -18% YTD, (+11.1% past five trading days)

Nasdaq Composite: +0.5% Monday, -8.7% YTD (+11.1% past five trading days)

FTSE 250 gains 14% in a week

UK markets were closed on both Friday and Monday due to the Easter holiday, but over the past five trading days London-listed stocks have posted substantial gains. Small cap names in particular have enjoyed a major rally. The FTSE 250 is up 13.7% over the past five trading days, versus 6.6% for the FTSE 100, although both indices are still sitting on 20% plus losses year-to-date, lagging well behind their US counterparts. On Thursday, ahead of the Easter weekend, both indices closed almost 3% higher. The FTSE 100 was carried higher by substantial gains from names including ITV, Legal & General and Lloyds Banking Group. Along with other banking names, Lloyds’ share price almost halved in the first three months of the year due to a combination of falling interest rates, heightened potential for borrowers to default and a forced dividend suspension. In the FTSE 250, previously beaten down names including Cineworld and William Hill also posted the largest Thursday gains.

FTSE 100: +2.9% Thursday, -22.5% YTD (+6.6% past five trading days)

FTSE 250: +3.4% Thursday, -25% YTD (+13.7% past five trading days)

What to watch

Johnson & Johnson: Consumer goods and pharmaceutical giant Johnson & Johnson has been a standout performer this year, and is down only 4.2% year-to-date, given the pickup in demand for its products. The company operates in sectors ranging from infectious disease to toothpaste, and is one of the firms working towards a coronavirus vaccine. Analysts will likely probe management on whether any surge in demand for the firm’s products has now subsided, and more detail on the individual sectors the company operates in. Analyst expectations for earnings per share in Q1 have fallen from $2.27 three months ago, to $2.01 now, although Wall Street still falls in favour of a buy weighting on the stock.

JPMorgan Chase: JPMorgan CEO Jamie Dimon’s comments will be among the most watched of the week, after he wrote that he is anticipating a “bad recession” and “some kind of financial stress similar to the global crisis of 2008” in his annual letter to shareholders last week. A huge number of items will be on the table for discussion when the company reports its Q1 earnings on Tuesday, including the impact of near-zero interest rates, lending policies, the firm’s role in providing small business loans as part of the US’ coronavirus response and more. Wall Street analyst expectations for the first quarter have fallen from $2.71 three months ago to $2.18 now.

Wells Fargo: JPMorgan is joined today by rival Wells Fargo, which is also reporting its Q1 figures, where similar topics will be on the table. In addition, there will likely be interest in what impact February’s $3bn fine for a scandal involving the creation of millions of fake accounts will have on the firm. For Wells in particular, analysts are likely to probe on the potential for homeowners to default on their mortgages in greater numbers, and difficulties in lending out new money. The company is the largest mortgage lender in the US, and its business is more dependent on that sector than many. Analyst earnings per share estimates for the quarter have cratered in recent months, falling from $0.91 three months ago to $0.37 now, and analysts overwhelmingly favour a hold rating on the stock.

Earnings season

US Q1 2020 corporate earnings season kicks off this week, beginning as usual with many of the large banks. Dismal numbers are expected from many companies, and how markets react will be determined by how poor results are versus expectation rather than in absolute terms. Closely watched items across industries will be companies’ ability to manage debt, how revenue has been impacted and what has happened to capital expenditure, along with how firms plan to handle dividends and stock buybacks. Investors should expect to see companies toss guidance out the window, make amendments to near and mid-term plans, and there are likely to be layoffs announced. Earnings reports will also be used as windows into consumer demand and spending, with many attempting to extrapolate the figures to develop a picture of how badly the economy is being impacted by the shutdown. The state of M&A deals that were in progress or recently announced when the pandemic hit, such as Morgan Stanley’s $13bn acquisition of E*Trade, will also be in the spotlight.

Crypto corner

Cryptoassets fell away from recent highs over the Easter weekend following last week’s substantial gains.

Bitcoin trended down over the weekend but surged on Sunday, hitting a high of $7172.26 before crashing down to $6555.00. It was back up trading around $6877.81 early on this morning. Ethereum followed a similar trajectory, trending down with a rally on Sunday to $165.23. Early doors on Tuesday saw it trading around $157.55. Finally, XRP saw a lesser rally on Sunday to $0.1960, trading down across the long weekend to around $0.1877 early this morning.

Square has announced that it is participating in the US government’s emergency Paycheck Protection Programme. This is an initiative whereby loans are provided to small businesses in order to pay employees during the coronavirus crisis, as part of the $2.3 trillion stimulus programme. Square, who was approved by the Treasury to take part in the programme as a lender, saw almost half of its revenue from Bitcoin sales in Q4 2019.

eToro (UK) Ltd is authorized and regulated by the Financial Conduct Authority. eToro (Europe) Ltd is authorized and regulated by the Cyprus Securities and Exchange Commission. eToro AUS Capital Limited is regulated by the Australian Securities and Investments Commission, ABN 66 612 791 803, AFSL 491139.

This is a marketing communication and should not be taken as investment advice, personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without having regard to any particular investment objectives or financial situation, and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared utilizing publicly-available information.

eToro is a multi-asset platform which offers both investing in stocks and cryptoassets, as well as trading CFDs.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 62% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money.

Cryptoassets are volatile instruments which can fluctuate widely in a very short timeframe and therefore are not appropriate for all investors. Other than via CFDs, trading cryptoassets is unregulated and therefore is not supervised by any EU regulatory framework. Your capital is at risk.