Despite a slight reprieve from Asian shares overnight, markets have ended the week on a downbeat tone as overall expectations of increased central bank stimulus came up short. European markets are down as much as 0.5% this morning whilst US futures are flat, except the Nadsaq which is showing a small gain of 0.3%

Eight of the S&P 500’s 11 sectors were in the red on Thursday, as investors reacted to Wednesday’s policy statement from the Federal Reserve. After-hours, there were reports that the Fed is also considering an extension to restrictions on dividends and share buybacks imposed on large banks. The central bank took action in June to cap dividends and ban share buybacks, saying that while banks had sufficient capital, it wanted them to preserve capital levels. Now, the Fed has said it will test big bank resilience through two new tests simulating severe recessions, with the results to be released by the end of the year.

On the positive side, there was a marginal improvement in the number of weekly jobless claims, with the figure coming in at 860,000, down by around 30,000 on the previous week. This was the third week in a row where the figure came in under the one million mark, although momentum has stalled.

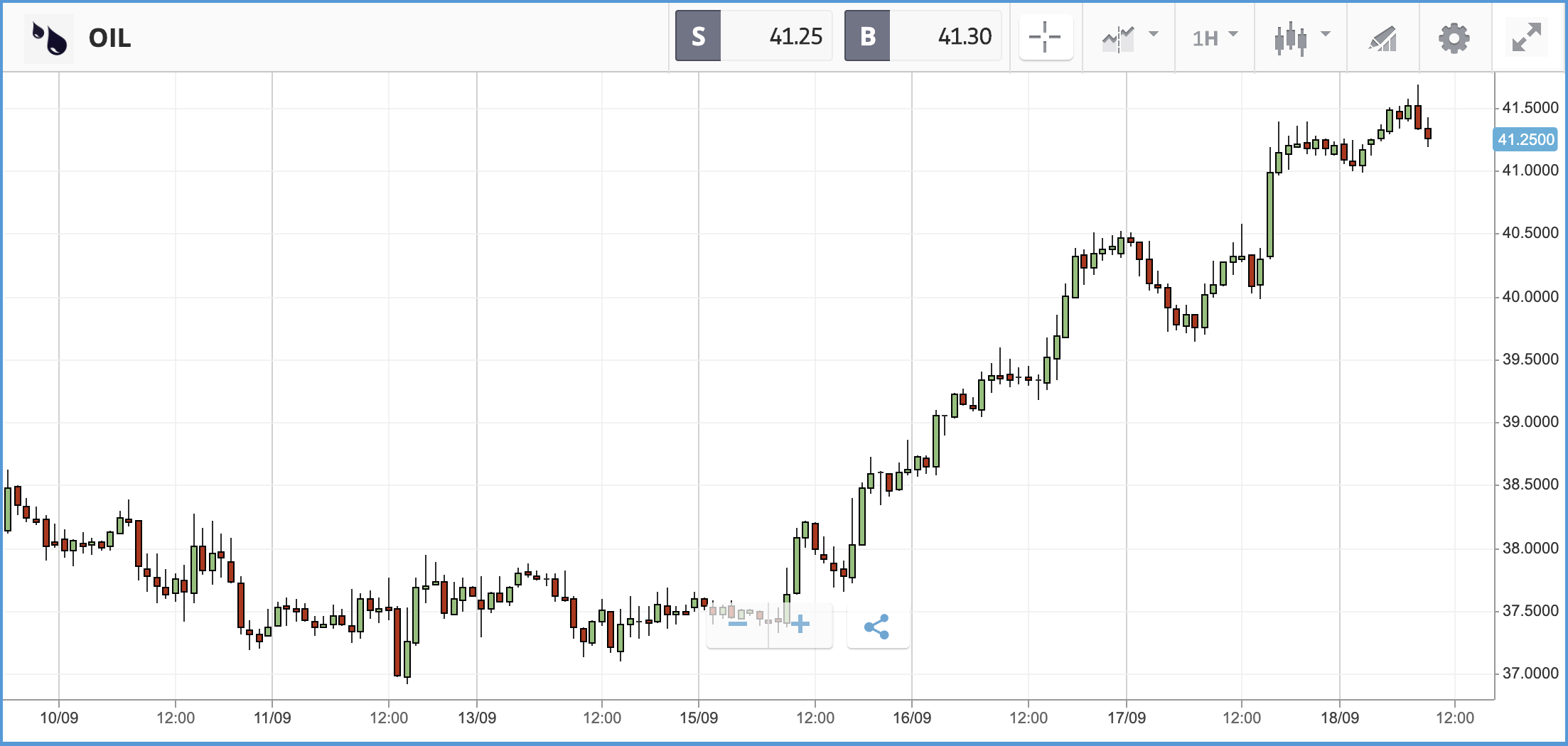

Elsewhere the price of oil has firmed up as OPEC signals its intent to crackdown on those members not complying with the production cuts. The price has also been helped by Hurricane Sally cutting US production. With the dollar now turning back down after its rally post-Fed plus a new storm brewing in the Gulf of Mexico, oil could be on track to build on the almost 10% gain it has made this week.

