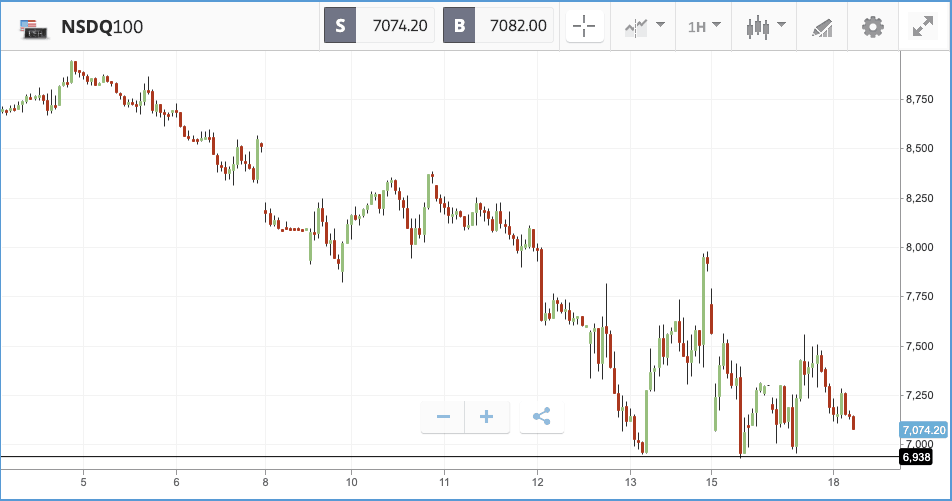

In what would have been one of the busiest days of the year across the hospitality industry, many pubs and bars found themselves empty as people chose to (or had to) stay in their homes and miss out on the usual St Patrick’s Day festivities. As a small consolation for investors who had to stay in, markets rallied with major indices gaining between 5% and 6%. Unfortunately, the rally was short lived, with US futures hitting their 5% limit down circuit breaker once again overnight. The Nasdaq, in particular, toyed with a significant support level a little below the 7000 mark for the third time in a week, but continues to hold up for now.

Asian stocks also plunged again as fears about COVID-19 outweighed fiscal policy responses, despite many Chinese businesses beginning to reopen. Virus fears continue to outweigh multiple government’s attempts at reassurance with monumental economic bailout packages. The FTSE 100 has dropped more than 4% on opening this morning, despite Chancellor, Rishi Sunak, laying out his £330bn stimulus package in a speech yesterday.

News broke yesterday that President Trump’s administration is seeking a trillion-dollar stimulus package that could include sending Americans $1,000 checks in the coming weeks. Following this, 10-year US Treasury yields climbed back above 1%, having been below half that rate earlier in the month. Treasury Secretary Steven Mnuchin reportedly warned Republican senators that without action the pandemic could drive US unemployment up to 20%. Meanwhile, Marriott said it will put tens of thousands of employees on unpaid leave.

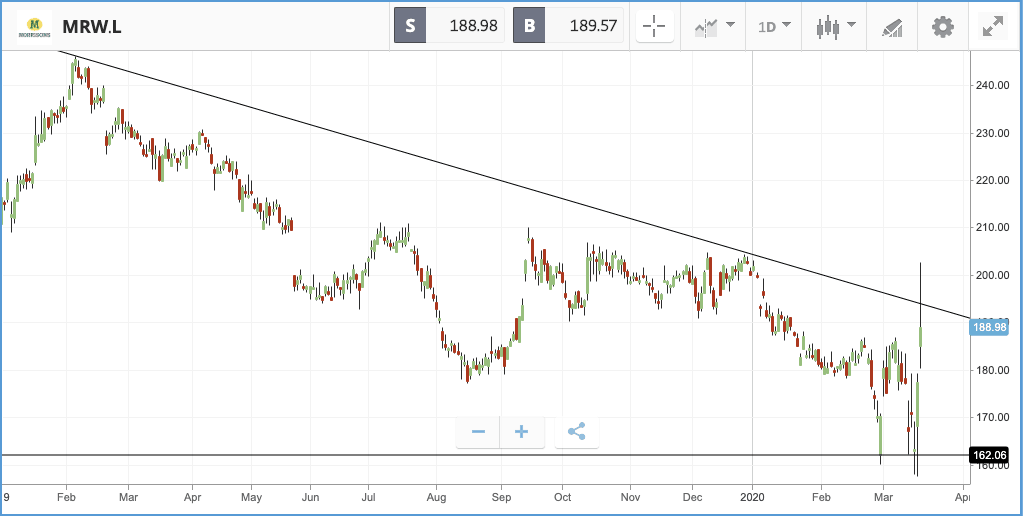

One bright spot among the sea of red this morning is UK supermarket Morrison. It’s shares have been given a boost after the company reported like-for-like sales are up an impressive 5% year on year for the first six weeks of 2020. With well documented long queues and empty shelves all over the country, investors are possibly backing supermarkets to fare much better than many businesses throughout the Coronavirus crisis as worried consumers stock up on essentials. However, whether this is sustainable is hard to predict. The reality is we don’t know how disruptive the pandemic will be to supermarkets’ supply chains and whether or not sales will be hit in the future. Sector peers Tesco and Sainsbury’s, also positive this morning, report their results on April 8th and April 30th respectively.

