Friday’s job report from the Bureau of Labor Statistics was the subject of significant controversy over the weekend. The report put the US unemployment rate at 13.3% in May, well below the level expected, but the unit admitted that a classification error had led to some furloughed workers not being counted as unemployed. If those individuals had been counted, the unemployment rate would have come in three percentage points higher. Despite the error, stocks were buoyed at the start of the week, as economists had been anticipating the unemployment rate to come in at close to 20%. Overnight in Asia both the Nikkei and the Hong Kong Hang Seng are up, with Japan’s index closing up 1.4% higher, and Hong Kong’s making marginal gains. US stock futures also traded higher ahead of Monday’s open, with the updated unemployment rate still well below what was expected. Investors are now looking forward to the Federal Reserve’s updated policy statement on Wednesday, which will be accompanied by its first economic projections of 2020. The surprising unemployment rate figures may impact the Fed’s interest rate stance and speed up the timeline for rates to move up from zero.

Elsewhere, the oil market was given a lift after Opec and Russia agreed to extend their record oil production cuts for a further month. Crude has already recovered to over $40 a barrel, with the group attempting to prop up a market devastated by the coronavirus pandemic.

S&P 500 close to breakeven year-to-date

All three major US stock indices made major gains last week, with the Dow Jones Industrial Average leading the way at 6.8%, versus 4.9% for the S&P 500 and 3.4% for the Nasdaq Composite. Investors looked past widespread civil unrest, instead choosing to focus on hopes of economic recovery. The Dow was boosted by a rebound in more economically sensitive value stocks, that have largely underperformed in 2020 so far. The Nadsaq Composite is now up near 10% in 2020 so far, while the S&P 500 is close to breaking even year-to-date. Energy and financial names had a particularly good week, with the former driven by US oil prices rebounding, while financial stocks were boosted by a rebound in US treasury yields – which hit an 11-week high. The Dow was helped higher by a major rebound in Boeing’s share price, driven by investor optimism around what the easing of lockdowns means for the airline industry. Boeing stock gained 36% last week and is now up almost 60% in 2020 so far. Airlines Delta, United and American all posted significant gains last week too, finishing up 31%, 44% and 67% higher respectively.

S&P 500: +2.6% Friday, -1.1% YTD (+4.9% last week)

Dow Jones Industrial Average: +3.2% Friday, -5% YTD (+6.8% last week)

Nasdaq Composite: +2.1% Friday, +9.4% YTD (+3.4% last week)

UK stocks shake off lack of Brexit negotiation progress

Similar to their US counterparts, the FTSE 100 and FTSE 250 soared last week, gaining 6.7% and 7% respectively. On Friday, both indices gained 2.3%, despite the European Union’s chief Brexit negotiator saying that there have been “no significant areas of progress” in negotiations between the UK and EU. He also accused the UK of “backtracking” on its commitments, and said fisheries, competition rules, governance and police cooperation are four key areas where sticking points remain. Over the weekend, British Airways – which is part of International Consolidated Airlines Group (IAG) – made headlines, as pilots’ union Balpa accused the firm of undermining talks on job losses. As with US airlines, IAG posted big gains last week, closing the week out 43% higher – including a 13.6% jump on Friday. The firm was one of the biggest winners in the FTSE 100 on Friday, with other travel names, plus financial and energy stocks, also helping take the index higher. Oil giants Royal Dutch Shell and BP finished the day 7.8% and 6.9% higher respectively, while Legal & General, Prudential, and Royal Bank of Scotland all rose by more than 8%.

FTSE 100: +2.3% Friday, -14% YTD (+6.7% last week)

FTSE 250: +2.3% Friday, -16.7% YTD (+7% last week)

What to watch

Coupa Software: California-based Coupa provides software that helps large companies maintain oversight of how money and resources are spent within their businesses. The firm’s share price has jumped 48% year-to-date and is up almost 80% over the past 12 months, as cloud-based software providers have become an investor favourite with large swathes of the corporate workforce working remotely. Coupa reports its latest set of quarterly earnings on Monday, where analysts are expecting an earnings-per-share figure of $0.07, in line with their expectations three months ago. Currently, 13 analysts rate the stock as a buy or overweight, seven as a hold, and two as an underweight or sell.

