European markets are in the red this morning as an increased Covid infection rate across the continent threatens a return to restrictive lockdown measures. The FTSE and Dax are both down just under 3% each as fearful investors move out of equities as uncertainty looms. The lack of clarity regarding further US stimulus is also likely weighing on sentiment.

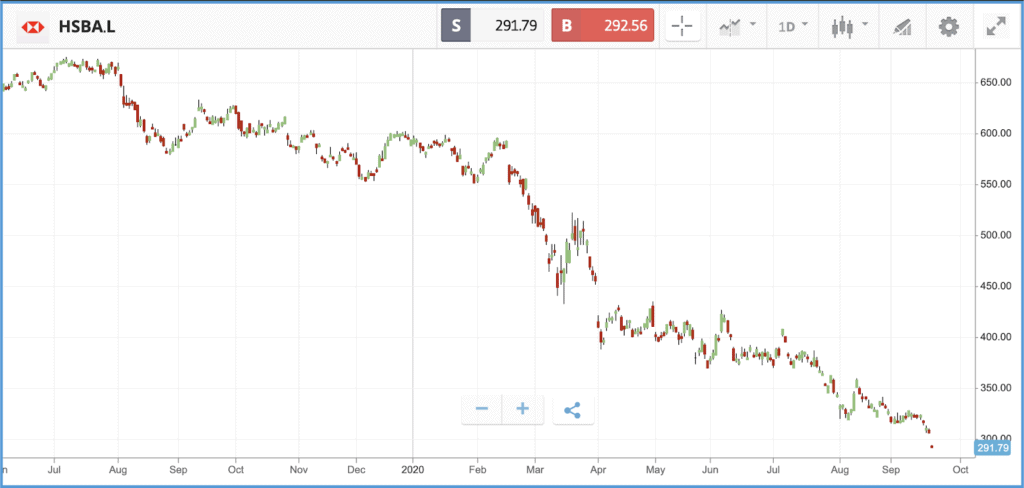

London listed banking giant HSBC is trading at a 25 year low this morning after a dossier was leaked alleging the illicit movement of funds spanning two decades involving HSBC and other major financial institutions including Standard Chartered, Deutsche Bank and JPMorgan. The implicated transactions are said to involve terrorists, drug traffickers and corrupt political regimes. HSBC responded by saying the report was ‘historical’ and since 2012 they had taken measures to overhaul these types of practices.

The S&P 500 delivered its third straight week of losses last week, with tech names including Apple and Amazon continuing to fall back from recent highs. On Sunday night, US stock futures pointed to a muted market open this morning, with investors facing down a variety of political risks. Democrat and Republican lawmakers are still struggling to come to agreement on the latest pandemic stimulus package, which has been the state of play since July. The death of Supreme Court Justice Ruth Bader Ginsberg could complicate those negotiations further and heighten tensions between the two parties in the run up to the presidential election. President Trump plans to immediately nominate someone for the seat, in the hopes of filling it before his current term is out – something that Democrats will try to stop.

Nonetheless, there were some positive signs in economic data on Friday even as the S&P 500 fell by 1.1%. The University of Michigan’s preliminary consumer sentiment index reading for September came in at 78.9, up from 74.1 the previous month and well ahead of economist expectations. That reading is the best since March, and confident consumers are a prerequisite for economic recovery in the US, given that consumer spending accounts for around 70% of the country’s economy.

Energy stocks lead the week after oil rallies back past $40 a barrel

The top line figures for the major US stock indices do not tell the full story of last week. Given their dominance market cap wise, the tech giants can easily swing indices into the red even when other sectors are performing well. Last week was just such an example of this, as while the 5% losses posted by Amazon and Apple took the index into the red, more than 70% of S&P 500 names closed the week in the green, according to analysts at financial advice firm Edward Jones.

The energy sector led the week, gaining 2.9% on aggregate, as the price of US crude oil recovered back past the $40 a barrel mark. Industrial stocks also enjoyed a positive week, gaining 1.5% on aggregate. Year-to-date, the energy sector remains behind the wider index by a huge margin; it has lost 45% to the S&P 500’s 2.8% gain overall.

