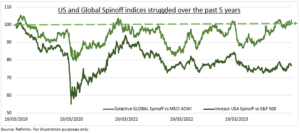

SPLIT UP: Company spin offs are leading corporate activity. Unilever (ULVR) demerging its ice cream unit incl. Ben & Jerry’s. Holcim (HOLN.ZU) its US aggregates business. Lennar (LEN) its land holdings. Cummins (CMI) its filtration business. GE (GE) nearing end of its successful split. Whilst Reddit (RDDT) continues the only glacial IPO, and M&A market, re-opening. Yet spinoffs have a mixed performance record (see chart). Blamed on passive investing, leaving small spin offs as orphans, or on activists, spinning off weak businesses. And as conglomerates make a stealth comeback, from big tech to private equity, and traditional Berkshire Hathaway (BRK.b).

SPIN OFFS: These aim to add value by better corporate focus and incentives whilst unlocking conglomerate valuation discounts. They are often tax-free, and the parent maintains a minority shareholding. As management and activist investors focus on generating returns in an uncertain macro environment. Industrial conglomerate GE (GE) has been one of the most aggressive, and successful recent proponents. Splitting itself into three after over 130 years of existence. It’s healthcare division (GEHC) has soared since listing in early 2023. And on April 2nd it is splitting its GE Vernova (GEV) power-generation business from the remaining GE Aerospace business.

CONGLOMERATE: Spin-offs fashion masks come back for once unfashionable conglomerates. Just in different guises. Whether as ‘big tech’, from Instagram to YouTube. Where any breakup could be a shareholder bonanza if history is a guide. Rockefeller did not become a billionaire until Standard Oil was broken into 34 companies in 1911. Whilst the Baby Bells telecom sum was greater than parts in its 8-way split in 1984. Or as private equity, which may be the ‘new conglomerates’, with multiple diverse businesses and $2 trillion ‘dry powder’ to invest. Whilst Berkshire Hathaway (BRK.b) is the biggest non-tech stock in S&P 500. See @Private-Equity.

All data, figures & charts are valid as of 20/03/2024.