Thor Industries: Recreational vehicle firm Thor sells RVs and towable camper trailers, including the famous Airstream brand. The company’s share price has soared more than 30% in 2020 so far, as investors anticipate that the coronavirus pandemic will cause more holidaymakers to look to domestic travel options, such as camping trips, rather than spending on international travel. Thor reports its latest set of quarterly earnings on Monday, where investors will be watching for details of the company reopening its US assembly lines, and a look into whether consumer demand has delivered the growth investors are anticipating. That said, analyst expectations for profit in the quarter being reported have sunk dramatically over the past three months, and the share price spike has caused some analysts to remove their buy rating on the stock.

What the rebound in longer-term US Treasury yields means

Optimism around the economic recovery pushed the yield on the 10-year US Treasury to its highest level since mid-March, as investors moved out of the safe-haven government debt and back into corporate bonds – including in sectors of the markets that have been under the most pressure. Remember, when bond prices fall, yields rise. In a Friday note, Traders at T. Rowe Price highlighted that the volume of deals in the investment grade corporate bond market was almost double what they had been expecting, with most new debt issuance being met with solid demand. The rebound in Treasury yields is the bond market’s way of saying that the worst is over for the US economy and means that the price of borrowing will once again begin to climb. That is good news for financial stocks, which suffer from compressed margins when yields are stuck at rock bottom levels. All eyes will now be on the Federal Reserve, and whether the central bank plans to maintain zero rates for the long-term as it waits out the risk of a second wave of the virus, or if it plans to take last week’s jobs numbers and other data points as a reason to begin increasing rates again.

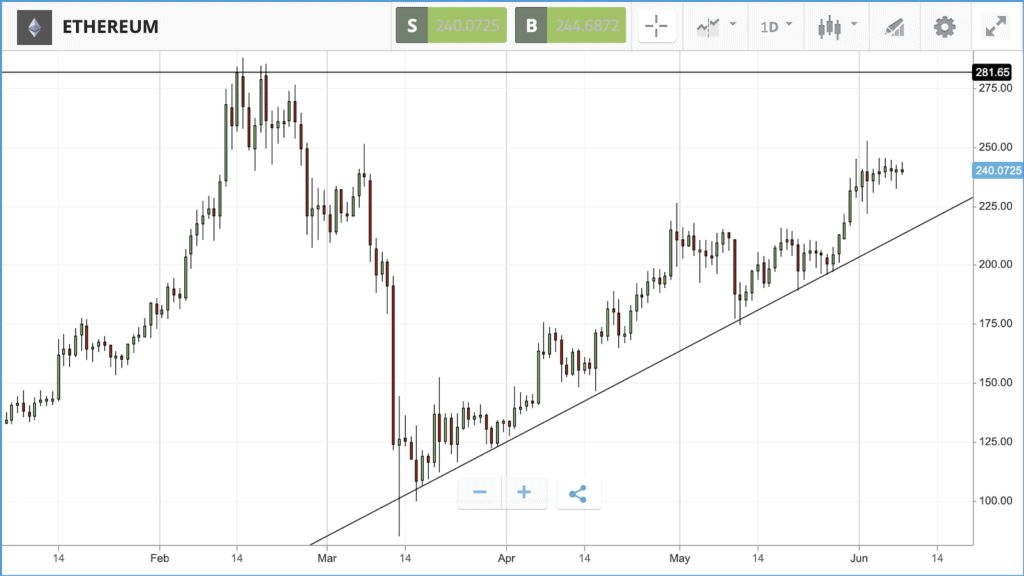

Crypto corner: Ethereum transaction fees surpass Bitcoin for first time since March

Over the weekend Ethereum transaction fees – a measure of how much currency is being mined – surpassed Bitcoin for only the second time this year.

Data from Glassnode showed Ethereum fees breaking above Bitcoin fees, with experts pointing out this could be a bullish sign for Ethereum.

According to a report on Bitcoinist, the founder of Mythos Capital, Ryan Sean Adams, recently noted that the price of Ethereum has been closely correlated with the transaction fees Ethereum users pay over the past four years.

Ethereum is currently trading at $241, its highest level since March.

All data, figures & charts are valid as of 08/06/2020. All trading carries risk. Only risk capital you can afford to lose.