Biden continues surge, Boeing seeks $60bn aerospace bailout

After a positive day for all three major indices, on Tuesday evening Joe Biden continued his surge towards the Democratic Party’s nomination. Biden swept the Florida, Illinois and Arizona primaries by substantial margins. It is worth noting that each step he has taken towards the nomination has been well received by markets, but tomorrow will be a test of whether the investor reaction to his success has already been and gone.

One set of firms left out of Tuesday’s rally were the oil exploration names that have been hammered since the oil price war kicked off. Apache fell another 18.3%, taking its one-month loss close to 85%. Oil giants had a more positive day — Exxon Mobil climbed 6.7%, putting its month loss at 38.5% and its dividend yield (it has increased payments every year for almost four decades) at close to 10%.

Boeing’s headache continued yesterday as it was also left out of the broad rally, closing 4.2% lower after S&P downgraded the firm’s credit rating by two notches. Boeing also announced that it is seeking at least $60bn in government support for the aerospace industry, to help it survive in a world where demand for air travel has fallen off a cliff. Tesla also missed out on the market rally, falling 3.3% after its factory in Alameda County, California was deemed a non-essential business by the county sheriff, a decision that could force it to shut down operations due to the shelter in-place order in effect to halt the spread of the virus. The electric carmaker’s market cap has now halved over the past month, although its share price is still up 61% over the past year.

Investors got a glimpse at US retail sales data on Tuesday, although the collection period misses out recent weeks when the virus impact has been escalating. February retail sales were 0.5% lower than January, with internet retailers the only category to post a decent increase in their sales figures for the month.

S&P 500: +6% Tuesday, -21.7% YTD

Dow Jones Industrial Average: +5.2% Tuesday, -25.6% YTD

Nasdaq Composite: +6.2% Tuesday, -18.3% YTD

Large-cap stocks rally on business support

London-listed large and small cap stocks diverged markedly on Tuesday, with the FTSE 100 closing the day 2.8% higher while the FTSE 250 ended up 3% down. The FTSE 100 was as much as 3% down in morning trading, but rallied as the day progressed. The FTSE 250 was dragged lower by 20% plus losses at companies including Cineworld and gambling firm William Hill.

In the afternoon, Chancellor Rishi Sunak announced that he is making £330bn of loans available to businesses and will go further than that if required. Smaller firms will also gain access to loans of up to £5m through a business interruption loan scheme, he said, along with specific help for airlines. Despite the announcement, most airline stocks still slumped further on Tuesday. International Consolidated Airlines Group (IAG) finished 6.5% lower, while easyJet was 6.1% down.

The biggest winners in the FTSE 100 were miner Antofagasta, takeaway delivery service Just Eat, and online supermarket Ocado. Antofagasta’s jump was spurred by an upbeat earnings report, including a smaller than expected dividend cut. The Chilean mining firm also announced it plans to cut back on spending to defend its margins as the pandemic hits the global economy.

FTSE 100: +2.8% Tuesday, -29.8% YTD

FTSE 250: -3% Tuesday, -36.4% YTD

Stocks to watch

General Mills: Food manufacturer General Mills has rallied by 10.3% over the past five trading days and is up 11.4% year-to-date. The firm, which operates in over 100 countries, owns brands including Cheerios, Haagen-Dazs and Betty Crocker and, along with other food producers, has been on the receiving end of a wave of demand as supermarkets attempt to remain stocked to deal with virus-related panic buying — which is certain to be a feature of its Wednesday morning (New York time) earnings call. Last quarter, the company beat earnings expectations by a significant margin. The focus will also be on how the firm has been hurt by the pandemic, rather than just increased demand, as many of its Haagen-Dazs stores have been closed. The disruptive impact to General Mills’ operations have varied by region.

Trip.com: Nasdaq-listed Trip.com is a Chinese online travel booking firm that also owns Skyscanner. Its stock has taken a 31% hit over the past month and is down 44.9% year-to-date. Earlier this month, the company’s CEO and chairman stopped taking salaries to help deal with the losses it is facing due to plummeting travel bookings caused by the virus. The pandemic will be front and center of the firm’s Wednesday evening (New York time) earnings call, but analysts will likely probe management on whether there is any silver lining in the reported gradual return to normalcy in China, where new cases of the virus appear to have been brought under control. Currently, 24 Wall Street analysts rate the stock a buy or overweight, 12 a hold, and two a sell.