“We think the new bull market will have more staying power than the tech sell-off. That said, we don’t think the short-term dip has set the market up to resume its trajectory of the past five months,” Edward Jones’ analysts wrote. “We think tech shares may continue to be a leader in both the rallies and dips ahead.”

S&P 500: -1.1% Friday, +2.8% YTD (-0.6% last week)

Dow Jones Industrial Average: -0.9% Friday, -3.1% YTD (0% last week)

Nasdaq Composite: -1.1% Friday, +20.3% YTD (-0.6% last week)

Are negative rates in store for the UK?

London-listed shares posted an almost flat week, as the Bank of England left interest rates unchanged and signalled it is ready to take additional action if required. The UK economy has a potentially bumpy road ahead, with the end of the government’s furlough support scheme looming, and the threat of a no-deal Brexit moving nearer. In a Friday note, T. Rowe Price shared the prediction of in-house economist Tomasz Wieladek, who predicted that if those risks cause the UK economy to stagnate in the second half of 2020, then the central bank could push rates well into negative territory. Bank of England governor Andrew Bailey has previously hinted that negative rates remain one option in the toolbox, one he has refused to rule out using. In the FTSE 100 last week, grocery delivery service Ocado Group was the biggest winner, gaining more than 20% after reporting encouraging signs from its switch from Waitrose products to Marks & Spencer. The news gave M&S shares a boost too, to the tune of 8.7% for the week.

FTSE 100: -0.7% Friday, -20.4% YTD (-0.4% last week)

FTSE 250: -1% Friday, -19.7% YTD (+0.1% last week)

What to watch

Kingfisher: Retailer Kingfisher is the company behind brands such as B&Q and Screwfix. The firm has been in turnaround mode since CEO Thierry Garnier took up the top seat late last year. Garnier has been forthright in saying that the firm has been trying to do too much at once, which he argued has been distracting the business from a focus on its customers. The company’s share price has enjoyed a strong 2020, gaining 24.6% year-to-date as the pandemic has driven demand for DIY supplies, with consumers taking advantage of being stuck at home. Kingfisher delivers its latest quarterly earnings update on Wednesday, investors will be watching for how well sales momentum has kept up as lockdowns have eased, in addition to how the pandemic has been affecting the broader turnaround plan.

Chicago Fed national activity index: Today, the monthly Chicago Fed national activity index for August will be released. The index combines 85 different economic indicators; a zero value means the national economy is expanding at its historic trend rate of growth, while a positive value means an above average growth rate. July’s figure came in at 1.18, after a record-high 5.33 in June. For August, the consensus is for a figure closer to 2, according to Trading Economics.

Tesla battery day

Tomorrow, Tesla will host an inaugural and highly anticipated event focused specifically on new battery technology. CEO Elon Musk has been teasing the event on social media recently, which has stirred up speculation that the electric car maker may be set to unveil major advances in battery technology, which are crucial to the mainstreaming of electric vehicles. Battery production costs, longevity and durability are all elements that analysts have suggested may be addressed, as well as the firm’s reliance on third-party battery cell makers versus in-house production. Major Tesla announcements typically lead to share price volatility, and how markets react will in part be driven by how confident investors are about timelines for any new technology making it into real-world products.

Crypto corner: EU to introduce new rules for cryptoassets in 2024

The European Union (EU) will release a new set of rules by 2024 to help streamline cross-border payments by using blockchain technology and cryptoassets, according to reports.

The move towards wider cryptoasset adoption is part of a broader effort to encourage a shift towards digital finance, especially at a time when the pandemic has boosted the notion of a cashless society, numerous reports said.

“By 2024, the EU should put in place a comprehensive framework enabling the uptake of distributed ledger technology (DLT) and crypto-assets in the financial sector,” the documents said. “It should also address the risks associated with these technologies.”

The document also said that the European Commission – the EU’s executive branch – would release a draft law to explain how the existing regulatory framework will be put into action, and how new regulations will be introduced as needed.

All data, figures & charts are valid as of 21/09/2020. All trading carries risk. Only risk capital you can afford to lose.