Southwest grounds 130 Boeing airliners

The Nasdaq Composite once again fell hardest among the major US stock indices on Thursday, losing 1.3%, with Illumina, Tesla and eBay among the names causing a drag. Illumina fell 7.6%, after an 8.4% loss on Wednesday, with the sell-off driven by rumours it is planning an $8bn acquisition of cancer-detection firm Grail Inc. In the S&P 500, which closed the day off 0.8%, Southwest Airlines was among the five worst hit stocks. The budget airline closed out the day 4% lower after announcing that it has grounded 130 Boeing 737-800 planes over discrepancies in weight data. Southwest said it made the decision “out of an abundance of caution” and it is not the first time weight issues have plagued the airline. The share price hit the firm took due to the grounding was relatively minor, given that it is already operating a reduced flight roster due to the pandemic.

S&P 500: -0.8% Thursday, +3.9% YTD

Dow Jones Industrial Average: -0.5% Thursday, -2.2% YTD

Nasdaq Composite: -1.3% Thursday, +21.6% YTD

Next raises profit forecast for second time in two months

London-listed shares fell on Thursday after the Bank of England made an expected division to hold interest rates at their current level and warned that the fragile economy is at risk from the government’s furlough scheme ending at the end of October. Retailers topped the FTSE 100 despite bleak consumer sentiment, with Next the biggest winner. The high street fashion brand jumped 4.2% after it said that it expects to deliver a profit for the year, as its recovery from the pandemic accelerates. This is the second time in two months that the firm has raised its profit outlook for the year, with its £300m expected figure up significantly from the £195m it predicted back in July. Sainsbury’s and Ocado Group also posted significant gains of 3.3% and 2.7% respectively. Miner Polymetal International, advertising giant WPP and bank NatWest brought up the back of the index, with all three closing the day out around 3% lower.

FTSE 100: -0.5% Thursday, -19.8% YTD

FTSE 250: -0.3% Thursday, -18.9% YTD

What to watch

Informa: Business intelligence and events business Informa is down more than 50% year-to-date, as the pandemic has decimated its ability to generate revenue from conferences and other exhibitions. The London-listed firm delivers its latest set of quarterly earnings on Monday. This week, JPMorgan Cazenove downgraded its rating on the stock to neutral, citing doubts about the firm’s ability to recover from here. “We have previously seen Informa as an attractive recovery play and long-term structural growth story. However, from here we have doubts,” the firm’s analysts said, pointing to a longer than anticipated period of suffering for business travel and the events industry more broadly.

US consumer sentiment: Preliminary data from the University of Michigan’s September consumer sentiment index will be delivered on Friday, with a marginal uptick expected versus August’s figure. Consumer sentiment is currently tracking near the lows seen in the depths of the pandemic, with consumers pessimistic about how long it will take for a return to normal.

Crypto corner: Libra hires HSBC banking chief

The Libra Association has hired former HSBC European head James Emmett as the managing director of Libra Networks — the operating company subsidiary of the association. Libra said on Thursday that Emmett, who spent more than 25 years at HSBC and recently stepped down as the CEO of HSBC Bank plc and Europe, is joining in October. Stuart Levey, CEO of the Libra Association, who also joined from HSBC recently, reportedly said Emmett’s leadership “will help make Libra’s vision a reality.”

Levey himself joined as chief executive earlier this year, having been the chief legal officer of HSBC. Levey is a former head of the US Treasury’s department overseeing terrorism and national security, where he was known for using the dollar as a weapon for cutting off funding to terrorist groups.

Libra was first announced by Facebook in 2019 as an independent organisation which would create a single global digital currency. However, Facebook only accounts for around 10% of its funding, with partners like Uber and Spotify also major backers.

The project has been hit by the departure of a series of partner companies including PayPal, Visa, Mastercard and Stripe. It has also faced regulatory hurdles, forcing to adjust its plans so that it now aims to launch multiple coins linked to countries’ existing currencies.

All data, figures & charts are valid as of 18/09/2020. All trading carries risk. Only risk capital you can afford to lose