Next: UK FTSE 100 constituent Next will update the market tomorrow. The high street fashion retailer will give their full year update against the backdrop of a 42% share price loss compared to 2020 highs. The company, which rode out the wave of Brexit volatility relatively well has, like most other retailers, seen its shares hammered as the high streets become ghost towns in the midst of the pandemic. Investors will be keen to know how the company will fare and what the scope is for them to bounce back.

Crypto corner:

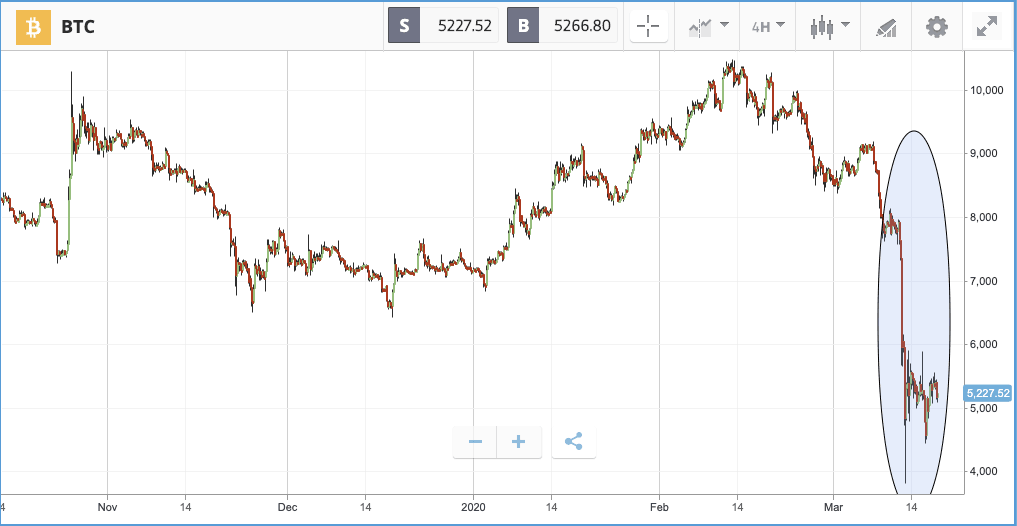

Cryptoassets rallied alongside US markets before falling away in early trading this morning, albeit to a much lesser degree. Bitcoin is now hovering around $5,200, with Ethereum at $113 and XRP down to $0.145. Even though the fall was not quite as sharp, cryptoassets are also still downtrending as the volatility continues. Investors are still fleeing risk assets and going into cash, which could put prices under pressure even further in the coming days and weeks.

On the chart below, we can see the price consolidating after a steep sell off, with the prevailing trend being downward, we could see another leg down following the consolidation period. Alternatively, if there is a material change in sentiment, a consolidation can be the beginning of a reversal but at the moment it is difficult to see where that shift would come from.

In other crypto news, the Steem community has planned a hard fork to break away from Tron founder Justin Sun’s Steemit, which he acquired last month. Steem is in essence a blog where contributors write posts and are rewarded in crypto based on the popularity of the posts. The dispute between Sun and the Steem community as to who leads the blockchain has now come to a head and a hostile hard fork is the result.

eToro (UK) Ltd is authorized and regulated by the Financial Conduct Authority. eToro (Europe) Ltd is authorized and regulated by the Cyprus Securities and Exchange Commission. eToro AUS Capital Limited is regulated by the Australian Securities and Investments Commission, ABN 66 612 791 803, AFSL 491139.

This is a marketing communication and should not be taken as investment advice, personal recommendation, or an offer of, or solicitation to buy or sell, any financial instruments. This material has been prepared without having regard to any particular investment objectives or financial situation, and has not been prepared in accordance with the legal and regulatory requirements to promote independent research. Any references to past performance of a financial instrument, index or a packaged investment product are not, and should not be taken as, a reliable indicator of future results. eToro makes no representation and assumes no liability as to the accuracy or completeness of the content of this publication, which has been prepared utilizing publicly-available information.

eToro is a multi-asset platform which offers both investing in stocks and cryptoassets, as well as trading CFDs.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 62% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work, and whether you can afford to take the high risk of losing your money.

Cryptoassets are volatile instruments which can fluctuate widely in a very short timeframe and therefore are not appropriate for all investors. Other than via CFDs, trading cryptoassets is unregulated and therefore is not supervised by any EU regulatory framework. Your capital is at risk.